Business Tax Lien Resolution: 2026 Complete Guide

Business tax lien resolution has never been more urgent than in 2026. If the IRS has filed a federal tax lien against your business, you face serious risks to your credit, your assets, and your ability to operate. The good news is that business tax lien resolution offers several proven paths forward — from installment agreements to offers in compromise — and a brand-new IRS Tax Debt Help tool launched April 16, 2026, makes it easier to start. This guide gives you a complete, step-by-step roadmap to protect your business and resolve your lien as fast as possible. For expert tax strategy support tailored to business owners, Uncle Kam is here to help.

This information is current as of 4/17/2026. Tax laws change frequently. Verify updates with the IRS if reading this later.

Table of Contents

- Key Takeaways

- What Is a Federal Tax Lien and How Does It Affect My Business?

- How Does the IRS File a Business Tax Lien in 2026?

- What Are My Business Tax Lien Resolution Options?

- How Does Lien Withdrawal, Discharge, and Subordination Work?

- How Does the 2026 IRS Climate Affect Tax Lien Resolution?

- How Can I Prevent a Business Tax Lien in the First Place?

- Uncle Kam in Action: Restaurant Owner Resolves $87,000 IRS Lien

- Next Steps

- Related Resources

- Frequently Asked Questions

Key Takeaways

- Business tax lien resolution in 2026 includes full payment, installment agreements, offers in compromise, and lien withdrawal.

- The IRS launched a new Tax Debt Help tool on April 16, 2026, making it easier to explore your options online.

- IRS staffing cuts of 25–27% may slow processing times, so act early and document everything.

- Online installment agreements are available for businesses owing $50,000 or less.

- Working with a qualified tax professional dramatically improves your resolution outcome.

What Is a Federal Tax Lien and How Does It Affect My Business?

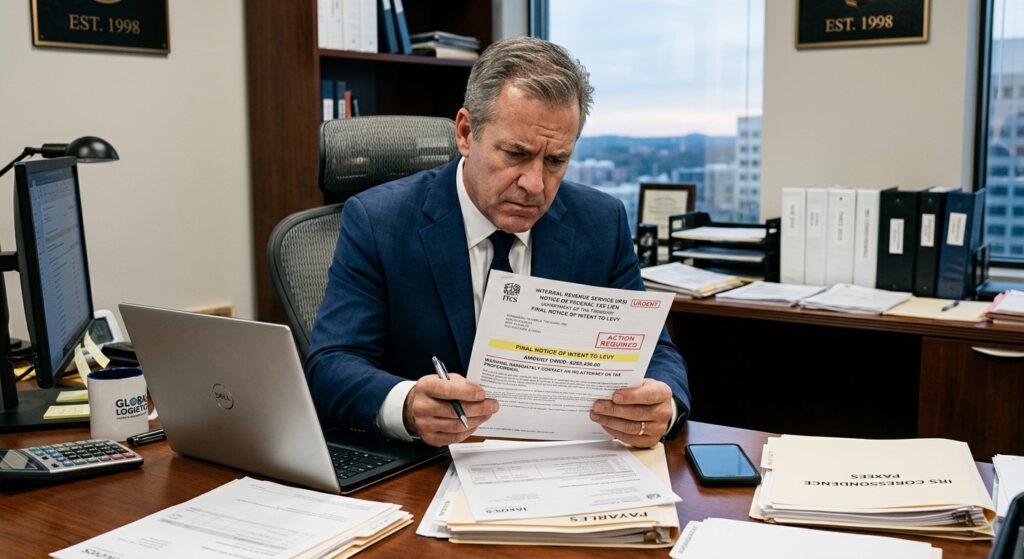

Quick Answer: A federal tax lien is the government’s legal claim against all your business property and assets when you fail to pay a tax debt. It can block financing, damage credit, and threaten business operations.

According to the IRS’s official federal tax lien guidance, a lien arises automatically when you neglect or refuse to pay a tax debt after the IRS sends a bill. The lien attaches to all your property — including real estate, personal property, and financial assets. It also attaches to property you acquire in the future while the lien is active. For a business owner, this is a serious threat that demands immediate action.

