Arizona Bonus Income Taxes: Complete 2026 Guide to Federal Withholding and Tax Planning

Arizona Bonus Income Taxes: Complete 2026 Guide to Federal Withholding and Tax Planning

For the 2026 tax year, understanding how arizona bonus income taxes work is essential for Arizona employees and business owners. The good news: Arizona has no state income tax, which means your bonus is not subject to state-level taxation. However, federal income tax withholding, Social Security tax, and Medicare tax all apply to bonus payments, making it crucial to understand the rules and plan strategically. This guide explains federal withholding methods for bonuses, provides real-world 2026 examples, and shows you how to work with a tax preparation professional in Arizona to maximize your after-tax bonus.

Table of Contents

- Key Takeaways

- Are Bonuses Taxed Differently Than Regular Pay in Arizona?

- Federal vs. Arizona Bonus Taxation: The Advantage of No State Tax

- How to Estimate Your After-Tax Bonus in Arizona

- The Two Federal Withholding Methods for Supplemental Wages

- Strategies to Maximize Your Bonus Take-Home Pay (Legally)

- Frequently Asked Questions

- Related Resources

Key Takeaways

- Arizona has no state income tax, so bonuses avoid state-level taxation entirely.

- Federal withholding on bonuses can be calculated using either the aggregate or percentage method.

- For 2026, FICA taxes (6.2% Social Security and 1.45% Medicare) apply to all bonuses.

- Supplemental wage withholding often results in higher tax rates than regular paychecks.

- Strategic W-4 adjustments and retirement contributions can reduce your bonus tax burden.

Are Bonuses Taxed Differently Than Regular Pay in Arizona?

Quick Answer: Yes. Federal law classifies bonuses as “supplemental wages” and allows employers to use two different withholding methods, often resulting in higher withholding than your regular paycheck.

Unlike regular salary, which is spread across all paychecks throughout the year, bonus income is classified by the IRS as supplemental wages. This distinction is important because it affects how federal income tax withholding is calculated. Under IRS rules, employers have flexibility in determining withholding on supplemental wages, which can significantly impact your take-home amount.

Why Bonus Income Feels More Heavily Taxed

The reason your bonus may feel more heavily taxed than your regular paycheck comes down to federal withholding methodology. When using the “percentage method” for supplemental wages (which many employers use), the IRS withholds a flat 22% federal income tax rate on bonuses up to $1 million. This is significantly higher than the marginal tax rate many middle-income earners face on regular wages. For 2026, if your bonus exceeds $1 million in a single payment, the withholding rate jumps to 37%, making strategic planning even more critical.

The Critical Arizona Advantage: No State Bonus Tax

Arizona residents receive a significant tax advantage compared to residents of other states. Since Arizona has no state income tax, bonus income is not subject to any state-level taxation. This means employees in Arizona keep more of their bonus compared to employees in states like California (13.3% top rate), New York (10.9% top rate), or Oregon (9.9% top rate). For a $10,000 bonus, an Arizona resident might save $1,000 or more compared to a neighboring California resident, depending on income level.

Federal vs. Arizona Bonus Taxation: The Advantage of No State Tax

Quick Answer: Federal taxes apply to all bonuses in Arizona, but Arizona state income tax does not. This creates a significant tax savings advantage compared to high-tax states.

When you receive a bonus in Arizona for the 2026 tax year, you’ll face federal income tax withholding and FICA taxes (Social Security and Medicare), but you’ll avoid state income taxation entirely. This is a major advantage for high-earning Arizona residents and employees receiving substantial bonuses.

Federal Supplemental Wage Withholding Rules

For 2026, the IRS treats bonuses and other supplemental wages under specific withholding rules. The percentage method withholds a flat 22% federal income tax (or 37% on amounts over $1 million). The aggregate method combines your bonus with your regular paycheck and calculates withholding as if they were all regular wages, often resulting in lower withholding. Your employer should explain which method they’re using, but you can request a different approach if it’s not working for your situation.

FICA Taxes Apply to All Bonus Income

Regardless of the federal income tax withholding method your employer uses, FICA taxes apply to 100% of your bonus. For 2026, this means 6.2% Social Security tax and 1.45% Medicare tax are automatically withheld from every bonus payment. If you’re self-employed or a business owner, you’ll owe both the employee and employer portions (12.4% and 2.9% respectively). High-earning individuals over the Social Security wage base limit ($168,600 for 2026) only pay the Medicare portion on excess earnings.

How to Estimate Your After-Tax Bonus in Arizona

Free Tax Write-Off Finder

Free Tax Write-Off FinderQuick Answer: Use the percentage method (22% federal + 7.65% FICA) to estimate your withholding, but confirm with your employer whether they’re using the percentage or aggregate method.

