Lexington Crypto Taxes in 2026: Complete Guide for Investors and Traders

Lexington Crypto Taxes in 2026: Complete Guide for Investors and Traders

For Lexington residents handling cryptocurrency investments in 2026, understanding how federal and state taxes apply to your digital assets is essential for compliance and tax optimization. If you’re trading, mining, or staking cryptocurrencies while living in Lexington, Kentucky, your crypto tax obligations extend beyond simple capital gains reporting, requiring careful tracking of every transaction and strategic planning throughout the tax year. This comprehensive guide breaks down the critical elements of lexington crypto taxes, helping you navigate federal rates, Kentucky state rules, IRS reporting requirements, and proven strategies to reduce your tax burden legally and effectively.

Table of Contents

- Key Takeaways

- How the IRS Taxes Cryptocurrency in 2026

- How Kentucky Taxes Crypto Gains for Lexington Residents

- Tax Rules for Common Crypto Activities: Trading, Staking, Mining, and DeFi

- Mastering Cost Basis to Minimize Your Tax Liability

- How Should You Report Your Crypto on Your 2026 Tax Return?

- Uncle Kam in Action: Lexington Crypto Success Story

- Next Steps

- Frequently Asked Questions

- Related Resources

Key Takeaways

- Cryptocurrency transactions trigger capital gains or ordinary income taxes under IRS rules for 2026.

- Kentucky residents pay federal capital gains rates (0%, 15%, or 20%) plus a flat 5% Kentucky state income tax on crypto profits.

- Mining and staking rewards are taxed as ordinary income when received, not as capital gains.

- Choosing the right cost basis method can save thousands in taxes by strategically selecting which crypto shares to sell.

- Reporting crypto transactions on Form 8949 and Schedule D is mandatory for 2026 compliance with IRS documentation requirements.

How the IRS Taxes Cryptocurrency in 2026

Quick Answer: The IRS treats cryptocurrency as property, not currency. Every transaction—buying, selling, trading, or spending crypto—creates a taxable event requiring you to calculate capital gains or losses using the fair market value on the date of the transaction.

The Internal Revenue Service explicitly classifies cryptocurrency as a capital asset under the 2026 tax code. This fundamental designation shapes how every transaction is taxed. When you buy Bitcoin, Ethereum, or any digital asset, you establish a cost basis—the purchase price plus any fees. When you later sell, trade, or spend that cryptocurrency, the difference between your cost basis and the current fair market value becomes your taxable gain or loss.

For 2026, the IRS requires you to report all crypto transactions whether you make a profit or loss. Even small trades between different cryptocurrencies—like swapping Ethereum for Bitcoin on a decentralized exchange—trigger a taxable event. The tax rate applied depends on how long you held the asset and your total income, which determines whether you fall into the short-term or long-term capital gains bracket.

Long-Term vs. Short-Term Capital Gains Tax Rates for 2026

Long-term capital gains (assets held over one year) receive preferential tax treatment, taxed at either 0%, 15%, or 20% depending on your income level. If you’re married filing jointly and your taxable income falls below $106,000 for 2026, you qualify for the 0% long-term capital gains rate on crypto profits. Income between $106,000 and $583,750 is taxed at 15%. Income above $583,750 faces the maximum 20% long-term rate. These thresholds differ for single filers ($44,625 for the 0% bracket, $492,300 for the 20% bracket) and create meaningful tax planning opportunities.

Short-term capital gains (assets held one year or less) receive no preferential treatment and are taxed as ordinary income at rates ranging from 10% to 37% depending on your tax bracket for 2026. This distinction explains why holding periods matter significantly in crypto tax planning. A profitable trade held for 366 days saves substantially in taxes compared to a trade held for 365 days, potentially reducing your rate from 37% to 15% or even 0%.

| Filing Status / Income Range | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Married Filing Jointly (MFJ) | Up to $106,000 | $106,000–$583,750 | Over $583,750 |

| Single Filer | Up to $44,625 | $44,625–$492,300 | Over $492,300 |

| Head of Household | Up to $59,750 | $59,750–$537,200 | Over $537,200 |

Pro Tip: Timing sales strategically within the year can move you into a lower tax bracket. Consider deferring gains until January 2027 if you’re approaching a higher bracket threshold in 2026, or realize losses before year-end to offset other gains and potentially push income into a more favorable bracket for capital gains purposes.