How a Lien Differs from a Levy

A lien and a levy are different things. A lien is a legal claim — a warning that you owe money. A levy is the actual seizure of property. However, a lien can lead to a levy if you don’t resolve the debt. Furthermore, a lien filed publicly as a Notice of Federal Tax Lien (NFTL) becomes part of the public record. That can damage your business credit score and make lenders, vendors, and partners nervous.

Real Business Impacts of a Tax Lien in 2026

The consequences of an unresolved business tax lien are wide-ranging. Moreover, they compound over time if left unaddressed. Here are the key risks every business owner must understand:

- Credit damage: A public NFTL shows up in credit reports and can prevent loan approvals.

- Blocked financing: Banks and lenders may refuse to extend lines of credit or business loans.

- Asset encumbrance: You cannot freely sell or transfer business property while a lien is active.

- Contract issues: Government contractors may lose eligibility for federal contracts.

- Escalation risk: A lien can escalate to a levy and actual property seizure.

Pro Tip: As soon as you receive an IRS notice, confirm the lien amount by requesting your IRS Account Transcript at IRS.gov. Errors happen, especially during the 2026 IRS staffing cutbacks.

How Does the IRS File a Business Tax Lien in 2026?

Quick Answer: The IRS files a lien after three steps: it assesses the tax, sends you a bill, and you fail to pay within ten days of the demand notice.

Understanding the lien filing process is critical for effective business tax lien resolution. The IRS follows a specific legal sequence before a lien officially attaches. As explained in IRS Publication 594 (Rev. 1-2026), the collection process begins with assessment and demand, then escalates if you don’t respond.

Step-by-Step: The IRS Lien Filing Process

- Step 1 – Tax Assessment: The IRS calculates what your business owes and officially records the debt.

- Step 2 – Demand Notice: The IRS sends a bill. You typically have 10 days to pay before the lien attaches.

- Step 3 – Lien Attaches: If you don’t pay, the lien attaches automatically to all your business property.

- Step 4 – NFTL Filed: The IRS may file a public Notice of Federal Tax Lien with your county recorder or secretary of state.

- Step 5 – CDP Rights: After the NFTL is filed, you receive a Collection Due Process notice. You have 30 days to request a CDP hearing.

Your Rights as a Business Taxpayer

You have important rights during this process. The Taxpayer Bill of Rights guarantees your right to be informed, to challenge IRS positions, and to appeal decisions. The Taxpayer Advocate Service is also available if you face significant hardship. Therefore, never ignore IRS notices — every notice starts a clock on your rights.

Pro Tip: Request a CDP hearing within the 30-day window if you receive a lien notice. Missing this deadline significantly limits your appeal options. Connect with Uncle Kam’s tax advisory team for immediate guidance.

What Are My Business Tax Lien Resolution Options?

Quick Answer: Your main business tax lien resolution options in 2026 are full payment, installment agreements, offers in compromise, currently not collectible status, and lien subordination or discharge.

Business tax lien resolution is not a one-size-fits-all process. The IRS offers multiple paths depending on your financial situation, business structure, and how much you owe. In April 2026, the IRS also launched a new online Tax Debt Help tool on IRS.gov to guide businesses through these options using simple, interactive questions — no personal data required to explore. Let’s walk through each major option in detail.

Option 1: Full Payment

Full payment is the fastest and cleanest path to business tax lien resolution. When you pay the entire tax debt, the IRS is required to release the lien within 30 days of payment. This eliminates the lien from public record and restores your business’s financial standing. However, most businesses facing a tax lien don’t have the full amount available in cash. Furthermore, paying in full doesn’t automatically remove the NFTL from your credit report — you may need to follow up separately.

Option 2: Installment Agreement

An installment agreement lets you pay your tax debt in monthly payments over time. For businesses owing $50,000 or less in combined tax, penalties, and interest, you can apply for a payment plan entirely online through IRS.gov without needing to call. Consequently, this is one of the most common and accessible business tax lien resolution strategies in 2026.

However, be aware that while an installment agreement stops the IRS from levying, the lien itself remains in place until you pay the full balance. In addition, the IRS continues to charge interest during the repayment period. For 2026, the underpayment penalty rate is approximately 7% (based on the federal short-term rate plus 3 percentage points).

