Maryland State Income Tax Rate 2026 CPA Guide

For the 2026 tax year, Maryland state income tax rates present unique challenges for CPAs and tax professionals. Maryland uses a progressive income tax structure with rates ranging from 2% to 5.75%, plus mandatory local income taxes that vary by county. Understanding how Maryland’s tax system interacts with federal changes is critical for practitioners serving clients in this jurisdiction. For a continuously updated overview, review this dedicated Maryland tax guide for professionals.

Table of Contents

- Key Takeaways

- How Does Maryland’s Progressive Tax Structure Work in 2026?

- What Are Maryland’s Local Income Tax Requirements?

- How Does Maryland Conform to Federal Tax Law Changes?

- What Are the 2026 Filing Requirements and Deadlines?

- What Deductions and Credits Are Available for Maryland Taxpayers?

- How Should CPAs Handle Multi-State Issues for Maryland Clients?

- Uncle Kam in Action: Maryland CPA Saves Client $18,500

- Next Steps

- Frequently Asked Questions

- Related Resources

Key Takeaways

- Maryland uses progressive state rates from 2% to 5.75% for 2026.

- Local income taxes are mandatory and vary by county.

- Maryland does not fully conform to federal tax law changes.

- The 2026 SALT deduction cap is $40,000 for joint filers.

- Maryland offers unique credits for earned income and childcare.

How Does Maryland’s Progressive Tax Structure Work in 2026?

Quick Answer: Maryland applies graduated state income tax rates from 2% to 5.75% based on income brackets. Combined with local taxes, the effective rate typically ranges from 4.75% to 8.95%.

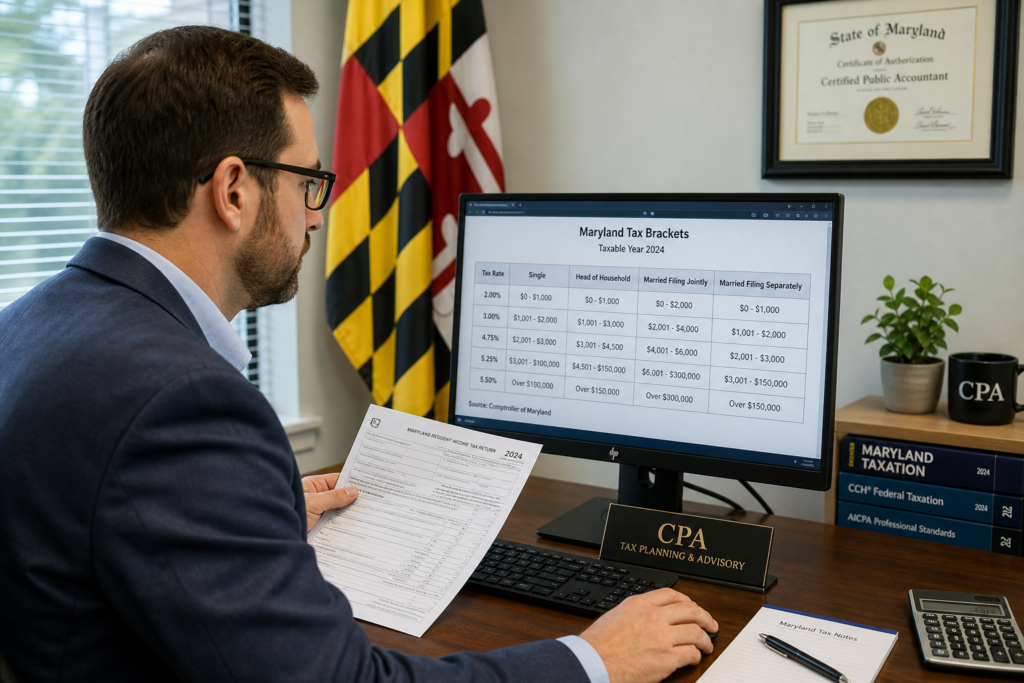

Maryland’s progressive income tax system is one of the most complex among U.S. states. For the 2026 tax year, CPAs must understand both the state and local components. The state imposes a graduated tax structure with eight brackets, starting at 2% for the lowest earners and reaching 5.75% for high-income taxpayers. This is administered by the Maryland Comptroller of Maryland. Practitioners can cross-check statutory language and administrative guidance against this practical Maryland CPA income tax overview when scoping engagements.

