LLC vs. S-Corp Taxes: The Definitive Guide to a Six-Figure Decision

For a profitable business owner, this isn’t a small administrative choice. It’s a high-stakes financial strategy decision that, over the life of your business, can easily be worth six figures. Getting it right means thousands, or even tens of thousands, of dollars in your pocket every single year. Getting it wrong is like voluntarily leaving a 15% tip for the IRS on your own hard-earned profits.

Most business owners get this wrong. They either stick with the default LLC structure out of simplicity and massively overpay in self-employment taxes, or they hear the term “S-Corp” and fear it’s too complex, too expensive, or too risky, and in doing so, leave a fortune on the table.

The Foundational Misunderstanding: An LLC is NOT a Tax Classification

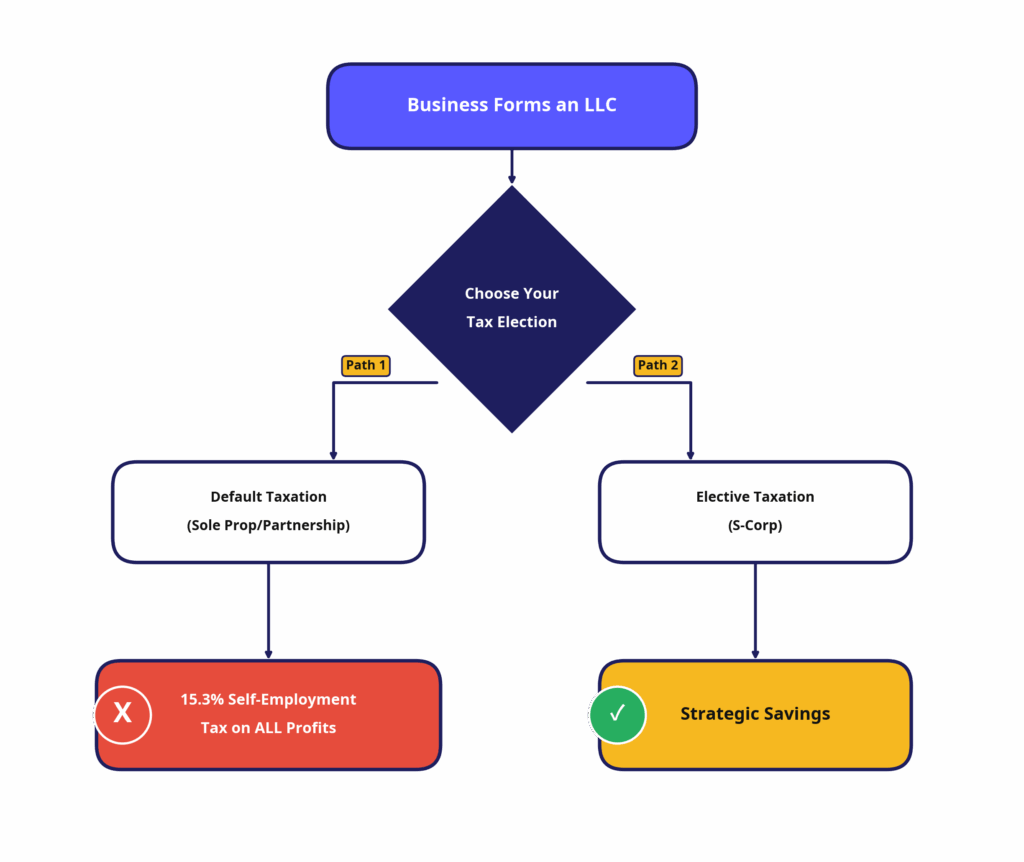

Before we can compare, we must clarify. The single greatest source of confusion in this entire debate is the failure to understand this one core concept: An LLC is a legal entity. An S-Corp is a tax election.

An LLC (Limited Liability Company) is a business structure created by state law. Its primary purpose is to provide you, the owner, with liability protection, creating a legal shield between your business debts and your personal assets (like your house and your car). That’s it. By default, the IRS doesn’t even have a tax category for LLCs.

Instead, the IRS “disregards” the LLC and defaults to taxing it based on the number of owners:

One owner (single-member LLC)

Taxed as a Sole Proprietorship

Two or more owners (multi-member LLC)

Taxed as a Partnership.

