Private Foundation vs Donor Advised Fund: 2026 Guide for High-Net-Worth Donors

Private Foundation vs Donor Advised Fund: 2026 Guide for High-Net-Worth Donors

Choosing between a private foundation vs donor advised fund is one of the most consequential philanthropy decisions a high-net-worth individual makes in 2026. Both vehicles offer powerful tax advantages. However, they differ dramatically in cost, control, privacy, and IRS compliance requirements. Understanding those differences can save you tens of thousands of dollars and align your giving with your long-term legacy goals. Our team at Uncle Kam’s high-net-worth tax advisory practice breaks it all down below.

Table of Contents

- Key Takeaways

- What Is the Difference Between a Private Foundation and a Donor Advised Fund?

- What Are the 2026 Tax Deduction Rules for Each Vehicle?

- How Much Does Each Option Cost to Set Up and Maintain?

- Who Controls the Giving — and How Much Privacy Do You Get?

- How Can You Use Appreciated Assets in Each Structure?

- What Are the 2026 Compliance and Regulatory Obligations?

- Which Vehicle Is Right for Your Philanthropic Goals in 2026?

- Uncle Kam in Action: Donor Maximizes Tax Savings Through Smart Giving

- Next Steps

- Related Resources

- Frequently Asked Questions

Key Takeaways

- A donor advised fund (DAF) offers lower setup costs and simpler compliance than a private foundation.

- For 2026, DAF cash contributions are deductible up to 60% of your AGI; private foundation cash gifts are limited to 30% of AGI.

- Private foundations require an annual 5% minimum distribution and pay a 1.39% excise tax on net investment income.

- DAF assets soared 30% to $326 billion, showing explosive growth in philanthropic use of this vehicle in 2026.

- High-net-worth donors with complex giving goals may benefit from using both structures together.

What Is the Difference Between a Private Foundation and a Donor Advised Fund?

Quick Answer: A private foundation is an independent legal entity you control entirely. A donor advised fund is a charitable account held within a sponsoring public charity where you advise on grants.

The debate between a private foundation vs donor advised fund begins with structure. Each vehicle is a legitimate tax-exempt charitable giving tool. However, they serve different needs and carry very different obligations.

What Is a Private Foundation?

A private foundation is a nonprofit legal entity typically created by a single donor, family, or corporation. It is classified as a 501(c)(3) organization under the IRS private foundation rules. You or your family control its board of directors. You decide which charities receive grants. You also manage its investments, hire staff, and set grantmaking priorities entirely on your own terms.

However, private foundations come with significant regulatory strings attached. The IRS imposes strict self-dealing rules, minimum distribution requirements, and annual public filings. Furthermore, the top 100 foundations in America now account for roughly 40% of all U.S. foundation assets, meaning this structure has historically been the domain of the ultra-wealthy with long-term institutional goals.

What Is a Donor Advised Fund?

A donor advised fund (DAF) is a charitable giving account held within a sponsoring public charity. Large financial institutions such as Fidelity Charitable, Schwab Charitable, and Vanguard Charitable sponsor the most popular DAFs. You contribute assets to the fund, take an immediate tax deduction, and then recommend grants to qualifying charities over time.

DAF assets soared 30% to reach $326 billion in assets under management, according to recent 2026 sector data. This explosive growth reflects how attractive the simplicity, flexibility, and favorable tax treatment of DAFs have become for high-net-worth donors seeking efficient philanthropy.

Pro Tip: The key legal distinction is ownership. When you contribute to a DAF, the sponsoring charity owns the assets. In a private foundation, you and your family retain full ownership and control. This difference drives most of the tax and compliance differences between the two.

