Columbia Rental Property Audit in 2026: Complete Guide for Montana Landlords

For 2026, Montana landlords face critical decisions regarding the columbia rental property audit process and Montana’s new second-home tax. With the March 20 filing deadline approaching, nearly three-quarters of the state’s rental properties remain unexempted from higher tax rates. This guide explains everything Columbia property owners need to know about 2026 compliance, documentation requirements, and how to avoid potential audits and penalties. Understanding these changes is essential for protecting your investment income and tenant relationships.

Table of Contents

- Key Takeaways

- What Is a Columbia Rental Property Audit in 2026?

- Understanding Montana’s Second-Home Tax and Its Impact on Rentals

- What Are the 2026 Filing Deadlines for Montana Rental Properties?

- How to Prepare Your Columbia Rental Property for a 2026 Audit

- What Are Common Triggers for Montana Rental Property Audits?

- What Are the Tax Implications if Your Property Is Audited?

- Uncle Kam in Action

- Next Steps

- Frequently Asked Questions

Key Takeaways

- Montana’s second-home tax deadline is March 20, 2026 for electronic applications at homestead.mt.gov.

- Unexempted rental properties face up to a 50% increase in property taxes between 2025 and 2026.

- For 2026, maintain detailed records including IRS Schedule E, lease agreements, and expense documentation.

- Over 21,000 Montana landlords have applied for exemptions, but 50,000-55,000 eligible properties exist.

- Standard deduction for 2026 is $31,500 (married filing jointly) and $15,750 (single).

What Is a Columbia Rental Property Audit in 2026?

Quick Answer: A Columbia rental property audit is a review by the Montana Department of Revenue to verify your property meets long-term rental classification standards and that your tax filing is accurate for 2026.

A rental property audit occurs when Montana tax authorities examine your property records, lease agreements, and income reports. These audits verify whether your property truly qualifies as a long-term rental and whether your reported income and expenses match your tax filings with the IRS. For the 2026 tax year, understanding this process is critical because non-compliance can result in significant property tax increases.

The audit process typically examines: occupancy records showing the property was rented 70% or more of the year, lease agreements documenting tenant relationships, annual rental income and expenses reported on your federal tax return, property condition and maintenance documentation, and whether the property qualifies for Montana’s long-term rental exemption under the second-home tax.

How Does the 2026 Audit Process Work in Montana?

When the Montana Department of Revenue initiates an audit, they typically request documentation within 30 days. The department has 21,000 applications from landlords as of February 2026, with determinations made on 9,200 so far. If selected for audit, you’ll provide your records, the department reviews for accuracy, and they issue a determination on your property’s classification. The department can take significantly longer to process paper applications compared to electronic submissions.

Why Are Audits Important for Columbia Landlords in 2026?

Audits protect your property tax rate. Without proper exemption approval, your Columbia rental could see its tax bill increase by up to 50% in 2026. This directly impacts your cash flow and tenant affordability. Additionally, accurate reporting prevents potential legal liability—the Montana Landlords Association notes that landlords worry about discrepancies between exemption applications and IRS filings creating fraudulent charge exposure. Proper preparation eliminates this risk.

Pro Tip: Ensure all information submitted to homestead.mt.gov matches exactly with your IRS Schedule E and federal tax returns to avoid audit complications for 2026.

Understanding Montana’s Second-Home Tax and Its Impact on Rentals

Quick Answer: Montana’s second-home tax applies higher property tax rates to residential properties not classified as primary residences or qualifying long-term rentals, potentially increasing tax bills by 50% for unexempted properties in 2026.

Enacted through Senate Bill 542 and House Bill 231, Montana’s second-home tax restructures residential property taxation. Rather than a single tax rate, the law creates graduated rates based on property use. Owner-occupied homes receive preferential rates. Long-term rentals that meet state requirements qualify for reduced rates. Properties not classified in these categories—including vacation homes and other uses—face significantly higher rates.

How Does This Tax Impact Your Columbia Rental Property?

For Columbia landlords, exemption status is critical. The Montana Department of Revenue analysis indicates unexempted residential properties could see 50% tax increases between 2025 and 2026. For example, a property with a $2,000 annual tax bill in 2025 could face a $3,000 bill in 2026 without exemption. This directly impacts your profitability and may force rent increases that affect tenant retention and market competitiveness.

What Property Uses Qualify as Long-Term Rentals?

Montana law defines long-term rentals as properties rented for residential purposes for at least 70% of the calendar year. The property must have a current lease agreement and be offered for rent continuously. Properties rented seasonally or for brief periods may not qualify. The Montana Landlords Association notes the law doesn’t cover all scenarios, particularly when owners rent rooms on the same property as their primary residence, so consulting the Department of Revenue may be necessary for complex situations.