Option 3: Offer in Compromise (OIC)

An offer in compromise allows eligible businesses to settle their IRS debt for less than the full amount owed. This is the most complex business tax lien resolution path, but it can be powerful for businesses that genuinely cannot pay the full balance. The IRS evaluates three factors when considering an OIC:

- Doubt as to Liability: You dispute the actual amount the IRS says you owe.

- Doubt as to Collectibility: You can’t pay the full amount even by selling assets and borrowing.

- Effective Tax Administration: Paying the full amount would create an economic hardship or be inequitable.

The IRS rejects a high percentage of DIY OIC applications. Working with an experienced tax professional through Uncle Kam’s tax preparation and filing services dramatically improves your odds of acceptance. You can check eligibility using the IRS OIC Pre-Qualifier Tool on IRS.gov before applying.

Option 4: Currently Not Collectible (CNC) Status

If your business truly cannot afford to pay its tax debt right now, you may qualify for Currently Not Collectible status. The IRS grants CNC when paying would prevent your business from meeting basic operating expenses. In CNC status, the IRS temporarily pauses active collection actions — including liens and levies. However, interest and penalties continue to accrue. CNC is a pause button, not a permanent solution. Nevertheless, it gives businesses breathing room to stabilize finances before pursuing a longer-term resolution strategy.

Option 5: Penalty Abatement

Penalty abatement doesn’t eliminate your lien, but it can reduce the total amount you owe — making other resolution options more affordable. The IRS offers several types of penalty abatement:

- First-Time Abatement (FTA): Available to businesses with a clean compliance history for the prior three years.

- Reasonable Cause: Available if you can show the failure to pay was due to circumstances beyond your control.

- Statutory Exception: Available in narrow circumstances specifically defined by tax law.

Pro Tip: Always explore penalty abatement before agreeing to a payment plan. Reducing penalties first lowers your total balance, which may make you eligible for simpler online resolution tools.

The table below compares your main business tax lien resolution strategies side by side for 2026.

| Resolution Option | Lien Released? | Best For | 2026 Key Fact |

|---|---|---|---|

| Full Payment | Yes – within 30 days | Businesses with cash reserves | Fastest resolution path available |

| Installment Agreement | No – lien stays until paid | Businesses owing $50,000 or less | ~7% interest rate applies in 2026 |

| Offer in Compromise | Yes – upon acceptance | Businesses unable to pay in full | Professional help strongly recommended |

| Currently Not Collectible | No – pauses collection | Businesses facing hardship | Interest/penalties keep accruing |

| Penalty Abatement | No – reduces balance | Businesses with clean prior history | First-Time Abatement widely available |

How Does Lien Withdrawal, Discharge, and Subordination Work?

Quick Answer: Lien withdrawal removes the NFTL from public record. Discharge removes the lien from specific property. Subordination allows another creditor to take priority over the IRS lien.

Beyond the standard payment-based options, business tax lien resolution also includes three powerful IRS tools that many business owners don’t know about: lien withdrawal, discharge, and subordination. Each serves a different purpose and can be a game-changer depending on your situation. The Taxpayer Advocate Service explains these options in detail on their website.

Lien Withdrawal

A lien withdrawal is the most powerful form of business tax lien resolution short of full payment. When the IRS withdraws a lien, it removes the NFTL from the public record entirely — as if it was never filed. Your business credit can recover much faster after a withdrawal than after a simple lien release. You may qualify for withdrawal if:

- You have entered into a Direct Debit Installment Agreement (DDIA) and owe $25,000 or less.

- The lien was filed prematurely or in violation of IRS procedures.

- Withdrawal would facilitate the collection of the tax owed.

- Withdrawal is in the best interest of you and the government.

Lien Discharge

A lien discharge removes the lien from a specific piece of property, but the underlying tax debt still exists. This is most useful when your business needs to sell an asset — such as real estate or equipment — to raise funds. The lien remains attached to all other business property. Therefore, discharge is a targeted business tax lien resolution tool, not a full solution. To apply, file IRS Form 14135, Application for Certificate of Discharge of Property from Federal Tax Lien.