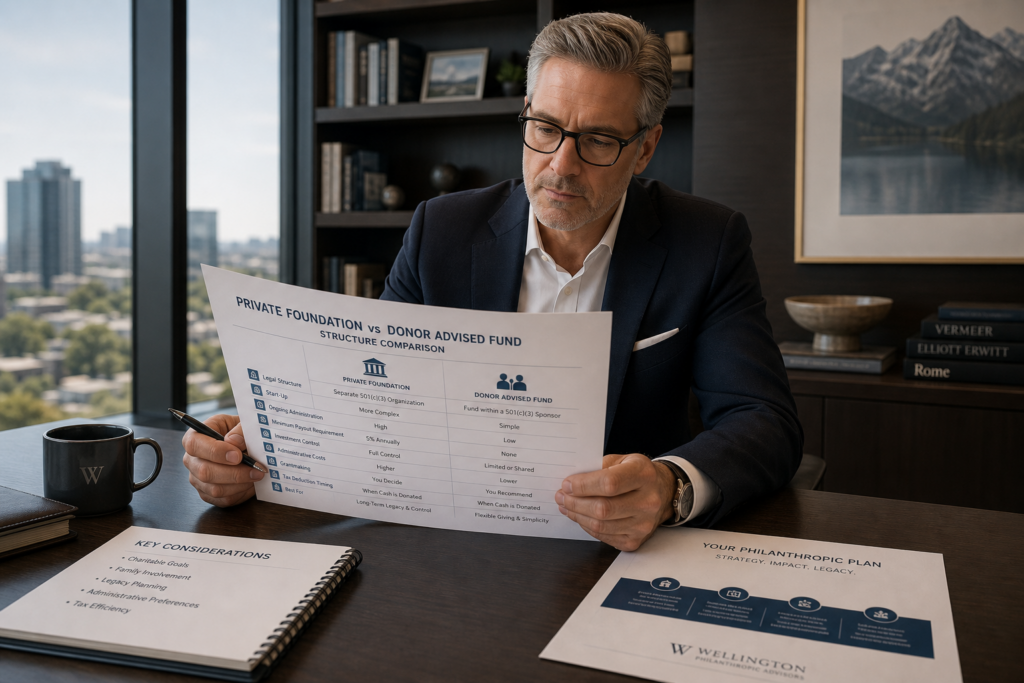

Side-by-Side Structural Comparison

Use this table to understand the fundamental structural differences before diving into the tax details:

| Feature | Private Foundation | Donor Advised Fund |

|---|---|---|

| Legal Structure | Independent 501(c)(3) entity | Account within a public charity |

| Asset Ownership | Donor/family | Sponsoring organization |

| Grantmaking | Full control | Advisory role (recommendations) |

| Minimum Setup | Typically $1M+ | As low as $5,000–$10,000 |

| Privacy | Public 990-PF filing required | Anonymous grants possible |

| Family Employment | Permitted (with restrictions) | Not permitted |

What Are the 2026 Tax Deduction Rules for Each Vehicle?

Quick Answer: DAFs offer significantly higher AGI deduction limits than private foundations. For 2026, DAF cash contributions are deductible up to 60% of AGI versus only 30% for private foundations.

The tax deduction rules represent one of the most critical differences in the private foundation vs donor advised fund debate. For the 2026 tax year, the IRS maintains distinct limits for each vehicle. Understanding these limits helps high-net-worth donors plan their giving strategy around maximum tax efficiency.

Donor Advised Fund Deduction Limits for 2026

When you contribute cash to a DAF, you may deduct up to 60% of your adjusted gross income (AGI) in 2026. This is the same limit that applies to donations directly to public charities. It is one of the most generous deduction limits available under U.S. tax law.

For contributions of long-term appreciated property — such as stocks, real estate, or business interests — the deduction limit drops to 30% of AGI. However, you still avoid paying capital gains tax on the appreciation. This combination of a full fair-market-value deduction plus capital gains bypass makes appreciated-asset contributions to a DAF extremely powerful. You can carry forward any unused deductions for up to five additional years under IRS Publication 526 rules.

Private Foundation Deduction Limits for 2026

Private foundations face tighter deduction limits. Cash contributions to a private foundation are deductible up to 30% of AGI for 2026. This is half the limit available for DAF cash contributions. Furthermore, contributions of appreciated property to a private foundation are generally limited to your cost basis — not fair market value — which significantly reduces the tax benefit compared to DAFs.

There is one exception: contributions of qualified appreciated stock (publicly traded stock held long-term) to a private foundation may still qualify for a fair-market-value deduction, up to 20% of AGI. This rule rewards donors who contribute listed securities rather than closely held business interests or real estate.

Pro Tip: If you earn a large bonus or experience a liquidity event in 2026, front-loading a DAF contribution lets you take a deduction at 60% of AGI this year. You can then distribute grants to charities over multiple years — giving you time to choose recipients carefully.

