The Proactive Tax Strategy: How to Stop Paying Taxes and Start Building Wealth

Most business owners treat taxes as a once-a-year event, a frantic scramble in April to gather receipts and hope for the best. This is a losing game. The proactive tax strategist understands that taxes are not a debt you owe; they are a result of a system you control. This guide is the blueprint for that system. We will show you how to move from a reactive taxpayer to a proactive tax planner, and in doing so, transform your tax bill from your biggest expense into your greatest source of investment capital.

The Three Pillars of a Proactive Tax Strategy

An effective tax strategy is not a random collection of tips and tricks. It is a holistic system built on three core pillars. Master these three pillars, and you will have mastered the game of tax reduction.

Pillar 1: Entity Optimization.

- This is the foundation. The legal and tax structure of your business is the single most important factor in your tax strategy. Choosing the right entity is the difference between paying a 15.3% self-employment tax on every dollar of profit and strategically controlling your tax destiny.

Pillar 2: Deduction Maximization.

- This is not about finding a few extra write-offs. This is about building a bulletproof system to ensure that every single dollar you spend on your business is properly documented and deducted. It’s about transforming your personal expenses into legitimate business deductions.

Pillar 3: Retirement Supercharging.

- This is the ultimate wealth-building tool. The tax code provides a powerful set of incentives for you to save for your own retirement. By using the right retirement accounts, you can shelter tens of thousands of dollars from tax every single year, creating a tax-free wealth machine.

Pillar 1: Entity Optimization - The S-Corp Decision

The S-Corp Advantage:

The magic of the S-Corp is that it allows you to split your income into two components: a reasonable salary and a distribution. You pay payroll taxes (the 15.3% for Social Security and Medicare) on your salary, but you do not pay this tax on the distributions. For a business with $150,000 in profit, this simple strategy can save you over $10,000 a year in self-employment tax.

As a general rule, once your business is consistently generating over $60,000 a year in net profit, the tax savings from the S-Corp election will far outweigh the administrative costs of running payroll and filing a separate tax return. If you are above this threshold and you are not an S-Corp, you are voluntarily overpaying the IRS.

Pillar 2: Deduction Maximization - Building Your System

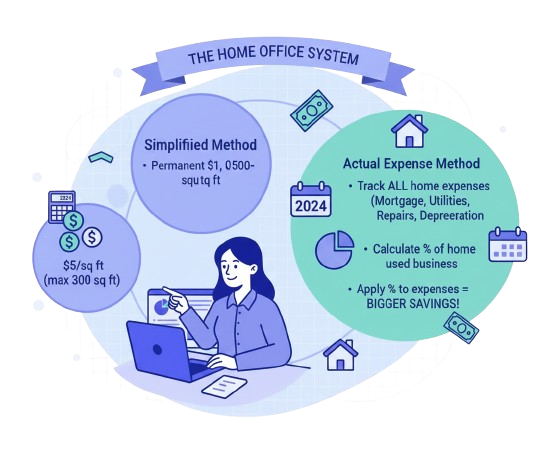

- Calculate the square footage of your office as a percentage of your home’s total square footage.

- Track all your actual home expenses throughout the year.

- Apply the percentage to your total expenses to determine your deduction.

To claim the home office deduction, you must use a portion of your home exclusively and regularly for business. While the simplified method ($5 per square foot) is easy, the Actual Expense Method is where the real savings are. With this method, you can deduct a percentage of your actual home expenses, including mortgage interest, rent, utilities, repairs, and depreciation. To do this correctly, you must:

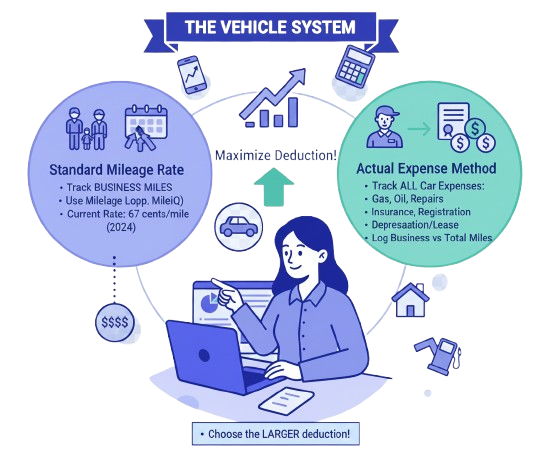

- Keep a contemporaneous mileage log. This is non-negotiable. Use an app like MileIQ to make this effortless.

- At the end of the year, calculate your deduction using both the standard mileage rate and the actual expense method (where you deduct the business-use percentage of your gas, repairs, insurance, and depreciation).

- Choose the method that results in the larger deduction.