Lien Subordination

Subordination allows another lender to take a higher priority position over the IRS lien. This doesn’t remove the lien — instead, it allows your business to refinance or obtain new financing even while the lien exists. Banks often require to be in first priority position before lending. Consequently, subordination can help you unlock capital you need to resolve the debt. To apply, file IRS Form 14134, Application for Certificate of Subordination of Federal Tax Lien.

Did You Know? The IRS has expanded its business tax advisory resources. Businesses that set up Direct Debit Installment Agreements (DDIA) may qualify for lien withdrawal even without paying the full debt.

How Does the 2026 IRS Climate Affect Tax Lien Resolution?

Free Tax Write-Off Finder

Free Tax Write-Off FinderQuick Answer: In 2026, IRS staffing cuts of 25–27% and major legislative changes under the One Big Beautiful Bill Act have created both delays and new opportunities for business tax lien resolution.

The IRS landscape in 2026 is unlike any prior year. For business owners working through tax lien resolution, understanding the current environment is critical. Several major developments shape how the IRS handles lien cases right now.

IRS Staffing and Budget Cuts

The IRS has experienced dramatic workforce reductions in 2026. According to reporting from Accounting Today, IRS staffing has been cut by approximately 25–27%. The agency also lost about half of the $80 billion it was originally set to receive under the Inflation Reduction Act of 2022. These cuts affect processing times for installment agreements, OIC applications, and lien-related paperwork. Moreover, the House spending panel proposed an additional $1 billion IRS funding cut in April 2026, which may further slow operations in the months ahead.

The One Big Beautiful Bill Act and Business Taxes

The One Big Beautiful Bill Act (OBBBA), enacted in 2025, brought sweeping changes to business taxes in 2026. Some of these changes directly affect businesses dealing with tax liens. For example, the OBBBA increased the Section 179 expensing limit to $2.5 million — up from $1.25 million previously. This means many businesses can now dramatically reduce their taxable income in the year they purchase equipment. Consequently, some businesses that previously incurred large tax debts may find improved cash flow in 2026 due to these deductions, making lien resolution more feasible.

The New IRS Tax Debt Help Tool (Launched April 16, 2026)

On April 16, 2026 — the day after the tax deadline — the IRS launched a major new resource for businesses and individuals facing tax debt. The Tax Debt Help tool on IRS.gov walks users through interactive questions about their financial situation and directs them toward appropriate resolution options. No personal information is required to explore your options. IRS CEO Frank Bisignano described it as part of the agency’s push toward “user-friendly, digital-first services.” For business owners starting business tax lien resolution, this tool is a logical first step.

Additionally, on April 16, 2026, the House passed H. Res. 1156, a resolution expressing support for the OBBBA’s tax provisions. This signals continued congressional backing for the current tax framework, providing business owners with greater certainty about the rules governing their lien resolution strategies.

| 2026 IRS Development | Date | Impact on Lien Resolution |

|---|---|---|

| IRS Tax Debt Help Tool Launched | April 16, 2026 | Easier self-service exploration of payment options |

| House Passes H. Res. 1156 | April 16, 2026 | Confirms OBBBA tax provisions remain in place |

| IRS Workforce Cut 25–27% | Ongoing in 2026 | Longer processing times for agreements and OICs |

| Section 179 Limit Raised to $2.5M | Effective 2026 | Reduces future tax debts for capital-intensive businesses |

| House Proposes $1B Additional IRS Cut | April 13, 2026 | May further delay IRS responses in late 2026 |

Pro Tip: Due to IRS processing delays in 2026, submit all lien resolution paperwork with certified mail and keep copies of everything. Follow up proactively every 30–45 days on pending requests.

How Can I Prevent a Business Tax Lien in the First Place?

Quick Answer: The best approach to business tax lien resolution is preventing a lien from happening. Pay estimated taxes quarterly, file on time even if you can’t pay, and respond to every IRS notice immediately.

Prevention is always less costly than resolution. For business owners, avoiding a tax lien requires consistent tax compliance and proactive financial management. Even if a lien has already been filed, adopting these prevention habits will keep you from facing another one after resolution.