An S-Corporation, on the other hand, is not a legal entity. It is a special tax status you can elect for your LLC (or C-Corporation) to have by filing a form with the IRS.

[Flowchart showing a business forming an LLC, then splitting into two paths: ‘Default Taxation (Sole Prop/Partnership)’ leading to ‘15.3% Self-Employment Tax on ALL Profits’, and ‘Elective Taxation (S-Corp)’ leading to ‘Strategic Savings’]

A Tale of Three Tax Bills: Case Studies at Every Level

To truly understand the power of the S-Corp election, we need to move beyond simple examples and look at detailed, real-world scenarios. We will follow three different business owners at three distinct profit levels to see how this single decision impacts their take-home pay, their financial strategy, and their ability to build wealth.

Case Study 1: The Rising Freelancer - $80,000 in Net Profit

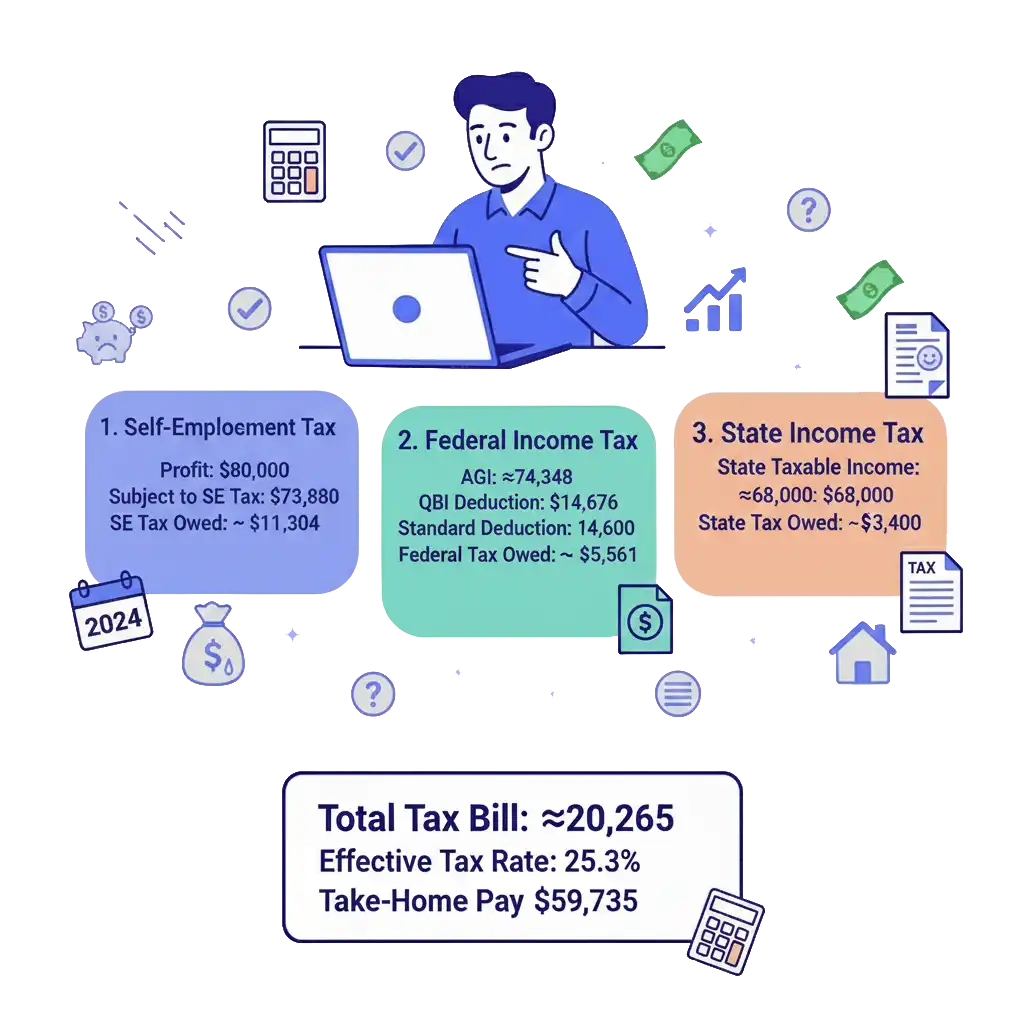

The Owner: Meet Alex, a talented freelance web developer. After years of building a client base, Alex’s single-member LLC had a breakout year, netting $80,000 after all business expenses. Alex lives in a state with a 5% income tax and is single.

