IRS CP2000 Notice: 2026 Response Guide for Tax Pros

An IRS CP2000 notice lands on your client’s desk, and the phone rings within minutes. As a solo practitioner, you know this moment well. The IRS CP2000 notice is one of the most common letters your clients receive. Yet it also creates one of your best chances to grow recurring advisory revenue. This 2026 guide shows you how to respond fast, protect your clients, and turn notice work into a scalable service. Our Florida tax preparation team handles these daily.

Table of Contents

- Key Takeaways

- What Is an IRS CP2000 Notice?

- How Do You Respond to a CP2000 Notice?

- How Do You Dispute a CP2000 Notice Effectively?

- What Penalties Come With a CP2000 Notice?

- How Does the New AEP Program Affect Penalties?

- How Can You Turn CP2000 Work Into Recurring Revenue?

- Uncle Kam in Action

- Related Resources

- Next Steps

- Frequently Asked Questions

Key Takeaways

- A CP2000 notice is a proposed change, not a bill or an audit.

- Clients get 30 days to respond, so speed matters.

- The accuracy-related penalty can add 20% of the underpayment.

- The new 2026 AEP program waives some penalties automatically.

- Notice resolution can become steady advisory revenue for solo firms.

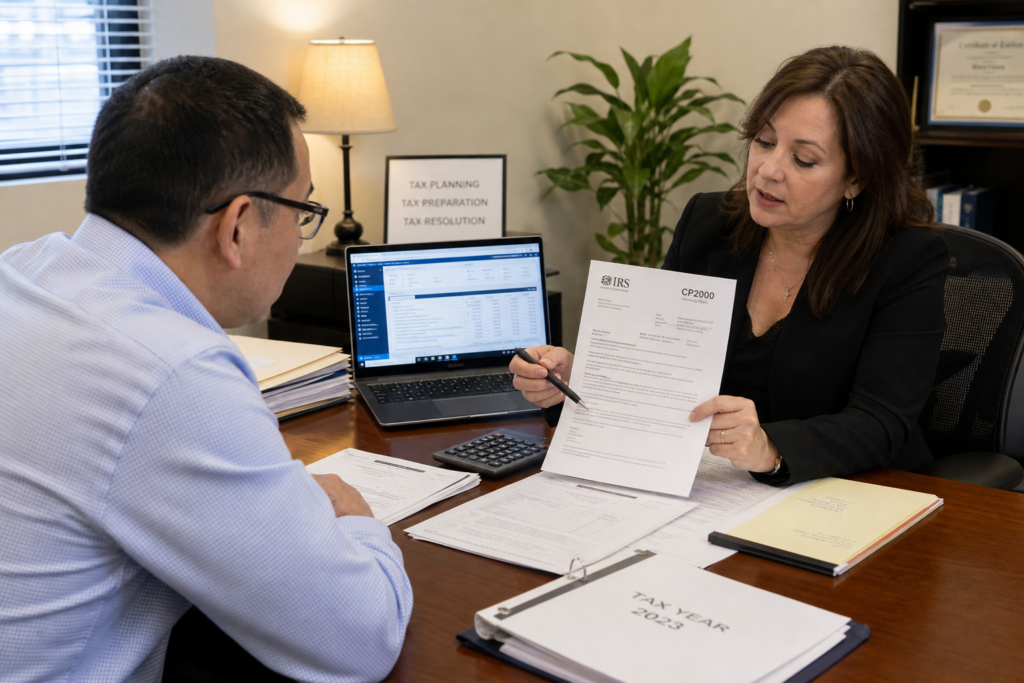

What Is an IRS CP2000 Notice?

Quick Answer: A CP2000 notice proposes changes to a return. It happens when reported income does not match third-party data. It is not an audit.