What Are the 2026 Filing Deadlines for Montana Rental Properties?

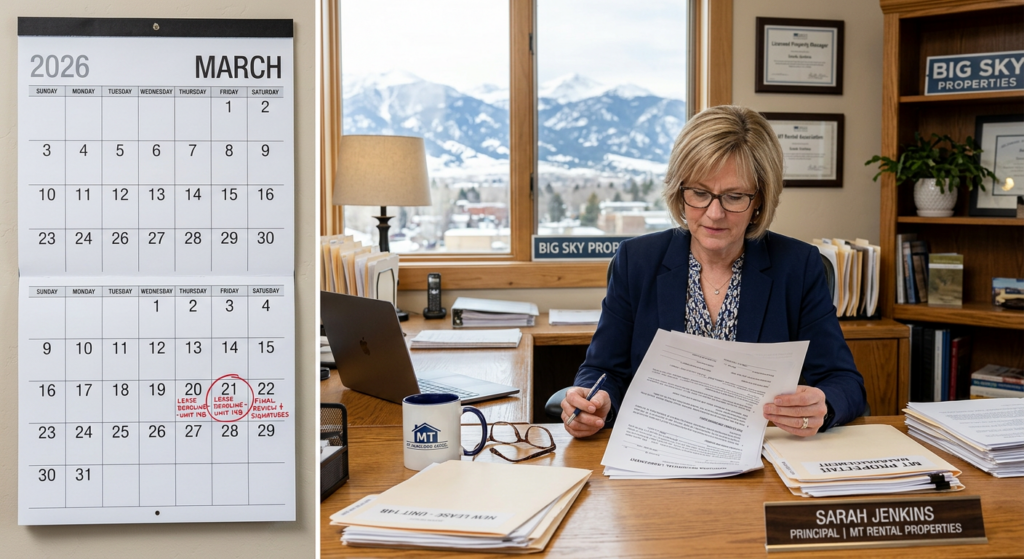

Quick Answer: For 2026, the deadline for Columbia landlords to apply for long-term rental tax exemptions is March 20 for electronic applications and mail-postmark deadline of March 20 for physical applications.

The Montana Department of Revenue extended the original March 1 deadline to March 20, 2026. This extension came after the online portal experienced technical issues from a surge in last-minute filings. Electronic applications must be submitted at homestead.mt.gov by midnight on March 20. Physical applications must be postmarked on or before March 20. Missing this deadline locks you into higher tax rates for the remainder of 2026.

Why the Extended Deadline Matters

The extended deadline gives Columbia landlords additional time to gather documentation and submit applications. As of late February 2026, the department had processed determinations on only 9,200 of 21,000+ received applications, with approximately 4,000 additional filings arriving in just one week. This indicates landlords are waiting until the deadline, which means processing times may extend beyond the application deadline. Submit early to avoid late-processing issues.

How to Apply for the Exemption

Visit homestead.mt.gov and complete the long-term rental application form. The form requests annual rental income, annual expenses, and monthly rent amounts. Have your lease agreement and financial records ready. The application process is straightforward, but accuracy is critical. Tenants can also verify their landlord’s application status using the department’s lookup tool on the revenue department website, providing transparency into the process.

| Deadline Checkpoint | Date | Action Required |

|---|---|---|

| Electronic Application Deadline | March 20, 2026 (midnight) | Submit at homestead.mt.gov |

| Paper Application Postmark Deadline | March 20, 2026 | Mail application to revenue department |

| Federal Tax Filing Deadline | April 15, 2026 | File 2025 tax return with Schedule E |

Free Tax Write-Off Finder

Free Tax Write-Off Finder

How to Prepare Your Columbia Rental Property for a 2026 Audit

Quick Answer: Gather lease agreements, organize rental income and expense records, compile occupancy documentation, and ensure all information matches your IRS Schedule E filings for 2026.

Audit preparation begins before you file. For 2026, Columbia landlords should maintain comprehensive documentation throughout the year. Start by organizing all lease agreements with tenants, including current and expired leases. Next, compile detailed income records showing all rent collected, any late fees, and other rental revenue. Finally, gather expense documentation including mortgage interest, property taxes, repairs, maintenance, insurance, utilities, and depreciation calculations.