Calculating your after-tax bonus is straightforward when you understand the two withholding methods. Most employers use the percentage method for supplemental wages, making the math simple. Let’s walk through real examples for 2026 and show you how to estimate your take-home amount.

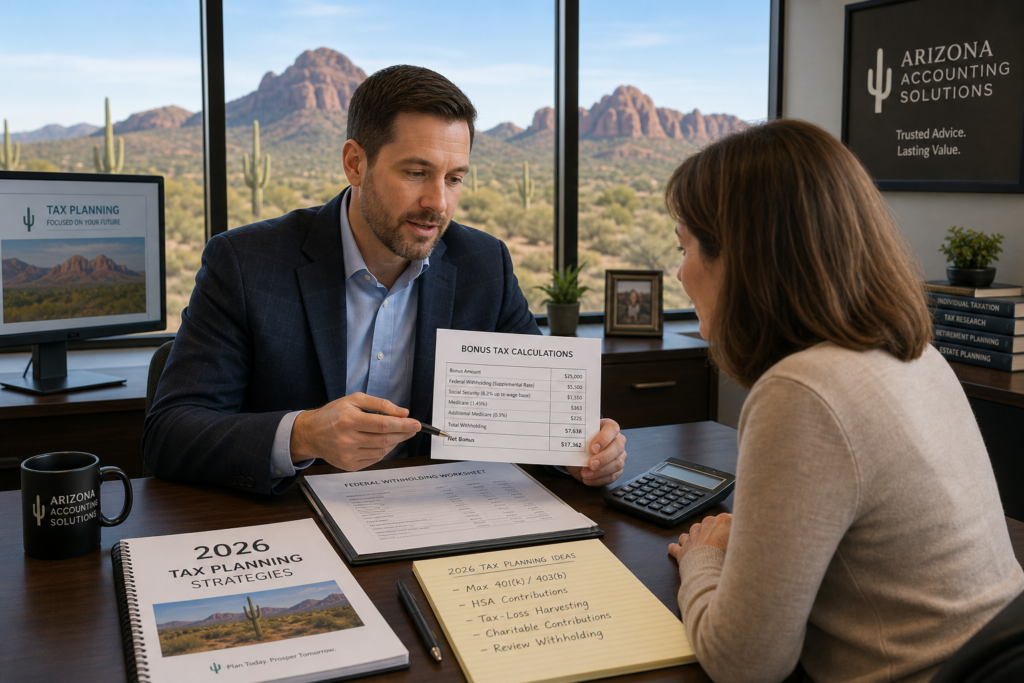

Example 1: $5,000 Bonus Using the Percentage Method

Let’s say you’re a single employee in Arizona earning $65,000 annually and you receive a $5,000 bonus in December 2026. Your employer uses the percentage method for withholding:

- Bonus amount: $5,000

- Federal income tax (22% percentage method): $1,100

- Social Security tax (6.2%): $310

- Medicare tax (1.45%): $72.50

- Arizona state income tax: $0 (Arizona advantage!)

- Total withholding: $1,482.50

- After-tax bonus: $3,517.50

In this example, your effective withholding rate is 29.65%, which includes the 22% federal income tax plus 7.65% in combined FICA taxes. Since you’re a single filer earning $65,000, your actual marginal tax rate is likely 12% federally, meaning your employer is over-withholding. This over-withholding becomes a refund when you file your 2026 tax return.

Example 2: $15,000 Bonus with High Income Earner

Now consider a married individual filing jointly with a total household income of $180,000 who receives a $15,000 year-end bonus in December 2026:

- Bonus amount: $15,000

- Federal income tax (22% percentage method): $3,300

- Social Security tax (6.2%): $930

- Medicare tax (1.45%): $217.50

- Arizona state income tax: $0

- Total withholding: $4,447.50

- After-tax bonus: $10,552.50

In this higher-income example, the percentage method results in 29.65% total withholding, but your actual federal marginal rate is approximately 22%. The aggregate method might yield lower withholding, which is why discussing withholding methods with your employer is critical.

The Two Federal Withholding Methods for Supplemental Wages

Quick Answer: The percentage method uses a flat 22% rate (simpler, often more withholding), while the aggregate method combines your bonus with regular pay (more accurate but requires more calculation).

Understanding the two federal withholding methods for supplemental wages is essential to estimate your after-tax bonus accurately. The method your employer chooses significantly impacts how much federal income tax is withheld from your bonus check.