The IRS CP2000 notice comes from the Automated Underreporter (AUR) system. This system compares your client’s return against forms like W-2s, 1099s, and 1098s. When the numbers do not match, the IRS sends a notice. As a result, many clients panic and assume they are being audited. However, that is not true. The IRS CP2000 notice simply flags a mismatch and proposes a fix.

For solo practitioners, this distinction matters a lot. You can calm the client quickly. Furthermore, you can frame your response as a protective service. The official IRS CP2000 page explains the basic process clearly. Still, most clients need a professional to translate it.

Why Clients Receive This Notice

Most CP2000 notices start with missing income. For example, a freelancer forgets a 1099-NEC. Or an investor omits a brokerage 1099-B. In addition, retirement distributions and gig income often trigger these letters. Many of your self-employed and 1099 clients face this issue every year.

- Unreported 1099-NEC or 1099-K income

- Missing brokerage or dividend statements

- Omitted retirement account distributions

- Duplicate or mismatched employer filings

How the Notice Differs From an Audit

An audit reviews your client’s whole return. A CP2000 notice, by contrast, targets one issue. Therefore, the scope stays narrow. Moreover, the resolution path is faster and less stressful. You simply agree, partly agree, or disagree. Then you send supporting documents.

Pro Tip: Always pull the client’s IRS wage and income transcript first. It reveals every form the IRS has on file.

How Do You Respond to a CP2000 Notice?

Quick Answer: Respond within 30 days. Use the notice response form. Agree, disagree, or partly agree. Then attach clear documentation.

Timing drives everything with a CP2000 notice. Clients get 30 days from the notice date to respond. Those living outside the United States get 60 days. Miss the window, and the IRS issues a Statutory Notice of Deficiency. Consequently, the case becomes far harder to fix. A strong tax filing and compliance process keeps you ahead of these deadlines.

The Three Response Paths

Every CP2000 response follows one of three paths. First, you can agree fully and sign the response. Second, you can disagree and provide proof. Third, you can partly agree when only some items are wrong. In each case, you must be clear and specific.

- Agree: Sign, return, and arrange payment or a plan.

- Disagree: Send a written explanation plus documents.

- Partly agree: Accept some items, dispute the rest.

Documents You Should Gather

Documentation wins CP2000 cases. Therefore, gather everything before you write a word. The IRS wants proof, not opinions. In addition, organized records speed the review. You can find the response steps on the IRS underreporter guidance page.

- Corrected or missing 1099 and W-2 forms

- Brokerage statements showing cost basis

- Receipts tied to disputed deductions

- A signed Form 2848 power of attorney

Pro Tip: Always mail responses by certified mail. The IRS does not confirm receipt otherwise.

How Do You Dispute a CP2000 Notice Effectively?

Quick Answer: Match each proposed change to real evidence. Explain cost basis. Show missing deductions. Then request penalty relief.

Many CP2000 notices overstate the tax owed. That happens because the IRS sees gross proceeds, not net gain. For example, a stock sale of $50,000 may show as full income. Yet the real gain might be only $3,000. As a result, your dispute can slash the proposed balance. This is where smart tax strategy and planning adds huge value.

Common Winning Arguments

Strong disputes rest on facts. Furthermore, they tie each number to a document. Below are the arguments that work most often. Each one can reduce or erase the proposed tax.

- Cost basis reduces reported capital gains

- Business expenses offset unreported 1099 income

- Income already reported on another line

- Duplicate reporting by a payer

When unreported 1099 income appears, self-employment tax often follows. Hyde Park, Florida practitioners can use our Self-Employment Tax Calculator for Hyde Park to estimate the 2026 impact fast.

Building a Clean Response Package

Presentation matters as much as substance. Therefore, organize your package like an examiner would want it. Start with a short cover letter. Next, list each disputed item. Then attach labeled exhibits. This method speeds approval and reduces follow-up letters. Advisory tools help you deliver this at scale. Uncle Kam is an entity-aware tax planning software that models multiple scenarios across 1040s and K-1s at once, so your notice work connects to real strategy.