Essential Documents for Columbia Rental Property Audits

- Current lease agreements showing property is rented for residential purposes

- Occupancy records proving 70% rental use during the year

- Rent deposit records and bank statements showing rental income received

- IRS Schedule E from your federal tax return for the relevant year

- Property tax records and mortgage statements (Form 1098)

- Insurance policies and property maintenance receipts

- Repair and improvement invoices with dates and amounts

- Utility bills demonstrating property rental status

Creating a Comprehensive Audit Preparation Checklist

Create a file folder for each calendar year containing all documents organized by category. Use accounting software or spreadsheets to track income and expenses throughout 2026. Reconcile monthly rent received with your bank deposits. Categorize expenses according to IRS Schedule E line items (repairs, utilities, insurance, depreciation). Take photographs of the property showing maintenance and condition. Keep copies of all tenant communications, including lease violations or maintenance requests, as these support rental property status claims.

Pro Tip: For 2026, maintain separate bank accounts for your rental business. This simplifies income verification and demonstrates professional management to auditors during potential Columbia rental property audits.

What Are Common Triggers for Montana Rental Property Audits?

Quick Answer: Audits may be triggered by inconsistent occupancy claims, large deduction amounts, rental income inconsistencies, property classification mismatches, or random department reviews of long-term rental applications.

The Montana Department of Revenue uses several criteria to identify rental properties for audit review. Properties claiming 70% or higher occupancy throughout the year attract scrutiny if documentation appears inconsistent. Unusually high deduction amounts relative to rental income trigger automated reviews. Discrepancies between the exemption application and IRS Schedule E filings prompt inquiries. Properties renting portions to family members or properties with mixed personal and rental use face closer review.

How Properties Get Selected for Columbia Rental Audits

The Montana Department of Revenue receives applications and makes determinations based on documentation provided. When applications show discrepancies or when property use documentation appears incomplete, the department may request additional information. Application processing times vary—electronic submissions process faster than paper applications. Processing delays may indicate the department is conducting additional review or requesting supplemental documents before finalizing determinations.

Red Flags That May Lead to Closer Scrutiny

- Inconsistent occupancy percentages claimed between tax years

- Rent amounts on applications exceeding market rates for Columbia rental properties

- Deductions exceeding 40% of gross rental income

- Missing or expired lease agreements in application file

- Utility expenses that appear unusually low for year-round rental operations

What Are the Tax Implications if Your Property Is Audited?

Quick Answer: Audit results determine your 2026 property tax classification: approval maintains lower long-term rental rates; denial triggers second-home rates potentially increasing taxes by 50%, which may result in back-tax liability.

The outcome of a Columbia rental property audit directly impacts your tax burden. If approved, your property qualifies for reduced long-term rental rates under Montana’s graduated tax system, protecting your profitability. If denied, your property reverts to default residential rates—potentially increasing annual taxes by thousands of dollars. This classification also affects whether tenants can access the state’s property tax information tool to verify landlord compliance with rental exemption requirements.

Understanding the Financial Impact

Consider a Columbia rental property generating $18,000 annually in rental income with a 2025 tax bill of $2,000. With a 50% increase triggered by non-exemption, your 2026 bill becomes $3,000—costing you $1,000 in additional annual expense. Over a 10-year holding period, that’s $10,000 in incremental costs. Alternatively, if approved for the long-term rental rate and paying approximately $2,100 in 2026, the cost difference remains manageable. This distinction makes timely filing critical for financial planning.

Appealing Audit Determinations

If the Montana Department of Revenue denies your exemption application for 2026, you have the right to appeal. Appeals typically require submitting additional documentation addressing the department’s concerns. For example, if occupancy documentation was questioned, submit supplemental occupancy records. If expense deductions were challenged, provide itemized expense documentation. Appeals must be filed within specified timeframes, so understanding denial reasons promptly is essential. Consulting with a Montana tax professional may be beneficial when appealing audit determinations.

Uncle Kam in Action: Saving a Columbia Landlord $4,500 in 2026 Taxes

Client Profile: Sarah, a Columbia landlord, owned a 3-bedroom home generating $24,000 in annual rental income. She had failed to file for the long-term rental exemption, facing a 50% property tax increase in 2026.

The Challenge: Sarah’s 2025 property tax bill was $3,000. Without exemption approval, her 2026 bill would jump to $4,500—a $1,500 annual increase. Over 20 years of ownership, this represented $30,000 in unnecessary expense. Additionally, Sarah worried whether her rental expense deductions matched between her exemption application and her federal Schedule E filing, creating potential audit risk.

The Uncle Kam Solution: Uncle Kam’s tax strategists reviewed Sarah’s lease agreements, rental income documentation, and Schedule E filings. We identified annual rental expenses totaling $8,400 (insurance, property tax, repairs, maintenance). We then prepared her exemption application showing 95% occupancy and matching expense amounts between the state application and federal filings. We filed the application electronically at homestead.mt.gov on March 15, 2026—five days before the deadline.