Understanding the State Income Tax Brackets

Maryland’s 2026 state income tax brackets apply progressively. The structure typically includes thresholds at $1,000, $2,000, $3,000, $100,000, $125,000, $150,000, $250,000, and above. However, practitioners should verify current-year brackets directly with the Maryland Comptroller as these figures may adjust for inflation.

The top marginal rate of 5.75% applies to taxable income exceeding $250,000 for single filers and $300,000 for joint filers. This rate has remained stable since 2008, making Maryland a relatively high-tax state compared to neighboring jurisdictions.

| Income Range | State Tax Rate | Filing Status |

|---|---|---|

| $0 – $1,000 | 2.00% | All filers |

| $1,000 – $2,000 | 3.00% | All filers |

| $2,000 – $3,000 | 4.00% | All filers |

| $3,000 – $100,000 | 4.75% | All filers |

| $100,000 – $125,000 | 5.00% | All filers |

| $125,000 – $150,000 | 5.25% | All filers |

| $150,000 – $250,000 | 5.50% | All filers |

| $250,000+ | 5.75% | All filers |

2026 Federal Conformity Considerations

Maryland generally conforms to the federal definition of adjusted gross income (AGI) but makes numerous adjustments. For 2026, CPAs must be aware that Maryland has not adopted several provisions of the One Big Beautiful Bill Act (OBBBA). This creates planning opportunities but also compliance complexities. Strategic tax planning becomes essential when federal and state laws diverge.

Pro Tip: Maryland’s tax brackets don’t adjust automatically for inflation. Monitor legislative updates each session to identify changes affecting client tax liability.

Calculating Maryland State Tax for High Earners

For a Maryland resident with $400,000 in taxable income for 2026, the state tax calculation involves applying each rate to its corresponding bracket. The top rate of 5.75% applies only to income above $250,000. This means $150,000 of income is taxed at 5.75%, resulting in approximately $8,625 in state tax on that portion alone.

When combined with local taxes (discussed below), the total Maryland income tax burden for this taxpayer could exceed $30,000. Therefore, strategic deduction planning and income timing become critical for high-net-worth Maryland residents.

What Are Maryland’s Local Income Tax Requirements?

Quick Answer: Maryland requires all residents to pay local income tax to their county or Baltimore City. Rates range from 2.25% to 3.20% depending on jurisdiction.

Unlike most states, Maryland imposes a mandatory local income tax in addition to the state tax. Every resident must pay local income tax to the county where they reside on December 31 of the tax year. Nonresidents who work in Maryland pay tax to the jurisdiction where they work.

County-by-County Rate Variations for 2026

For 2026, local income tax rates vary significantly across Maryland’s 23 counties and Baltimore City. Montgomery County and Baltimore City typically have the highest rates at 3.20%. Lower-tax counties like Worcester assess rates around 2.25%. These rates are set by local governments and can change annually. A consolidated view of county-level changes is maintained in this Maryland local income tax rate summary.

| County/City | 2026 Local Rate | Combined Top Rate |

|---|---|---|

| Montgomery County | 3.20% | 8.95% |

| Baltimore City | 3.20% | 8.95% |

| Prince George’s County | 3.20% | 8.95% |

| Anne Arundel County | 2.81% | 8.56% |

| Howard County | 3.20% | 8.95% |

| Worcester County | 2.25% | 8.00% |

Withholding Obligations for Maryland Employers

CPAs advising Maryland businesses must ensure proper withholding for both state and local taxes. Employers must withhold based on the employee’s county of residence, not the work location. This creates administrative complexity for businesses with employees across multiple counties. Maryland Form MW507 captures this information.