2026 Deduction Limits Comparison Table

| Contribution Type | DAF (2026 Limit) | Private Foundation (2026 Limit) |

|---|---|---|

| Cash | 60% of AGI | 30% of AGI |

| Publicly Traded Stock (Long-Term) | 30% of AGI (FMV deduction) | 20% of AGI (FMV deduction) |

| Non-Publicly Traded Appreciated Property | 30% of AGI (FMV deduction) | 30% of AGI (cost basis only) |

| Carryforward Period | 5 years | 5 years |

Always verify current deduction limits with the IRS charitable contribution deduction guidance or consult a qualified tax advisor. Our tax strategy team can help model the right approach for your specific income level and asset mix.

How Much Does Each Option Cost to Set Up and Maintain?

Quick Answer: A DAF has minimal setup costs — sometimes zero — and charges a small annual administrative fee. A private foundation typically costs $5,000–$50,000+ to establish and requires ongoing legal, accounting, and staff expenses.

Cost is often the deciding factor in the private foundation vs donor advised fund choice for donors who are earlier in the wealth accumulation journey. Even for the ultra-wealthy, administrative burden matters when it competes with time spent on other priorities.

Cost of Opening and Running a Donor Advised Fund

Opening a DAF with a major sponsoring organization typically requires a minimum contribution of $5,000 to $10,000. After that, annual fees are typically a small percentage of assets under management — often 0.60% or less for large accounts. There are no legal formation costs, no attorney fees for incorporation, and no IRS application process. You simply open an account and fund it.

In addition, the sponsoring organization handles all investment management, grant processing, tax receipt documentation, and regulatory compliance. This means you do not need to hire staff, engage CPAs for annual filings, or worry about the IRS rules governing private foundations.

Cost of Forming and Operating a Private Foundation

Forming a private foundation involves filing articles of incorporation or a trust document, applying to the IRS for 501(c)(3) status using Form 1023, and establishing governance procedures. Legal fees alone can run $5,000 to $25,000 or more depending on complexity. The IRS user fee for the full Form 1023 application is currently $600.

Ongoing costs are significant. You must file Form 990-PF annually. You need a CPA or tax attorney familiar with nonprofit compliance. Investment management, staff salaries, and office costs add further expense. Realistically, a private foundation needs at least $1 million in assets to justify its administrative overhead compared to a DAF. Many advisors recommend $5 million or more before a private foundation makes financial sense.

Pro Tip: One powerful strategy is to use a DAF first to accumulate charitable assets tax-efficiently. Once your philanthropic capital grows large enough, you can convert or supplement with a private foundation for greater control and legacy planning.

Who Controls the Giving — and How Much Privacy Do You Get?

Quick Answer: Private foundations give you maximum control. DAFs offer more privacy since grants can be made anonymously, while private foundation grants are publicly disclosed on Form 990-PF.

Control and privacy are deeply personal priorities. For many high-net-worth families, the ability to direct grants, hire family members in paid staff roles, and shape a lasting philanthropic legacy justifies the additional cost of a private foundation. For others, the ability to give anonymously and avoid public scrutiny makes a DAF more appealing.

Private Foundation Control and Transparency Requirements

With a private foundation, you and your family control the board. You set grantmaking priorities. You can hire family members as foundation employees — within strict IRS self-dealing rules under IRC Section 4941. You can give to foreign organizations if you meet specific expenditure responsibility or equivalency determination tests. You can also make program-related investments (PRIs) — loans or equity investments in charitable programs.

However, transparency is mandatory. Private foundations must file Form 990-PF each year. This public document discloses your grants, investments, officer compensation, and other financial details. Anyone can look up your foundation’s 990-PF through public databases. Half of America’s top 100 foundations are controlled by billionaires or their families, and these filings are subject to significant public attention and scrutiny.

DAF Control and Privacy Advantages

With a DAF, you recommend grants rather than control them legally. In practice, sponsoring organizations almost always follow donor recommendations. However, the sponsoring charity has final legal authority over all distributions. This is an important legal distinction that affects estate planning and multi-generational giving structures.

The privacy advantage is real and meaningful. DAF grants can be made anonymously. When a charity receives a DAF grant, the sponsoring organization — not you — appears as the grantor. This protects high-net-worth donors from unsolicited fundraising requests and public controversy. Furthermore, since a DAF is an account within a public charity, only the sponsoring organization files a Form 990 — and your individual giving data is not publicly disclosed.

Pro Tip: High-net-worth donors who value privacy should strongly consider DAFs for sensitive or politically contentious causes. Anonymous giving through a DAF shields your identity far more effectively than a private foundation’s public filing requirements allow.

How Can You Use Appreciated Assets in Each Structure?