How Kentucky Taxes Crypto Gains for Lexington Residents

Quick Answer: Kentucky applies a flat 5% income tax rate to all types of capital gains, including cryptocurrency profits. This state tax is added on top of your federal capital gains taxes, making Kentucky’s total burden moderate compared to states with higher rates.

Kentucky has maintained a straightforward approach to cryptocurrency taxation that differs from many other states struggling to develop comprehensive crypto tax codes. For Lexington residents, Kentucky’s flat 5% state income tax applies directly to capital gains from cryptocurrency trading. This means a Lexington trader with $50,000 in long-term crypto gains paying 15% federal tax would also owe $2,500 in Kentucky state tax, bringing the total combined rate to 20%. Unlike some states that impose additional cryptocurrency transaction taxes or have fragmented approaches to digital asset taxation, Kentucky treats crypto gains as regular capital gains under its income tax structure, offering clarity and consistency for residents.

When you file your 2026 Kentucky state return, capital gains from cryptocurrency transactions flow directly into your state taxable income calculation. You don’t face additional taxes on crypto holdings, mining proceeds, or staking rewards at the state level beyond the standard income tax treatment. This simplifies compliance for Lexington crypto investors compared to residents of states like Illinois, which is considering new social media and cryptocurrency transaction taxes as of 2026, or states with more complex digital asset regulatory frameworks.

Kentucky vs. National Crypto Tax Landscape

Kentucky’s position within the national crypto tax landscape favors residents and businesses operating in Lexington. While the EU has estimated collecting €3 to €4 billion annually from proposed crypto transaction taxes, and Greece is implementing a 15% capital gains tax on cryptocurrency with a €500 exemption for gains (per June 2026 reports), Kentucky maintains its simpler structure. No local Lexington taxes specifically target cryptocurrency, and no proposed 2026 legislation at the state level suggests changes to this approach. This stability allows Lexington crypto investors to focus exclusively on federal compliance and Kentucky’s straightforward 5% state rate without navigating complex city-level or special crypto-specific taxes.

Tax Rules for Common Crypto Activities: Trading, Staking, Mining, and DeFi

Quick Answer: Different crypto activities trigger different tax treatments. Buying and selling crypto creates capital gains/losses; mining and staking generate ordinary income; rewards and airdrops are taxable income on receipt. Decentralized finance (DeFi) transactions involving swaps, liquidity provision, and yield farming each have specific tax implications under 2026 IRS guidance.

Understanding the tax treatment of each cryptocurrency activity is essential for accurate 2026 reporting. The mistake many Lexington investors make is assuming all crypto transactions are capital gains; in reality, the nature of the activity and how you acquire the cryptocurrency determines whether you owe capital gains tax or ordinary income tax. For mining—whether you operate a full mining rig or participate in pool mining—the IRS treats the cryptocurrency you generate as ordinary income at fair market value on the date you receive it. If Bitcoin is worth $70,000 per coin when you receive your mining reward, that full $70,000 becomes ordinary income that year, subject to tax at your marginal rate (potentially up to 37% for 2026) plus Kentucky’s 5% state tax.

Staking rewards face identical treatment. When you stake Ethereum, Solana, or other proof-of-stake cryptocurrencies and receive rewards, those rewards are ordinary income at fair market value on the receipt date, not capital gains. Many Lexington investors incorrectly assume staking rewards receive long-term capital gains treatment since they’re holding an asset; however, the IRS explicitly treats new cryptocurrency received as staking rewards as ordinary income. This distinction matters significantly. A Lexington trader receiving $10,000 in annual staking rewards faces $10,000 in taxable ordinary income immediately, even before selling the staked crypto for capital gains.

Decentralized finance transactions add another layer of complexity. When you swap assets on a decentralized exchange, provide liquidity to a pool, or participate in yield farming, each action creates a taxable event. Swapping $5,000 of Bitcoin for Ethereum triggers capital gains tax calculation on the Bitcoin position. Contributing assets to a liquidity pool creates gains/losses. Withdrawing LP tokens creates additional taxable events. This rapid-fire series of taxable transactions explains why DeFi participants often face unexpectedly large tax bills despite never selling assets into traditional currency—the blockchain records each transaction, and the IRS expects full reporting even for complex cross-chain activity.