For remote workers who moved during 2026, special rules apply. The local tax is based on residence as of December 31, 2026. Therefore, an employee who moved from Montgomery County to Worcester County in November would owe Worcester County rates for the entire year, potentially requiring year-end withholding adjustments.

Special Local Tax Considerations for Nonresidents

Nonresidents who earn income from Maryland sources must pay local income tax to the jurisdiction where the income was earned. For example, a Virginia resident working in Montgomery County owes Montgomery County local tax but may claim a credit on their Virginia return. Understanding these reciprocity rules is essential for business owners with cross-border operations.

Pro Tip: Maryland’s local tax structure creates planning opportunities. High earners considering relocation within Maryland should evaluate county tax rate differentials as part of their decision.

How Does Maryland Conform to Federal Tax Law Changes?

Quick Answer: Maryland generally conforms to federal AGI but decouples from many federal deductions and credits. CPAs must track both systems separately for accurate compliance.

Maryland’s conformity to federal tax law is selective, creating both challenges and opportunities for CPAs. For 2026, Maryland starts with federal adjusted gross income (AGI) but requires numerous additions and subtractions. This selective conformity approach means that federal tax planning strategies don’t automatically translate to Maryland tax savings.

Key Federal Provisions Maryland Does Not Follow

Maryland has decoupled from several major federal provisions. The state does not conform to the expanded Section 179 expensing limits under the OBBBA. Maryland caps Section 179 at $25,000, significantly lower than the federal limit. This creates timing differences that CPAs must track for depreciation schedules.

Additionally, Maryland does not recognize the federal deduction for qualified business income (QBI) under Section 199A. Pass-through entity owners receive no state-level benefit from this deduction, making entity structure planning more complex in Maryland compared to conforming states.

2026 SALT Deduction Cap Impact on Maryland Taxpayers

For 2026, the federal state and local tax (SALT) deduction cap remains at $40,000 for joint filers and $20,000 for separate filers. This significantly impacts Maryland residents, particularly those in high-tax counties. A Montgomery County couple with $400,000 in income could pay over $30,000 in combined state and local tax, limiting their federal deduction to $40,000 even if they also pay substantial property taxes.

According to recent IRS data, approximately 45% of 2026 filers have claimed the expanded Working Families Tax Cuts. However, Maryland has not conformed to several of these provisions, creating federal-state calculation differences that CPAs must navigate carefully.

Maryland Addition and Subtraction Modifications

Maryland requires taxpayers to add back certain federal deductions and subtract certain Maryland-specific benefits. Common additions include Section 179 depreciation exceeding Maryland limits and income from U.S. government obligations. Subtractions include Social Security benefits (to the extent taxable federally) and certain retirement income for taxpayers over age 65.

For 2026, practitioners should pay special attention to the treatment of remote work income. Maryland has issued guidance clarifying that income earned while working remotely from Maryland is Maryland-source income, even if the employer is located elsewhere. This affects both resident and nonresident filers.

What Are the 2026 Filing Requirements and Deadlines?

Quick Answer: Maryland personal income tax returns for 2026 are due April 15, 2027. Extensions to October 15, 2027, are available but don’t extend the payment deadline.

Maryland’s filing requirements generally align with federal deadlines, but there are important differences. For the 2026 tax year, Maryland residents must file Form 502 by April 15, 2027. Nonresidents earning Maryland income file Form 505. Part-year residents use Form 502/505 combination returns.

Electronic Filing Mandates for Tax Professionals

Maryland requires electronic filing for paid preparers who file more than 100 Maryland returns annually. For 2026, the threshold remains at 100 returns. Practitioners exceeding this threshold must use approved Maryland e-file software. The Maryland Comptroller maintains a list of authorized providers on their website.

Penalties for failure to e-file when required can be substantial. CPAs should track their Maryland filing volume carefully and implement e-file procedures well before reaching the threshold. Many practitioners choose to e-file all Maryland returns regardless of volume to ensure compliance and improve efficiency.