Free Tax Write-Off Finder

Free Tax Write-Off FinderQuick Answer: A DAF accepts a wider range of appreciated assets — including closely held stock, real estate, and cryptocurrency — and generally provides a full fair-market-value deduction without triggering capital gains.

One of the most powerful strategies for high-net-worth donors is contributing appreciated assets instead of cash. This approach lets you take a charitable deduction at fair market value while avoiding the capital gains tax on the embedded appreciation. The choice between a private foundation vs donor advised fund significantly affects how this strategy works in practice for the 2026 tax year.

Appreciated Asset Contributions to a DAF

DAFs accept a remarkably broad range of appreciated assets. These include publicly traded stocks and mutual funds, closely held business interests, real estate, cryptocurrency, restricted stock, and even intellectual property. When you contribute these assets to a DAF, you generally receive a fair-market-value deduction up to 30% of AGI and avoid all capital gains tax on the appreciation.

Consider a specific 2026 example. You purchased stock 10 years ago for $100,000. It is now worth $500,000. If you sell it, you owe federal capital gains tax on $400,000 of gain — potentially $60,000 or more at the 20% long-term rate, plus the 3.8% net investment income tax for high earners. However, if you contribute the stock directly to a DAF, you owe zero capital gains tax. You also receive a $500,000 charitable deduction. That is the full fair market value, not just your $100,000 basis. Our tax advisory team models these scenarios regularly for clients approaching liquidity events.

Appreciated Asset Contributions to a Private Foundation

Private foundations face more restrictive rules for appreciated assets. For contributions of non-publicly traded property — such as closely held stock, real estate, or partnership interests — the deduction is generally limited to your cost basis, not fair market value. This is a significant disadvantage compared to DAFs for donors who want to contribute illiquid appreciated assets.

The one exception involves publicly traded securities held long-term. You may deduct the full fair market value of qualified appreciated stock contributed to a private foundation, subject to the 20% of AGI limit. However, if you plan to contribute closely held business interests, real estate, or pre-IPO stock to a charitable vehicle, a DAF almost always provides the superior tax outcome.

Pro Tip: Planning a business sale or IPO in 2026? Contribute appreciated shares to a DAF before the transaction closes. This can generate a large current-year deduction and completely eliminate capital gains tax on the gifted shares. Timing is everything — consult your advisor well before the closing date.

What Are the 2026 Compliance and Regulatory Obligations?

Quick Answer: Private foundations face far more onerous compliance requirements than DAFs in 2026, including mandatory annual distributions, excise taxes, self-dealing rules, and public Form 990-PF filings.

Regulatory compliance is arguably the most underappreciated cost of operating a private foundation. The IRS imposes a distinct set of rules on private foundations under Chapter 42 of the Internal Revenue Code that simply do not apply to DAFs. Understanding these obligations is essential before choosing the private foundation vs donor advised fund path.

Private Foundation Compliance Requirements in 2026

Private foundations must meet all of the following requirements in 2026:

- 5% Minimum Distribution: The foundation must distribute at least 5% of its average net investment assets annually for qualifying charitable purposes. Failure to meet this threshold triggers significant excise tax penalties.

- 1.39% Excise Tax: The foundation pays a flat 1.39% excise tax on its net investment income each year. This applies to interest, dividends, capital gains, and rents earned by the foundation.

- Self-Dealing Prohibition: Transactions between the foundation and disqualified persons (family members, officers, major donors) are strictly prohibited. Violations result in severe excise tax penalties.

- Annual Form 990-PF Filing: This public document reports all grants, investments, officer compensation, and other financial activity. The 2026 IRS Form 990 Transparency Initiative is proposing even greater reporting requirements for foundations receiving government funding.

- Jeopardizing Investment Prohibition: Foundation managers may not make investments that jeopardize the foundation’s charitable purpose.

- Taxable Expenditure Rules: Grants to individuals or non-charitable organizations generally require prior IRS approval and detailed expenditure responsibility procedures.

DAF Compliance Requirements in 2026

DAF compliance is dramatically simpler. The sponsoring organization handles all regulatory obligations. As a DAF account holder, you are not required to make minimum annual distributions. You can let funds grow tax-free for years before recommending grants. There is no excise tax on investment income. There are no annual filings on your part. The sponsoring charity handles all legal obligations.

However, DAFs do have one important compliance limitation: you cannot recommend grants to individuals. All grants must go to IRS-qualified public charities. You also cannot receive any benefit in exchange for a DAF grant — the anti-abuse rules prohibit so-called grant-back arrangements where the donor personally benefits from a recommended grant.