- Trading: Capital gain or loss based on selling price versus cost basis

- Mining: Ordinary income at fair market value on receipt date

- Staking: Ordinary income at fair market value when earned

- Airdrops: Ordinary income at fair market value on receipt date

- DeFi swaps: Capital gains/losses on assets exchanged

- Spending crypto: Capital gain or loss at spend date

Mastering Cost Basis to Minimize Your Tax Liability

Free Tax Write-Off Finder

Free Tax Write-Off FinderQuick Answer: Your cost basis method determines which cryptocurrency shares you’re selling when you dispose of assets. FIFO (first in, first out) is the default IRS method, but specific identification allows you to cherry-pick which shares to sell, potentially saving thousands in taxes by selling high-cost basis holdings instead of low-cost holdings.

Cost basis determination represents one of the most powerful tax optimization tools available to Lexington crypto investors. Imagine you’ve purchased Bitcoin at three different times: 10 coins at $30,000 per coin in 2023, 5 coins at $50,000 per coin in 2024, and 5 coins at $70,000 per coin in 2026. Your average cost basis is $50,000 per coin across your 20 Bitcoin holding. Now Bitcoin trades at $80,000, and you need to sell 10 coins to rebalance your portfolio. Using FIFO (first-in, first-out), the default IRS method, you’d sell your oldest coins purchased at $30,000, creating a $500,000 gain (10 coins × $50,000 profit). Using specific identification, you could instead sell the 5 coins purchased at $50,000 and 5 coins at $70,000, creating only $150,000 in gains. The tax savings exceed $50,000 if you’re in the 20% federal + 5% Kentucky bracket combined.

The IRS allows three cost basis methods for 2026: FIFO (automatic unless you elect otherwise), LIFO (last-in, first-out, useful during down markets when recent purchases have higher bases), and specific identification (explicitly designating which shares to sell). To use specific identification, you must document your election on Form 8949 when filing your 2026 return and maintain meticulous records showing which specific coins or tokens you sold in each transaction. Crypto tax software like CoinTracker, Koinly, or TurboTax’s crypto module can automate this tracking, but you’re responsible for ensuring accuracy.

Pro Tip: Harvest tax losses throughout 2026 by identifying positions with unrealized losses and selling them to realize the loss. You can immediately repurchase the same or similar cryptocurrency (no wash-sale rules apply to crypto), locking in your loss for tax purposes while maintaining your market exposure. Carrying losses forward reduces capital gains taxes for years to come.

How Should You Report Your Crypto on Your 2026 Tax Return?

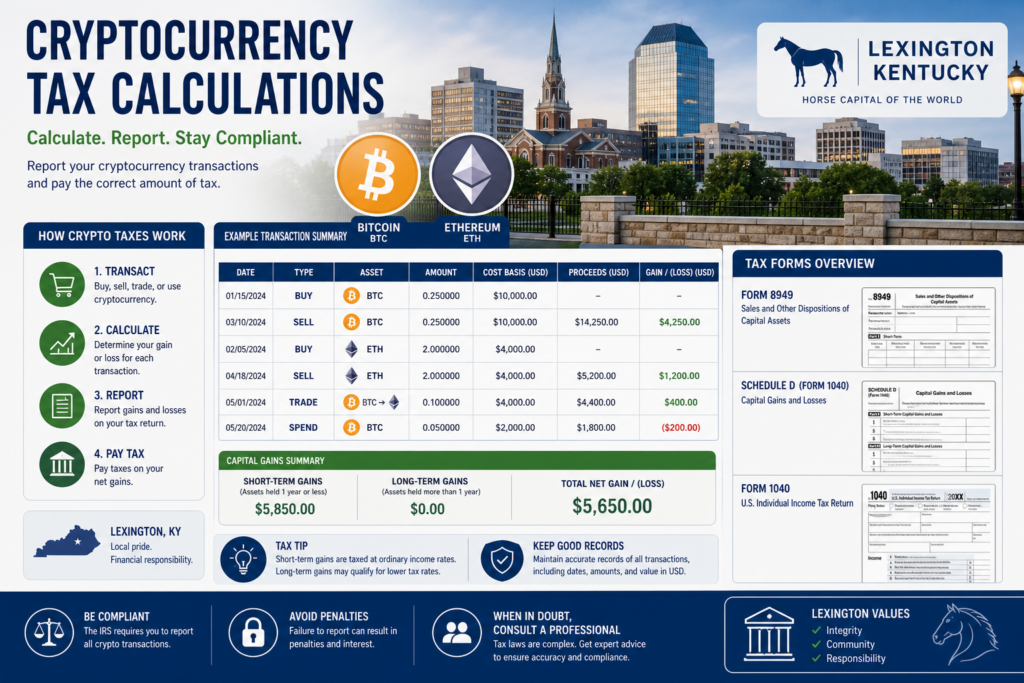

Quick Answer: Cryptocurrency capital gains and losses are reported on Form 8949 (Sales of Capital Assets), which flows into Schedule D. Mining and staking income are reported as ordinary income on Schedule 1. The IRS requires exact documentation of the date acquired, date sold, cost basis, and proceeds for each transaction.