Estimated Tax Payment Requirements

Maryland requires estimated tax payments if the expected tax liability exceeds $1,000 after withholding credits. For 2026, quarterly estimated payments are due April 15, June 15, September 15, 2026, and January 15, 2027. Maryland does not allow annualized income installments, unlike federal rules, so taxpayers with uneven income throughout the year may face underpayment penalties.

Safe harbor rules allow taxpayers to avoid penalties by paying 110% of the prior year’s tax (90% if prior year AGI was under $150,000). For high-income Maryland residents in counties with the 3.20% local rate, this can mean substantial quarterly payments. Proactive tax advisory services help clients manage cash flow while maintaining compliance.

Extension and Amendment Procedures

Maryland grants automatic six-month extensions to October 15, 2027, for 2026 returns. No separate extension request is required if the taxpayer has a federal extension. However, the extension applies only to filing, not to payment. Interest accrues on unpaid tax from the original April 15 due date at Maryland’s statutory rate.

Amended returns use Form 502X and must be filed within three years of the original due date or two years from the date tax was paid, whichever is later. CPAs should maintain thorough documentation supporting all amendments, as Maryland has increased audit activity in recent years despite federal IRS workforce reductions.

What Deductions and Credits Are Available for Maryland Taxpayers?

Quick Answer: Maryland offers targeted credits for earned income, childcare, and biotechnology investment. The state standard deduction is 15% of federal AGI with a minimum of $1,550 and maximum of $2,400.

Maryland’s deduction and credit structure differs significantly from the federal system. Understanding these provisions is essential for CPAs to maximize tax savings for clients. For 2026, several credits offer substantial benefits for qualifying taxpayers.

Maryland Standard and Itemized Deductions

Unlike the federal system with fixed standard deduction amounts, Maryland calculates its standard deduction as 15% of federal AGI, subject to a floor of $1,550 and a ceiling of $2,400 for single filers. Joint filers have a floor of $3,100 and ceiling of $4,850. This formula-based approach means that as income increases, the Maryland standard deduction provides less relative benefit.

Maryland allows itemized deductions but doesn’t automatically follow federal itemized deduction calculations. The state requires separate schedules for mortgage interest, charitable contributions, and medical expenses. Notably, Maryland’s medical expense threshold differs from the federal 7.5% AGI floor, creating another calculation difference.

Earned Income Tax Credit and Refundable Credits

Maryland offers an earned income tax credit equal to 50% of the federal EITC for 2026. This refundable credit provides significant benefits for lower-income working families. CPAs should ensure all eligible clients claim this credit, as it can result in substantial refunds even for taxpayers with little or no Maryland tax liability.

The state also offers a refundable child and dependent care credit. For 2026, this credit is based on a percentage of qualifying expenses, with the percentage varying by income level. Unlike the federal credit, Maryland’s version remains refundable, providing benefits even to taxpayers with no tax liability.

| Credit Type | 2026 Benefit | Refundable |

|---|---|---|

| Earned Income Credit | 50% of federal EITC | Yes |

| Child Care Credit | 32% of expenses (income-based) | Yes |

| Biotechnology Investment Credit | 50% of qualified investment | No |

| Long-Term Care Insurance Credit | Up to $500 per policy | No |

Business and Investment Credits

Maryland offers several business-related credits that CPAs should consider for applicable clients. The biotechnology investment tax credit provides a 50% credit for investments in qualified Maryland biotechnology companies. This credit is particularly valuable for high-income investors seeking Maryland tax reduction strategies.

The One Maryland tax credit incentivizes business investment in economically distressed areas. For 2026, qualifying businesses can claim credits for job creation, property investment, and employee training expenses. These credits have specific certification requirements that must be met before the tax year begins, requiring proactive planning.

How Should CPAs Handle Multi-State Issues for Maryland Clients?

Quick Answer: Maryland residents working in other states face double taxation without reciprocity. Virginia and Pennsylvania have reciprocal agreements; DC, Delaware, and West Virginia do not.