Did You Know? Many CP2000 notices are wrong or overstated. A documented dispute often cuts the balance sharply.

What Penalties Come With a CP2000 Notice?

Quick Answer: The main risk is the 20% accuracy-related penalty. Interest also accrues on any unpaid tax.

A CP2000 notice often includes a proposed accuracy-related penalty. This penalty equals 20% of the underpayment. It applies to substantial understatements or negligence. Consequently, a $10,000 tax increase can add a $2,000 penalty. On top of that, interest runs from the original due date. You can review the rule on the IRS accuracy-related penalty page.

Penalty Comparison Table

The table below shows the penalties tied to underreporting for 2026. Use it to explain risk clearly to clients.

| Penalty Type | 2026 Rate | Applies When |

|---|---|---|

| Accuracy-related | 20% of underpayment | Negligence or substantial understatement |

| Failure to file | Up to 25% of unpaid tax | Late or missing return |

| Failure to pay | 0.5% per month | Unpaid balance after due date |

How to Request Penalty Relief

You can fight the accuracy-related penalty on two grounds. First, argue reasonable cause with good faith. Second, show the client relied on a professional. In addition, you can point to clean prior compliance. Many of your business owner clients qualify under these rules.

Pro Tip: Always request penalty relief inside the CP2000 response. Do not wait for a separate letter.

How Does the New AEP Program Affect Penalties?

Quick Answer: The 2026 AEP program waives some penalties automatically. It replaces First Time Abate for compliant taxpayers.

In summer 2026, the IRS launched the Automatic Exemption from Penalty (AEP) program. This program waives certain penalties without any request. It applies to failure-to-file, failure-to-pay, and failure-to-deposit penalties. However, it does not cover the accuracy-related penalty tied to a CP2000 notice. Therefore, your dispute skills still matter greatly.

The AEP replaces the old First Time Abate program. It applies to eligible 2025 returns and 2026 quarterly filings. Moreover, it fully replaces First Time Abate for returns due on or after January 1, 2027. You can read the details on the IRS newsroom page.

Who Qualifies for AEP

AEP rewards clean compliance history. Specifically, the taxpayer must have filed and paid on time. This must hold for the three prior years. For quarterly filers, the standard is 12 consecutive quarters. As a result, most steady clients now qualify automatically.

AEP vs. First Time Abate vs. Reasonable Cause

| Relief Type | Request Needed? | Best For |

|---|---|---|

| AEP (2026) | No, automatic | Compliant repeat filers |

| First Time Abate | Yes, during transition | Clean 3-year history |

| Reasonable Cause | Yes, always | Illness, disaster, reliance |

During 2026, some clients may still get penalty notices as systems shift. In those cases, request First Time Abate under the old process. The National Taxpayer Advocate estimates 1.5 million taxpayers could benefit yearly. That is up from about 220,000 under the manual system. Guiding clients through ongoing advisory relationships keeps them protected.

Did You Know? The AEP does not touch the CP2000 accuracy penalty. Your dispute work remains essential.

How Can You Turn CP2000 Work Into Recurring Revenue?

Quick Answer: Package notice resolution with proactive planning. Then convert one-time clients into monthly advisory retainers.

A CP2000 notice is a doorway, not a dead end. Your client is scared and grateful when you fix it. That moment is your best chance to sell advisory. Furthermore, the pain that caused the notice usually signals deeper issues. Missing income often means missing planning. Therefore, you can offer a full review. This is exactly why so many practitioners learn how the Uncle Kam marketplace helps tax pros transition to advisory.

Build a Notice Resolution Service Tier

Solo practitioners need leverage, not longer hours. So create a fixed-fee notice resolution package. Then add a follow-up planning engagement. This turns reactive work into predictable revenue. In addition, it raises your value in the client’s eyes.