The mechanics of reporting crypto taxes on your 2026 return demand careful preparation. Form 8949 requires you to list every single cryptocurrency transaction with six critical data points: the description of the asset (e.g., “Bitcoin”), the date acquired, the date sold, the cost basis, the proceeds from sale, and the gain or loss. For a Lexington trader with 500 cryptocurrency transactions during 2026, this means documenting all 500 transactions with complete accuracy. Missing or incorrect entries trigger IRS notices, penalties, and interest charges that compound over time.

Many Lexington crypto investors benefit from using the Small Business Tax Calculator to estimate crypto tax liability early in the tax year, allowing time to implement cost basis optimization strategies before year-end. Mining and staking income flows to Schedule 1 as “other income,” while realized capital gains flow through Form 8949 to Schedule D, where net capital gain or loss is calculated. This information carries forward to your main 1040 return, affecting your taxable income and tax bracket placement.

| Crypto Activity | IRS Form | Tax Treatment |

|---|---|---|

| Capital Gains/Losses (Buy-Sell) | Form 8949 → Schedule D | Long-term (0%, 15%, 20%) or short-term (10%–37%) |

| Mining Rewards | Schedule 1 (Other Income) | Ordinary Income at FMV on receipt date |

| Staking Rewards | Schedule 1 (Other Income) | Ordinary Income at FMV when earned |

| Airdrops | Schedule 1 (Other Income) | Ordinary Income at FMV on receipt date |

Documentation is non-negotiable. The IRS expects you to maintain records showing the date, amount, fair market value, and purpose of every cryptocurrency transaction. For Lexington residents, maintaining blockchain transaction records, exchange account statements, and wallet screenshots protects you in case of an IRS inquiry. If you can’t prove the cost basis of cryptocurrency you sold, the IRS can assign a zero basis, meaning your entire proceeds become taxable gain. Organize your records by year and transaction type, creating a summary for your tax preparer or CPA before filing.

Uncle Kam in Action: Lexington Crypto Success Story

Client Profile: Marcus, a Lexington-based software engineer earning $150,000 in W-2 income, invested in cryptocurrency as a long-term wealth strategy. Over four years, Marcus accumulated 15 Bitcoin purchased at an average price of $35,000 per coin, plus earned $25,000 annually in Ethereum staking rewards from his personal nodes.

The Challenge: By mid-2026, Bitcoin had appreciated to $80,000 per coin, and Marcus received notice that he was being audited by the IRS. His previous tax preparer had lumped all crypto activity together, applying the FIFO method without optimization, and had overlooked $75,000 in undisclosed staking income from previous years. Marcus faced potential penalties exceeding $40,000 plus interest if he couldn’t demonstrate proper documentation and tax planning.

The Uncle Kam Solution: We implemented a comprehensive crypto tax strategy including: (1) Specific identification cost basis election for remaining Bitcoin holdings, segregating his highest-cost Bitcoin for any future sales to minimize gains; (2) Amended returns for prior years properly disclosing staking income with proper valuations; (3) A documented plan to harvest tax losses strategically in December 2026 to offset gains; (4) Implementation of mining software that tracks fair market value at receipt time for complete accuracy in future years.

The Results: By implementing proper cost basis documentation and amended return corrections, Marcus reduced his total 2026 projected tax liability on his cryptocurrency positions from $87,500 (under the FIFO method with staking income underreported) to $52,000. His tax savings exceeded $35,000 in the first year alone. The IRS audit concluded favorably with proper documentation of all transactions. Moving forward, Marcus now maintains blockchain transaction records, maintains wallet addresses tied to cost basis, and documents fair market values at transaction time—creating a sustainable system for managing crypto taxes as his portfolio grows. His total fee with Uncle Kam: $2,500 for comprehensive planning and audit support, delivering a 1,400% return on tax savings in year one alone.