Multi-state taxation is increasingly common for Maryland CPAs due to remote work arrangements and cross-border commuting. Maryland’s location creates unique challenges as many residents work in neighboring jurisdictions. For 2026, understanding reciprocity agreements and credit mechanisms is essential.

Maryland’s Reciprocal Agreements

Maryland maintains reciprocal agreements with Virginia, Pennsylvania, West Virginia, and the District of Columbia. These agreements generally prevent double taxation on wage income. A Maryland resident working in Virginia files only a Maryland return on wage income, while Virginia wages are exempt from Virginia tax. The employee must file Form MW507 with their employer to claim reciprocity.

However, these agreements apply only to wage income. Business income, rental income, and investment income remain taxable in the source state. For self-employed individuals and business owners, multi-state taxation cannot be avoided through reciprocity.

Remote Work and Sourcing Rules

For 2026, Maryland continues to assert taxing authority over income earned by Maryland residents, even if the work is performed remotely for an out-of-state employer. This “convenience of the employer” approach has generated controversy but remains Maryland policy. A Maryland resident working remotely for a New York company owes Maryland tax on 100% of their wages.

Conversely, nonresidents who work remotely from their home state for a Maryland employer generally don’t owe Maryland tax. This creates planning opportunities for businesses considering workforce location strategies. CPAs should document the facts supporting sourcing positions, as these rules face increased scrutiny from state tax authorities.

Credit for Taxes Paid to Other States

When reciprocity doesn’t apply, Maryland residents can claim a credit for income taxes paid to other states. For 2026, this credit is calculated on Schedule CR and is limited to the lesser of the tax actually paid to the other state or the Maryland tax on the same income. The credit applies only to income taxes, not to sales taxes or other levies.

CPAs must carefully allocate income between Maryland and other states to maximize the credit. This requires detailed records of income sources and days worked in each jurisdiction. For high-income clients with complex multi-state situations, comprehensive tax strategy planning using specialized software becomes necessary.

Pro Tip: For Maryland residents considering relocating to a lower-tax state, timing the move for late in the tax year minimizes Maryland’s apportionment claim on year-to-date income.

Uncle Kam in Action: Maryland CPA Saves Client $18,500

Sarah Chen, a Maryland-based CPA with a growing advisory practice, faced a common challenge in early 2026. Her client, Michael Torres, owned a successful consulting business operating as a Maryland S corporation. Michael earned $450,000 annually and lived in Montgomery County, where the combined state and local income tax rate reached 8.95%.

Michael’s previous tax preparer had simply filed returns without strategic planning. For 2025, Michael paid over $40,000 in Maryland income taxes and couldn’t fully deduct his SALT payments on his federal return due to the $40,000 cap. He was frustrated by his tax burden and concerned about cash flow.

Sarah enrolled in Uncle Kam’s tax advisory operating system and immediately identified opportunities. She analyzed Michael’s situation using the MERNA™ framework, focusing on entity structure optimization and retirement planning.

Sarah implemented a three-part strategy. First, she established a defined benefit pension plan for Michael’s S corporation, allowing a $85,000 deductible contribution for 2026. Second, she restructured his reasonable compensation to $180,000, with the remaining $270,000 distributed as S corporation distributions, avoiding the 3.8% Medicare surtax. Third, she maximized Maryland-specific credits, including the long-term care insurance credit.

The results were substantial. Michael’s 2026 combined federal and state tax liability decreased by $18,500. His Maryland tax alone dropped by $6,200 due to the lower AGI from pension contributions. Sarah charged $3,500 for the advisory engagement, delivering a 5.3x first-year return on investment.

Michael now meets with Sarah quarterly for proactive planning, and she’s expanded her advisory practice by 40% since implementing the Uncle Kam system. This success demonstrates how CPAs can transform their practices by moving from compliance to strategy. Learn more about proven client success strategies that generate measurable results.

Next Steps

Maryland state income tax planning requires specialized knowledge and proactive strategies. CPAs who master these complexities can deliver exceptional value to clients while building more profitable advisory practices. Here’s how to take action:

- Review all Maryland client returns for missed credit opportunities.