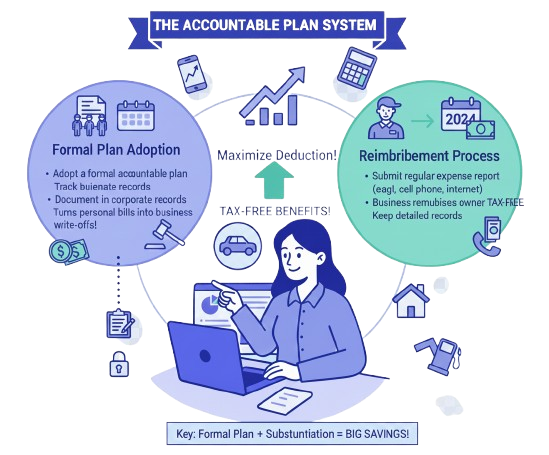

- Adopt a formal accountable plan in your corporate records.

- Submit a regular expense report to your business for the business-use portion of your personal expenses.

- Have the business reimburse you for that amount.

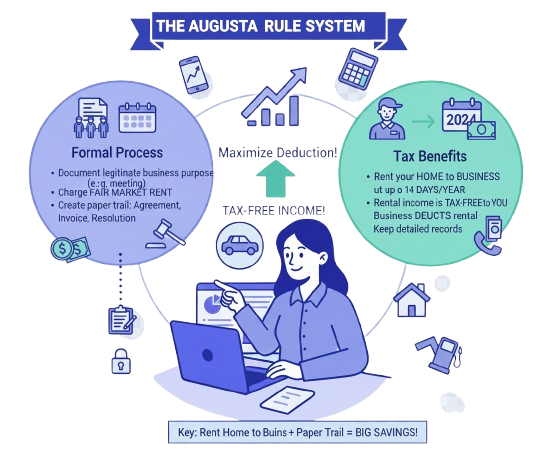

This is one of the most powerful and underutilized strategies. The Augusta Rule allows you to rent your personal home to your business for up to 14 days a year, and the rental income is completely tax-free to you personally, while the business gets to deduct the rental payments. To do this correctly, you must:

- Document a legitimate business purpose for the rental (e.g., a board meeting, a team retreat).

- Charge a fair market rent. Research what a comparable event space would cost.

- Create a formal paper trail: a rental agreement, an invoice from you to the business, and a board resolution approving the rental.

Pillar 3: Retirement Supercharging - Your Tax-Free Wealth Machine

The Big Three Retirement Plans:

1. SEP IRA: The easiest to set up. You can contribute up to 25% of your compensation, up to a maximum of $69,000 for 2024. The contributions are 100% deductible to the business.

2. SIMPLE IRA: This plan allows for both employee and employer contributions, but the limits are lower than other plans.

3. The Solo 401(k): The King of Small Business Retirement Plans. If you are a solo business owner (or only employ your spouse), the Solo 401(k) is, without a doubt, the best retirement plan available. It allows you to contribute as both the “employee” and the “employer,” which can allow you to contribute over $69,000 a year, even on a relatively modest income. It also has two other massive advantages:

- The Roth Option:Most Solo 401(k)s have a Roth option, which allows you to make after-tax contributions that will grow completely tax-free forever.

- The Loan Provision: You can borrow up to $50,000 from your Solo 401(k) for any reason, providing a valuable source of liquidity.

Case Study: The Power of the Solo 401(k)

Meet Jane, an S-Corp owner with $120,000 in profit. She pays herself a $60,000 salary. With a Solo 401(k), she can contribute:

As the “employee”:

She can contribute 100% of her salary, up to the employee limit of $23,000 (for 2024).

As the “employer”:

She can contribute up to 25% of her salary, which is another $15,000.

In total, Jane can contribute $38,000 to her Solo 401(k), reducing her taxable income by that amount and saving over $10,000 in federal and state income tax. This is the power of a proactive retirement strategy.

Putting It All Together: The Proactive Tax Strategy Calendar

A strategy is only as good as its implementation. Here is a simple calendar to keep you on track throughout the year.

- January: Set your reasonable salary for the year. Adopt your accountable plan. Make your final prior-year estimated tax payment.

- February: File your 1099s for any contractors you paid over $600 last year.

- March: S-Corp and partnership tax returns are due (or file for an extension). This is also the deadline to make the S-Corp election for the current year.

- April: Personal tax returns are due. Make your first-quarter estimated tax payment for the current year.

- May: Review your year-to-date financials. Are you on track with your profit goals?

- June: Make your second-quarter estimated tax payment.

- July: Mid-year review. Meet with your tax advisor to assess your tax situation and make any necessary adjustments to your salary or distributions.

- August: Plan your Augusta Rule rental days for the rest of the year.

- September: Make your third-quarter estimated tax payment.

- October: Final deadline for extended S-Corp, partnership, and personal tax returns.

- November: Year-end tax planning. Meet with your advisor to project your final income and make any last-minute strategic moves, like purchasing equipment or funding your retirement plan.

- December: Final push to maximize deductions. Make sure all your expenses are paid and recorded.

The Final Word: You Are in Control

A proactive tax strategy is a system for winning the game of taxes. It is a conscious decision to move from a place of fear and confusion to a place of power and control. You have the ability to build a tax-efficient machine that will not only save you thousands of dollars a year but will also provide the capital to build the business and the life of your dreams.

It’s time to stop being a taxpayer and start being a tax planner.