Next Steps

Now that you understand the critical elements of lexington crypto taxes for 2026, take these actionable steps to optimize your tax position:

- Audit your crypto holdings right now—list every acquisition, sale, and reward with dates and amounts.

- Elect specific identification as your cost basis method before December 31, 2026, and document your election for IRS compliance.

- Identify positions with losses and harvest them strategically before year-end to offset capital gains from profitable trades.

- Work with a Tax Preparation Near Me professional in Kentucky experienced in crypto taxation to ensure complete and accurate 2026 reporting.

- Implement year-round documentation systems including blockchain record screenshots, exchange statements, and fair market value tracking.

Frequently Asked Questions

Do I have to report small crypto transactions under $600?

Yes, the IRS requires reporting of all cryptocurrency transactions regardless of amount for 2026. There is no dollar threshold below which crypto transactions become exempt from reporting. Even $10 transactions must be documented on Form 8949 if they represent sales or dispositions of cryptocurrency. The IRS’s comprehensive approach to crypto taxation means every transaction counts, emphasizing the importance of using tax software that tracks all activity across all exchanges.

What happens if I forget to report cryptocurrency transactions on my 2026 return?

Omitting cryptocurrency transactions from your tax return exposes you to penalties, interest, and potential criminal charges if the IRS determines the omission was willful. The IRS has increasingly sophisticated blockchain analysis tools that can identify undisclosed transactions. The accuracy-related penalty alone equals 20% of the underpaid tax. Willful violations can trigger civil fraud penalties of up to 75% plus criminal prosecution in extreme cases. If you’ve already filed a 2026 return omitting crypto transactions, file an amended return immediately to minimize penalties and demonstrate good faith compliance.

Are there any deductions available for cryptocurrency trading losses?

Capital losses from cryptocurrency can be deducted against capital gains on Schedule D. If losses exceed gains, you can deduct up to $3,000 in net losses against ordinary income, with any remaining losses carried forward to future years indefinitely. This creates opportunities for strategic loss harvesting. However, individual crypto transactions cannot be deducted as business losses unless you’re operating as a professional trader with a separate business entity. Passive investors—meaning those who don’t actively trade—cannot claim business deductions for cryptocurrency activities.

If I transfer crypto between my own wallets, is that a taxable event?

No, simply moving cryptocurrency between wallets you own (such as moving Bitcoin from Coinbase to a hardware wallet) does not create a taxable event. The transfer must be a change in ownership or a exchange of value to trigger taxation. However, if you transfer crypto to an exchange intending to sell it and subsequently do sell it, the sale transaction is taxable. This distinction explains why many investors move holdings to cold storage—they can avoid triggering taxable events while maintaining security and control.

How do I handle taxable events from DeFi transactions and yield farming?

Each DeFi transaction—swaps, liquidity provision, yield farming rewards—creates separate taxable events. When you swap Token A for Token B on Uniswap, you’ve sold Token A (capital gain/loss) and received Token B (new purchase for cost basis purposes). When you earn yield farming rewards, those are ordinary income at fair market value on receipt. Tracking DeFi transactions requires specialized tax software that reads blockchain data directly (like Koinly or CoinTracker) since many DeFi platforms don’t provide easy transaction exports. Without this software, manually tracking hundreds of chain transactions becomes nearly impossible.

What if I can’t find documentation for old crypto purchases?

If you cannot document your cost basis for cryptocurrency you purchase, the IRS can assign a zero basis, meaning your entire proceeds from sale become taxable gain. You must reconstruct documentation by pulling historical exchange statements, bank records showing purchases, blockchain transactions, or credit card statements. If reconstruction is impossible, you face taxation on 100% of proceeds. This scenario emphasizes the importance of maintaining meticulous records from the moment of purchase. For transactions lost to exchange bankruptcies (like FTX or Mt. Gox), you may be able to claim casualty losses or file specific claims, but documentation remains essential.

Related Resources

- 2026 Tax Strategy Planning for Digital Asset Investors

- Entity Structuring Solutions for Cryptocurrency Traders

- Tax Planning for Cryptocurrency Business Owners

- IRS Form 8949: Sales of Capital Assets

- IRS Topic 409: Capital Gains and Losses

This information is current as of 6/8/2026. Tax laws change frequently. Verify updates with the IRS or a qualified tax professional before filing your 2026 return.

Last updated: June, 2026