Did You Know? The IRS launched a Form 990 Transparency Initiative in 2026 that proposes enhanced reporting requirements for foundations that receive government funding or act as fiscal sponsors. This could increase compliance costs for some private foundations over the next several years.

Our tax preparation and filing specialists guide high-net-worth clients through all Foundation compliance requirements and help model the true after-tax cost of each philanthropic vehicle.

Which Vehicle Is Right for Your Philanthropic Goals in 2026?

Quick Answer: Most donors benefit more from a DAF due to its simplicity, lower costs, and superior tax deduction limits. Private foundations make sense for donors with $5M+ in philanthropic assets who need maximum control and want a lasting institutional legacy.

The right choice between a private foundation vs donor advised fund ultimately depends on your specific situation. There is no universal answer. However, several clear patterns emerge when advisors work with high-net-worth donors on this decision in 2026.

Choose a DAF If You:

- Want to start giving quickly with minimal paperwork or legal setup

- Have a large income year in 2026 and want to front-load a deduction

- Plan to contribute closely held stock, real estate, or cryptocurrency

- Value privacy and anonymous grantmaking

- Have philanthropic assets under $5 million

- Prefer to avoid ongoing legal and accounting overhead

- Want to give to a broad range of public charities over time

Choose a Private Foundation If You:

- Have $5 million or more dedicated to philanthropic giving

- Want to create a lasting family legacy institution

- Want to employ family members in meaningful philanthropic roles

- Plan to make grants to foreign organizations

- Want to make program-related investments (PRIs) or social impact investments

- Prioritize full board-level control over grantmaking decisions

- Are comfortable with public disclosure of your giving activity

The Hybrid Strategy: Use Both

Many sophisticated donors use both vehicles in tandem. They use a DAF to handle quick, tax-efficient contributions of appreciated assets in high-income years. They then maintain a private foundation to pursue longer-term legacy initiatives requiring greater control, such as family scholarships, PRIs, or specific grant programs. This hybrid approach allows for maximum tax efficiency alongside institutional control.

According to the 2026 DAF Fundraising Report from Chariot, the median DAF gift is now 12 times larger than the median non-DAF gift. Meanwhile, DAF donors demonstrate retention rates 13% higher than non-DAF donors. These data points confirm that strategic use of a DAF leads to more engaged, sustained, and impactful philanthropy. Our MERNA Method incorporates philanthropic planning into a comprehensive multi-year tax strategy for high-net-worth clients.

Uncle Kam in Action: Donor Maximizes Tax Savings Through Smart Giving

Client Snapshot: Rebecca is a 52-year-old biotech executive based in the Boston metro area. She has a net worth of approximately $12 million and earns $950,000 per year in W-2 income. She had been considering establishing a private foundation for years. However, she had never acted due to uncertainty about the compliance burden.

The Challenge: In 2026, Rebecca’s company completed a secondary stock offering. She held $800,000 in company shares with a cost basis of only $75,000. She wanted to give generously to medical research charities she believed in. However, she did not want a large administrative burden. She also had a one-time income spike that pushed her into the top tax bracket. She needed a strategy that would maximize her deduction this year while preserving flexibility for future giving.

The Uncle Kam Solution: Our team recommended opening a DAF and contributing $800,000 of her appreciated company shares before selling. This eliminated capital gains tax on the entire $725,000 of appreciation — saving her approximately $159,500 in combined federal capital gains and net investment income taxes. She received a full fair-market-value deduction of $800,000 against her 2026 AGI. Given her AGI, this kept her deduction well within the 30% of AGI limit for appreciated stock contributions to a DAF.

Our team then structured a five-year grant schedule that allowed Rebecca to recommend grants to her five favorite medical research nonprofits. She carries forward unused deductions into future tax years. Additionally, we used a small portion of her cash to seed a private foundation for targeted grants to overseas medical programs she is passionate about — a use case that required the foundation’s expenditure responsibility capabilities.

The Results:

- Tax Savings: $159,500+ in capital gains tax avoided; approximately $296,000 in income tax deductions at her marginal rate

- Philanthropic Impact: Over $800,000 directed to medical research, with 5-year visibility into grantmaking plans

- Uncle Kam Fee: $12,500 for comprehensive planning, modeling, and implementation support

- First-Year ROI: Over 35x return on advisory investment

Rebecca’s story is one of many documented on our client results page. Philanthropic tax planning is one of the highest-ROI strategies available to high-net-worth donors in 2026.