Pay Your Quarterly Estimated Taxes on Time

The IRS expects businesses to pay estimated taxes four times per year. Failing to do so triggers an underpayment penalty — currently around 7% in 2026 based on the federal short-term rate plus 3 percentage points. That penalty compounds. Additionally, the failure-to-pay penalty adds 0.5% per month on the unpaid balance. In contrast, the failure-to-file penalty is a punishing 5% per month — up to 25% of the unpaid balance. Therefore, always file your returns on time, even if you can’t pay the full amount right away.

Respond to Every IRS Notice Promptly

Many business owners make the mistake of ignoring IRS notices. This is dangerous. Each IRS notice is a step in the collection process that moves toward a lien and eventually a levy. Instead, read every notice carefully, confirm the amounts, and respond within the stated timeframe. If the notice seems incorrect, dispute it immediately in writing. In 2026, with IRS staffing reduced by 25–27%, response times are slower — so the sooner you engage, the better.

Use Smart Business Structure Planning

Your business entity structure affects your tax liability significantly. S corporations and LLCs structured correctly can reduce self-employment taxes, lower your overall tax burden, and improve cash flow. Lower tax burdens mean less risk of falling behind on payments. Explore your options with Uncle Kam’s entity structuring services to ensure your business is set up for long-term tax efficiency.

Use our LLC vs S-Corp Tax Calculator to compare structures and estimate how much you could save by optimizing your entity type for 2026.

Maintain Accurate Books Year-Round

Poor bookkeeping is one of the leading causes of surprise tax bills that lead to liens. When your books are accurate, your quarterly estimates are more reliable, your deductions are well-documented, and your risk of an unexpected large tax balance drops sharply. Consider using Uncle Kam’s business solutions for bookkeeping and financial systems that keep your compliance on track throughout the year.

Pro Tip: Under the One Big Beautiful Bill Act, the Section 179 deduction limit is now $2.5 million in 2026. Maximizing this deduction in the year of a major equipment purchase can dramatically cut your taxable income and reduce your risk of falling behind on taxes.

Uncle Kam in Action: Restaurant Owner Resolves $87,000 IRS Lien

Client Snapshot: A restaurant owner in the mid-Atlantic region came to Uncle Kam in early 2026 after receiving a Notice of Federal Tax Lien from the IRS for $87,000 in unpaid payroll taxes and penalties accumulated over two years.

Financial Profile: The restaurant had annual revenues of approximately $1.2 million but operated on thin margins. The business had an outstanding payroll tax balance, including failure-to-deposit penalties of 2–10% and mounting interest.

The Challenge: The public Notice of Federal Tax Lien was blocking the owner’s ability to refinance the restaurant’s commercial lease property — a critical move needed to fund urgent kitchen equipment upgrades. The lien was also affecting the restaurant’s relationship with its primary food distributor, which had discovered the lien during a routine credit check.

The Uncle Kam Solution: Uncle Kam’s tax advisory team took a multi-step approach to business tax lien resolution. First, they requested the client’s IRS Account Transcript and discovered $9,200 in penalty charges that qualified for First-Time Abatement based on the restaurant’s clean compliance history in prior years. They filed a successful FTA request, reducing the balance to approximately $77,800. Next, the team filed an Application for Certificate of Subordination (Form 14134) to allow the property refinance to proceed, which gave the client access to $50,000 in capital. Finally, they enrolled the client in a Direct Debit Installment Agreement for the remaining balance, which also qualified the business for a lien withdrawal request under the IRS Fresh Start Program. Within 90 days of engagement, the NFTL was withdrawn from the public record.

The Results:

- Tax Debt Reduced: From $87,000 to $77,800 through penalty abatement — a $9,200 savings.

- Lien Withdrawn: Public NFTL removed from record within 90 days, protecting business credit.

- Refinancing Unlocked: $50,000 in capital secured through lien subordination.

- Investment: Client paid $3,500 in professional fees to Uncle Kam.

- First-Year ROI: Over $62,700 in combined value (penalty reduction + refinancing capital), representing an 18x return on the professional fee investment.