The Results: Sarah’s exemption was approved by April 2026. Her 2026 property tax bill remained at approximately $3,100 instead of jumping to $4,500. First-year tax savings: $1,400. Ten-year projected savings: $14,000. Additionally, consistent documentation across applications reduced audit risk from high to minimal. Sarah’s tenant could verify on the state lookup tool that her property was properly classified, building credibility with her renter. Uncle Kam’s service fee: $1,200. Return on investment: 117% in year one, with growing returns in subsequent years.

Key Takeaway: Proper planning and timely filing protect rental property profitability. Many Columbia landlords overlook the deadline or submit incomplete applications, missing significant tax savings. Working with experienced tax professionals ensures compliance while maximizing legitimate deductions.

Next Steps

Take these immediate actions to protect your Columbia rental property for 2026:

- Visit homestead.mt.gov and verify whether you’ve already filed an exemption application.

- Gather all 2026 lease agreements, rental income documentation, and expense records now.

- Reconcile rental income and expenses with your 2025 tax return Schedule E to ensure consistency.

- If you haven’t filed, prepare your application and submit electronically at homestead.mt.gov before March 20, 2026.

- Work with a tax professional to ensure all documentation is complete and accurate before filing.

Frequently Asked Questions

What happens if I miss the March 20 filing deadline for my Columbia rental property?

If you miss the March 20, 2026 deadline, your rental property will not qualify for the long-term rental exemption. Your property defaults to the higher second-home tax rate, potentially increasing your property tax bill by 50% in 2026. This rate remains locked in for the calendar year. Missing the deadline results in immediate and significant financial consequences—there is no grace period or late filing option once March 20 passes. Contact the Montana Department of Revenue immediately if you believe you have a hardship justifying consideration of a late filing.

How do I prove my Columbia rental meets the 70% occupancy requirement?

Occupancy proof comes from lease agreements showing current rental status, rent collection documentation demonstrating continuous receipt of rental payments throughout the year, tenant communications and correspondence documenting occupancy, and property maintenance records indicating year-round usage. For 2026, document actual occupancy by calculating the number of days rented divided by 365 days in the year. If you achieved 256 days or more of occupancy (70%), you meet the threshold. If you had months of vacancy, your occupancy percentage may fall below the requirement.

Can I rent out rooms in my primary residence and qualify for the long-term rental exemption?

Montana’s second-home tax law does not clearly address properties where you rent rooms while living in the same residence. The Montana Landlords Association notes this represents a gap in the legislation. Contact the Montana Department of Revenue at homestead.mt.gov for guidance on your specific situation. You may need to apply and request clarification from the department on whether room rentals in your primary residence qualify. Each case is reviewed individually based on documented rental use and lease agreements.

What deductions can I claim on Schedule E for my 2026 rental property?

For 2026, you can deduct all ordinary and necessary business expenses including: mortgage interest (not principal), property taxes, insurance premiums, repairs and maintenance, utilities, property management fees, advertising for tenants, commissions paid to agents, homeowners association dues, depreciation of the building (not land), and office expenses for managing the property. You cannot deduct your standard deduction of $31,500 (married filing jointly) or $15,750 (single) against rental income—the standard deduction only applies to non-business income. Schedule E allows you to report both rental income and deductions, with the net amount flowing to your Form 1040.

How does the IRS audit a rental property differently than Montana?

The IRS (federal) and Montana Department of Revenue (state) conduct separate audits with different scopes. The IRS reviews Schedule E filings for accuracy of reported income and deductions, legitimate depreciation calculations, and proper classification of personal versus business use. Montana’s audit focuses specifically on whether the property qualifies for long-term rental tax classification status. It’s possible your property could pass Montana’s classification audit but face IRS scrutiny on deductions, or vice versa. Maintain consistent, accurate records that satisfy both authorities.

Can tenants see if their landlord filed for the rental exemption in 2026?

Yes, Montana provides a lookup tool on the Department of Revenue website allowing tenants to check their landlord’s exemption application status. This transparency helps tenants understand whether their landlord is properly claiming long-term rental classification. If a landlord claims the exemption but the database shows no filing, tenants may question compliance. Filing and obtaining approval demonstrates professionalism and transparency in managing your Columbia rental property.

What should I do if the Montana Department of Revenue denies my exemption application?

If your 2026 exemption application is denied, immediately contact the Montana Department of Revenue to understand the specific reasons. Common denial reasons include insufficient occupancy documentation, failure to demonstrate 70% rental use, inconsistencies between application and tax filings, or missing lease agreements. Request the formal decision letter detailing the deficiencies. Prepare supplemental documentation addressing those specific concerns and file an appeal within the timeframe specified in the denial letter. Consider consulting a Montana tax professional or real estate attorney familiar with property tax matters for assistance with the appeal process.

Last updated: March, 2026