Next Steps

Now that you understand the private foundation vs donor advised fund comparison, here are concrete actions to take in 2026:

- Review your 2026 AGI and identify highly appreciated assets available for charitable contribution.

- Model the after-tax impact of a DAF contribution versus a private foundation using your actual income and asset data.

- If you have a large income year in 2026, consider front-loading a DAF contribution before December 31 to maximize your 2026 deduction.

- Contact our team to schedule a strategic tax advisory session focused on your philanthropic giving plan.

- Verify current IRS deduction rules directly at IRS.gov to confirm limits applicable to your filing status.

This information is current as of 5/21/2026. Tax laws change frequently. Verify updates with the IRS if reading this later.

Related Resources

- Advanced Tax Strategies for High-Net-Worth Individuals

- Uncle Kam Tax Strategy Services

- Comprehensive Tax Guides and Planning Resources

- The MERNA Method: Strategic Tax Planning Framework

- Personalized Tax Advisory and Coaching Services

Frequently Asked Questions

Can I convert a private foundation to a donor advised fund?

Yes. You can dissolve a private foundation and transfer assets to a DAF. However, the process must follow IRS termination rules. A private foundation can terminate by distributing all assets to a public charity — which includes most DAF sponsoring organizations. The transfer counts toward the foundation’s minimum distribution requirement. Consult a qualified tax advisor before initiating a conversion, as specific rules govern whether the transfer qualifies as a terminating distribution under IRC Section 507.

Can a donor advised fund make grants to individuals?

No. DAFs cannot make grants directly to individuals. All grants must go to IRS-qualified public charities. This is a key limitation compared to a private foundation. A private foundation can make grants to individuals — such as scholarships — if it follows IRS expenditure responsibility procedures and obtains advance approval for certain grant types. If you want to fund individual scholarships or fellowships directly, a private foundation provides that capability that a DAF does not.

What happens to a donor advised fund when the donor dies?

When a DAF account holder dies, assets in the account pass to the sponsoring organization. You can designate a successor advisor — typically a family member — who continues recommending grants after your death. Most sponsoring organizations allow multi-generational DAF accounts. However, unlike a private foundation, the assets do not pass to your estate and cannot be redirected to non-charitable purposes. Succession planning for a DAF should be documented carefully with the sponsoring organization while you are alive.

Is there a minimum amount required to open a donor advised fund?

Most major DAF sponsors require a minimum opening contribution of $5,000 to $10,000. However, minimums vary by institution. Some community foundations offer DAF accounts with lower minimums. Unlike private foundations — which practically require $1 million or more to justify the administrative costs — DAFs are accessible to a much broader range of donors. The low barrier to entry is one of the key reasons DAF assets have soared 30% to $326 billion in recent years.

Do private foundation excise taxes apply to DAFs?

No. The 1.39% excise tax on net investment income that applies to private foundations does not apply to DAFs. Since a DAF is an account within a public charity, its investment income grows tax-free. This is a significant long-term advantage for donors who want their charitable assets to grow before granting. Over a 10- to 20-year time horizon, the elimination of this excise tax can meaningfully increase the total amount available for charitable distribution from a DAF compared to a foundation holding the same assets.

Can a private foundation invest in non-traditional assets like private equity?

Private foundations can hold non-traditional investments — including private equity, hedge funds, and real estate — but must avoid jeopardizing investments that put the foundation’s charitable mission at risk. Self-dealing rules also restrict transactions with disqualified persons. Program-related investments (PRIs) in mission-aligned ventures are permitted. DAFs, by contrast, generally invest in traditional diversified portfolios managed by the sponsoring organization. High-net-worth donors seeking more creative investment authority often find that a private foundation offers greater flexibility for non-traditional or mission-related investing.

How does the 2026 standard deduction affect philanthropic tax planning?

For 2026, the standard deduction is $32,200 for married filing jointly and $16,100 for single filers. High-net-worth donors who itemize generally exceed these thresholds through a combination of mortgage interest, state and local taxes (SALT), and charitable contributions. However, the bunching strategy — concentrating multiple years of giving into one large DAF contribution — remains powerful even after the One Big Beautiful Bill Act (OBBBA) changes. By front-loading several years of giving into a single large DAF contribution, you can maximize the itemized deduction in a peak income year and take the standard deduction in lower-income years. Learn more about strategic tax planning on our tax strategy blog.

Last updated: May, 2026