- Flat-fee CP2000 response and dispute

- Quarterly compliance and estimated tax review

- Annual proactive tax planning session

- Monthly advisory retainer for ongoing needs

Use Systems to Scale Representation

You cannot scale by working harder. Instead, you scale with systems and repeatable processes. Templates, checklists, and software handle the heavy lifting. As a result, you serve more clients with less stress. Ready to build a real advisory engine? Book a strategy session with Uncle Kam to map your plan. You can also study proven models in our client results library.

Pro Tip: Price notice resolution as a package, not hourly. Value pricing lifts both trust and profit.

Uncle Kam in Action: How a Solo CPA Turned a Notice Into a Retainer

Client Snapshot: Maria runs a one-person tax firm in Florida. She serves freelancers and small business owners. Like many solo pros, she wore every hat and felt stuck.

Financial Profile: Her firm earned about $140,000 in annual revenue. Most of that came from seasonal tax prep. Advisory income was almost zero.

The Challenge: One client, a gig-economy driver, received a CP2000 notice. The IRS proposed $14,000 in extra tax. It also added a 20% accuracy-related penalty of $2,800. The client panicked and called Maria in tears. She fixed notices often, yet never charged well for them.

The Uncle Kam Solution: Maria joined Uncle Kam and used its planning system. First, she pulled the client’s wage and income transcript. Then she documented business mileage and expenses. As a result, the real tax owed dropped to just $2,100. She also requested reasonable-cause penalty relief and won. Next, she used the MERNA framework to spot bigger savings. She proposed an S Corp election and a retirement plan.

The Results: Maria charged a $1,500 flat fee for the notice resolution. She then closed a $6,000 annual advisory engagement. Her client saved over $11,900 in tax and penalties that year. Furthermore, the planning uncovered $9,000 in future annual savings.

- Tax Savings: $11,900 in year one

- Investment: $1,500 notice fee plus $6,000 advisory

- ROI: Over 2.7x return in the first year

Within six months, Maria added eight advisory retainers. See more stories like this in our documented client results.

Related Resources

- Proactive Tax Strategy Services

- The MERNA Method Framework

- Uncle Kam Tax Strategy Blog

- Self-Employed Tax Solutions

Next Steps

Ready to turn notice work into steady revenue? Take these clear actions this week. For a full roadmap, learn how the Uncle Kam network equips tax pros with AI software, MERNA certification, and warm leads.

- Build a fixed-fee CP2000 resolution package today.

- Create a reusable response and documentation template.

- Add a follow-up advisory offer after every notice.

- Book a free strategy session to scale your firm.

This information is current as of 7/14/2026. Tax laws change frequently. Verify updates with the IRS if reading this later.

Frequently Asked Questions

Is a CP2000 notice an audit?

No, a CP2000 notice is not an audit. It is a proposed change from mismatched income data. The scope stays narrow. Therefore, resolution is usually faster than an audit.

How long do clients have to respond?

Clients get 30 days from the notice date. Those outside the United States get 60 days. Miss the deadline, and the IRS may issue a Notice of Deficiency. As a result, act quickly.

Does the 2026 AEP program cancel CP2000 penalties?

No, the AEP program does not cover accuracy-related penalties. It waives failure-to-file, pay, and deposit penalties only. Consequently, your CP2000 dispute work still matters. You must request relief separately.

What if the CP2000 notice is wrong?

Many notices overstate the tax owed. For example, gross stock proceeds ignore cost basis. So gather documents and disagree in writing. Then attach clear proof for each disputed item.

Can I charge advisory fees after resolving a notice?

Yes, and you should. A resolved notice builds deep trust fast. Therefore, offer proactive planning next. Many solo firms convert these clients into monthly retainers.

What happens if my client missed one quarterly payment?

One missed quarter can break AEP eligibility for quarterly filers. However, reasonable cause relief may still apply. So document the reason and request relief. Prior clean history also helps your case.

Last updated: July, 2026