Method 1: The Percentage Method (Most Common)

The percentage method is the most common approach employers use for bonus withholding in 2026. This method is straightforward: the IRS applies a flat 22% federal income tax withholding rate to all supplemental wages up to $1 million. For bonuses exceeding $1 million in a single payment, the rate increases to 37%. No other calculations are needed. This simplicity explains why most employers prefer this method, and it’s particularly common for bonuses processed on separate paychecks from regular wages.

Pro Tip: The percentage method often results in over-withholding for employees in lower tax brackets. If this applies to you, plan to get a refund when you file your 2026 return, or adjust your regular W-4 to receive more take-home pay during the year.

Method 2: The Aggregate Method (More Accurate)

The aggregate method combines your bonus with your regular wages for the pay period and calculates withholding as though you received one larger paycheck. This method uses your actual W-4 withholding allowances and often results in more accurate withholding that matches your true tax liability. However, it requires more detailed calculations, which is why some employers avoid it. If you want lower withholding and more take-home pay from your bonus, request that your employer use the aggregate method.

Strategies to Maximize Your Bonus Take-Home Pay (Legally)

Quick Answer: Adjust your W-4, contribute to retirement plans, use HSA contributions, and request aggregate method withholding to reduce your effective tax rate on bonuses.

While you cannot avoid federal income tax, Social Security tax, and Medicare tax on bonuses, there are legal strategies to minimize what you owe and maximize take-home pay. These strategies work best when planned before you receive your bonus.

Strategy 1: Request the Aggregate Withholding Method

Contact your employer’s payroll department and request that your bonus be processed using the aggregate withholding method instead of the percentage method. Explain that you want your bonus combined with your regular paycheck withholding to calculate more accurate federal income tax withholding. This often results in lower federal withholding, particularly for employees in lower tax brackets or those near the end of the year when they’ve already used substantial deductions.

Strategy 2: Maximize Pre-Bonus Retirement Contributions

If you know your bonus is coming, maximize your 401(k) or similar retirement plan contributions in the months before receiving it. For 2026, the 401(k) limit is $24,500 (or $32,500 for those age 50 and older with catch-up contributions). Each dollar you contribute to a traditional 401(k) reduces your taxable income dollar-for-dollar, including income from your bonus. If you contribute an additional $5,000 before your bonus arrives and you’re in the 22% federal tax bracket, you’ll save $1,100 in federal taxes—money that effectively reduces your bonus tax burden.

Strategy 3: Contribute to a Health Savings Account (HSA)

If you’re covered by a high-deductible health plan, maximize your HSA contributions before receiving your bonus. HSA contributions reduce your federal income tax, FICA taxes, and state income taxes (though Arizona has no state tax). For 2026, the HSA contribution limit is $4,300 for individual coverage or $8,550 for family coverage. These contributions are triple-tax-advantaged: they reduce federal taxes, Social Security taxes, and Medicare taxes—making HSA contributions one of the most tax-efficient ways to reduce the tax burden from your bonus.

Now, let’s discuss how to work with tax preparation professionals in Arizona to develop a comprehensive bonus tax strategy for your situation.

Uncle Kam in Action: Arizona Executive Maximizes $50,000 Bonus

Meet James, a 48-year-old marketing executive in Phoenix earning $145,000 annually in base salary. He’s married, filing jointly, with two children. In December 2026, James learned he would receive a $50,000 performance bonus—his largest bonus ever.

James initially panicked, assuming he’d lose nearly $15,000 of his bonus to taxes. He reached out to Uncle Kam’s tax planning team in Arizona. Together, they executed a strategic plan:

The Challenge: Using the standard percentage method at 22% federal withholding plus 7.65% FICA, James would have approximately $14,825 withheld from his $50,000 bonus, leaving him just $35,175. However, his actual marginal tax rate was approximately 12%, not 22%.

The Uncle Kam Solution: Three weeks before his bonus, Uncle Kam’s team advised James to:

- Contribute an additional $8,000 to his 401(k) (bringing his year-to-date total to $24,500)

- Contribute $8,550 to his HSA (maximizing his family coverage limit)

- Request his employer use the aggregate withholding method for his bonus

- Adjust his W-4 to account for the bonus and avoid over-withholding

The Results: By executing these strategies, James reduced his total tax burden from the $50,000 bonus from approximately $14,825 to $12,100—a savings of $2,725 in his first year alone. The retirement and HSA contributions not only reduced the bonus tax but also positioned him for tax-advantaged growth on $16,550 in contributions. When filing his 2026 return, James received an additional $1,200 refund due to proper aggregate method withholding and W-4 adjustments. His after-tax bonus was $38,100 instead of $35,175—a difference of nearly $3,000.

Year One ROI: James paid $1,500 in tax planning fees to Uncle Kam and saved $4,925 in federal taxes through strategic planning. His return on investment was 228% in the first year alone, and his retirement and health accounts benefited from $16,550 in tax-advantaged contributions.