This case shows why professional guidance transforms business tax lien resolution outcomes. See more results like this on our client results page.

Next Steps

If your business is dealing with a federal tax lien, take action now. Every day of delay adds interest and penalties. Here are your immediate next steps:

- Step 1: Pull your IRS Account Transcript at IRS.gov to verify the lien amount and confirm there are no errors.

- Step 2: Use the new IRS Tax Debt Help tool at IRS.gov to explore your options anonymously — no login required.

- Step 3: Check whether any penalties qualify for First-Time Abatement to reduce your total balance before choosing a resolution strategy.

- Step 4: If you received a Collection Due Process notice, request a CDP hearing within 30 days — do not miss this deadline.

- Step 5: Work with a qualified tax professional. Contact Uncle Kam’s business tax strategy team to build a personalized lien resolution plan for 2026.

Related Resources

- Business Tax Strategy Services — Uncle Kam

- Tax Advisory and Ongoing Guidance — Uncle Kam

- Entity Structuring for Business Owners — Uncle Kam

- Uncle Kam Tax Guides and Resources

- Frequently Asked Tax Questions — Uncle Kam

Frequently Asked Questions

How long does it take for business tax lien resolution to complete in 2026?

The timeline depends on which resolution path you choose. Full payment triggers a lien release within 30 days. Installment agreements can be set up online in as little as a few days. However, offers in compromise typically take 6–12 months to process, and IRS staffing cuts in 2026 may extend these timelines further. Lien withdrawal requests after entering a Direct Debit Installment Agreement can take 30–60 days. Therefore, acting early gives you the best chance of a faster resolution.

Can I sell my business property if there is an active tax lien?

Generally, a federal tax lien attaches to all property you own — including real estate and equipment. You cannot freely sell encumbered property without the IRS’s involvement. However, business tax lien resolution tools like discharge (IRS Form 14135) can remove the lien from a specific asset so it can be sold. In many cases, the IRS agrees to discharge when the sale proceeds go toward paying the tax debt. Work with a tax professional before attempting any property sale while a lien is active.

Does an IRS payment plan remove the tax lien from my credit report?

Not automatically. An installment agreement stops the IRS from levying your assets, but the lien itself remains active until the full balance is paid. However, if you set up a Direct Debit Installment Agreement and owe $25,000 or less, you may qualify for a lien withdrawal, which does remove the public NFTL from the record. This is one of the most underutilized strategies in business tax lien resolution. Ask your tax professional about the DDIA withdrawal program when negotiating your installment agreement terms.

What happens if I ignore a federal tax lien in 2026?

Ignoring a federal tax lien is extremely risky. If you do nothing, the IRS can escalate to a tax levy — the actual seizure of your business assets, bank accounts, or accounts receivable. The failure-to-pay penalty continues to accumulate at 0.5% per month, and interest accrues on the full balance at approximately 7% in 2026. Furthermore, the IRS has a 10-year statute of limitations to collect, meaning it can pursue collection for a decade. Business tax lien resolution becomes more expensive and complicated the longer you wait.

How does the 2026 IRS Tax Debt Help tool work for businesses?

The IRS launched its Tax Debt Help tool on April 16, 2026. It is available on IRS.gov at any time without requiring you to log in or share personal information. The tool asks a short series of questions about your financial situation and guides you toward appropriate resolution options, such as payment plans, offers in compromise, or temporary collection delays. It is a good starting point for business owners who want to understand their options before calling the IRS or consulting a professional. However, it cannot replace expert guidance for complex business tax lien resolution situations involving large balances, multiple years, or payroll tax issues.

Can the IRS file a lien against my personal assets for business tax debt?

It depends on your business structure. If you operate as a sole proprietor or general partnership, there is no legal separation between you and the business — the IRS can file a lien against both business and personal assets. For LLCs and corporations, personal liability is generally limited, but there are important exceptions. If you are a responsible party for payroll taxes (Trust Fund taxes), the IRS can pursue you personally through a Trust Fund Recovery Penalty even if your business is a corporation or LLC. This is one of the most aggressive IRS collection tools, making proper entity structuring critical for business owners.

Last updated: April, 2026