- Document multi-state income allocation positions thoroughly for 2026.

- Implement quarterly estimated payment monitoring systems for high-income clients.

- Stay current on Maryland legislative changes throughout the year.

- Explore comprehensive tax planning solutions that streamline Maryland compliance.

Frequently Asked Questions

Does Maryland tax Social Security benefits in 2026?

No, Maryland does not tax Social Security benefits for 2026. Taxpayers who include Social Security in federal AGI can subtract it on their Maryland return. This subtraction applies regardless of income level, making Maryland relatively favorable for retirees compared to states that tax Social Security benefits.

What is Maryland’s tax treatment of retirement income in 2026?

Maryland offers a pension exclusion for taxpayers age 65 or older. For 2026, eligible taxpayers can exclude up to $37,900 of qualifying retirement income, including pension, annuity, and IRA distributions. This exclusion is reduced dollar-for-dollar by Social Security benefits excluded. Younger retirees may exclude smaller amounts based on age.

How do Maryland’s pass-through entity tax rules work for 2026?

Maryland allows pass-through entities to elect entity-level taxation. For 2026, this election permits the entity to pay Maryland tax at 5.75%, allowing owners to claim a credit on their individual returns. This election helps high-income owners exceed the federal SALT deduction cap by shifting the deduction to the entity level.

Are there penalties for underpaying Maryland estimated taxes in 2026?

Yes, Maryland assesses interest on underpaid estimated taxes. For 2026, the rate is set quarterly based on federal short-term rates. Penalties can be avoided by paying 110% of prior year tax or 90% of current year tax through withholding and estimates. Maryland does not allow annualized income exceptions.

What documentation should CPAs maintain for Maryland local tax compliance?

CPAs should document client county of residence as of December 31 for each tax year. For clients who moved during 2026, obtain proof of relocation dates and addresses. For multi-state situations, maintain employment contracts, remote work agreements, and day-counting logs. These records are essential if Maryland audits local tax allocation.

How does Maryland’s treatment differ from federal for bonus depreciation?

Maryland has decoupled from federal bonus depreciation provisions. For 2026, Maryland does not allow the immediate expensing of assets that qualify federally. CPAs must maintain separate depreciation schedules for Maryland purposes, typically using 168(g) alternative depreciation system (ADS) lives. This creates significant book-to-tax differences for equipment-intensive businesses.

What audit red flags should CPAs avoid on Maryland returns for 2026?

Common audit triggers include large charitable deductions, non-wage business income without corresponding business expenses, out-of-state income without proper sourcing documentation, and inconsistencies between federal and Maryland AGI. Maryland has enhanced computer matching capabilities, so ensure W-2s, 1099s, and K-1s match exactly between federal and state returns.

Related Resources

- Tax Strategy Insights for CPAs

- Comprehensive State Tax Planning Guides

- The MERNA™ Tax Planning Framework

- Business Advisory Solutions for CPAs

For an at-a-glance reference of rate tables, credits, and local differentials as they evolve, bookmark the central Maryland tax reference hub for advisors.

Last updated: June, 2026

This information is current as of 6/11/2026. Tax laws change frequently. Verify updates with the IRS or Maryland Comptroller if reading this later.

Turn Maryland Tax Complexity Into Scalable Advisory Revenue

Maryland’s layered state and local system creates exactly the type of recurring planning need that supports a year-round advisory model. Uncle Kam equips CPAs and EAs with an integrated AI engine, a 300+ strategy library, and MERNA™ certification so practitioners can productize Maryland-focused planning packages for business owners and high earners. Learn how the Uncle Kam marketplace helps tax pros transition to advisory and plug into a steady flow of warm prospects who already value proactive planning.

Advisors who specialize by state win bigger, stickier client relationships. If the goal is to dominate the Maryland market with premium strategy offers instead of seasonal prep, it helps to have a blueprint. Book a Free Strategy Session with an Uncle Kam growth strategist to map out a Maryland-focused advisory niche, packaging, and pricing plan tailored to the firm’s current capacity and goals.