Next Steps

Ready to maximize your bonus take-home pay in Arizona? Here are your next actions:

- Ask your payroll department which withholding method they use for bonuses (percentage or aggregate).

- Calculate your estimated bonus tax using the examples above or our Small Business Tax Calculator for bonus estimates.

- Schedule a consultation with a tax professional to discuss retirement contributions and HSA strategies before your bonus arrives.

- Review your W-4 and consider adjustments if you expect a significant refund when filing your 2026 return.

- Learn more about comprehensive tax strategies designed for business owners and high-earning professionals.

Frequently Asked Questions

Does Arizona tax bonus income differently than regular income?

No, Arizona does not tax bonus income at all because Arizona has no state income tax. Whether your income comes from bonuses, salary, self-employment, or investments, Arizona residents pay zero state income tax on all sources of income. This is a major advantage compared to neighboring California, which taxes all income including bonuses at progressive rates up to 13.3%.

Is the 22% withholding on my bonus my final tax liability?

Not necessarily. The 22% withholding is just an estimate of what your employer withholds. Your actual tax liability depends on your complete 2026 income, filing status, deductions, and credits. If you’re in a lower tax bracket (12%, 10%, or 0%), the 22% withholding is too high and you’ll receive a refund when you file your 2026 return. Conversely, if you’re a high earner in the 32% or 35% bracket, 22% might not be enough.

Can I avoid the 22% withholding on my bonus?

No, you cannot avoid federal income tax withholding on bonus income. However, you can request that your employer use the aggregate method instead of the percentage method, which often results in lower withholding. Additionally, maximizing retirement contributions and HSA contributions before your bonus reduces your taxable income and overall tax liability. The key is planning before you receive your bonus.

What’s the difference between supplemental wages and regular wages for tax purposes?

Supplemental wages include bonuses, commissions, vacation pay, severance, and other payments separate from regular salary. The IRS allows employers to use simplified withholding methods (percentage method) for supplemental wages, whereas regular wages require detailed W-4 calculations. This means bonuses often result in higher withholding rates than regular paychecks. The distinction exists to simplify payroll processing for employers.

Do I owe self-employment tax on a W-2 bonus?

No. If your bonus is paid as a W-2 employee, you pay employee-side FICA taxes (6.2% Social Security and 1.45% Medicare), and your employer pays the matching employer-side taxes. You do not owe self-employment tax. However, if you’re self-employed or receive a 1099 bonus payment, you owe self-employment tax on top of income tax, which is why W-2 employment is generally more favorable for bonus compensation.

How does the Social Security wage base limit affect my bonus taxes?

For 2026, the Social Security wage base limit is $168,600. Once your combined wages (salary plus bonus) exceed this limit, you stop paying the 6.2% Social Security tax on additional income. However, you continue paying the 1.45% Medicare tax on all wages above the limit. If you’re near or above the $168,600 limit when your bonus arrives, your FICA withholding will be lower because only Medicare tax applies to the portion of your bonus exceeding the wage base.

Should I request a larger refund from my W-4 for my bonus?

Rather than request a larger refund, it’s better to adjust your W-4 in advance of your bonus using the IRS W-4 calculator at IRS.gov. This ensures you don’t over-withhold throughout the year but still cover your actual tax liability. If your bonus is unexpected, you might receive over-withholding and a refund when you file, but this is inefficient use of your money. Advance planning with a tax professional is the better approach.

Is there a 1099-NEC threshold I need to know about for 2026?

For 2026, the federal 1099-NEC reporting threshold increased to $2,000 (up from $600 in prior years). This change was made under the One Big Beautiful Bill Act (OBBBA). If you’re self-employed or a contractor receiving less than $2,000 in annual payments, those payments may not be reported on a 1099-NEC. However, you still owe income tax and self-employment tax on all income, regardless of the reporting threshold. Arizona, which has no state income tax, has no additional state 1099-NEC requirements.

When should I contact a tax professional about bonus planning?

Ideally, contact a tax professional 4-6 weeks before you expect to receive your bonus. This allows time to execute retirement contributions, adjust your W-4, and communicate with your payroll department about withholding methods. If you’re expecting a significant bonus ($10,000 or more), the investment in tax planning typically pays for itself through reduced withholding and strategic contributions. Tax advisory services can provide ongoing planning to optimize your total tax situation.

Related Resources

- Tax Strategy Services for Business Owners and High Earners

- Entity Structuring for Optimal Tax Efficiency

- Services for Business Owners in Arizona

- Ongoing Tax Advisory for Maximum Planning

- IRS Publication 15: Employer’s Tax Guide

Last updated: May, 2026