The Default LLC Path:

Alex sticks with the default sole proprietorship taxation. The math is straightforward and brutal.

- 1. Self-Employment Tax: The IRS demands its 15.3% cut for Social Security and Medicare on nearly all of the profit.

- Profit Subject to SE Tax: $80,000 * 92.35% = $73,880

- SE Tax Owed: $73,880 * 15.3% = $11,304

- 2. Federal Income Tax: Alex gets the standard deduction and the QBI deduction.

- Adjusted Gross Income (AGI): $80,000 - (1/2 of SE Tax of $5,652) = $74,348

- QBI Deduction: 20% of $73,880 = $14,776

- Taxable Income: $74,348 - $14,776 (QBI) - $14,600 (Standard Deduction) = $44,972

- Federal Income Tax Owed: ~$5,561

- 3. State Income Tax:

- State Taxable Income: ~$68,000 (varies by state rules)

- State Income Tax Owed: ~$3,400

👉Total Tax Bill: ~$20,265

👉Effective Tax Rate: 25.3%

👉Take-Home Pay: $59,735

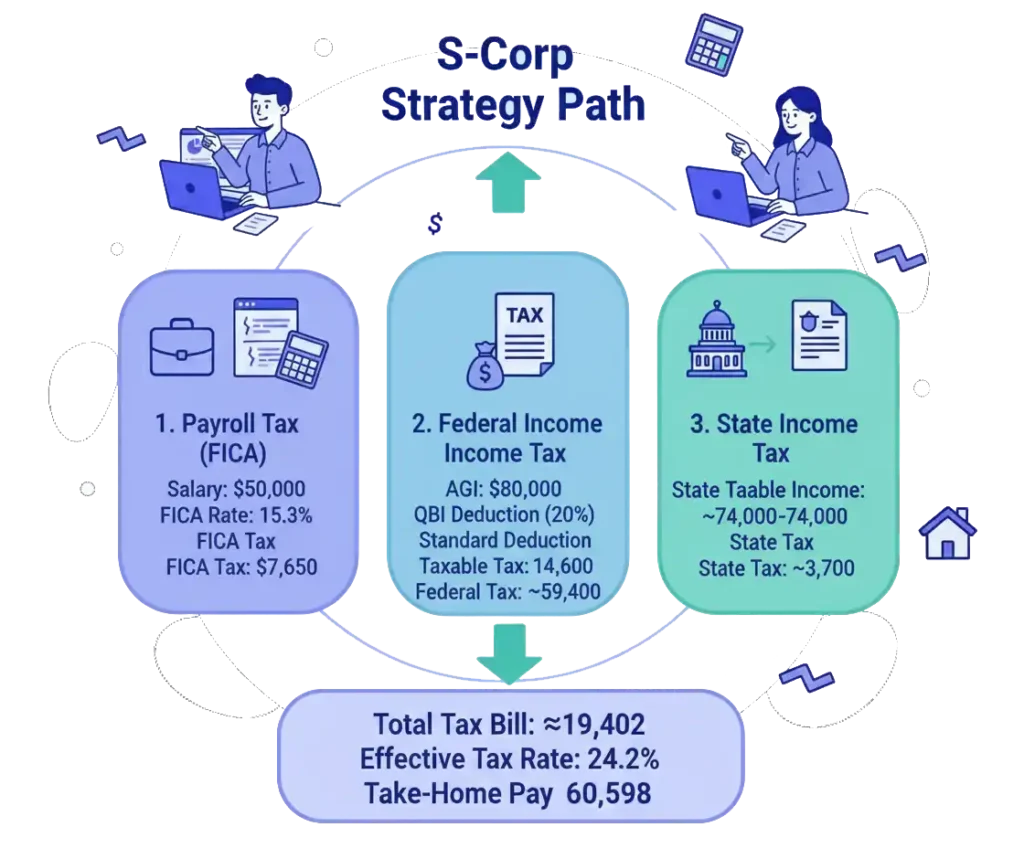

The S-Corp Strategy Path:

Alex consults a tax strategist and elects to be taxed as an S-Corp. They determine a reasonable salary for a web developer in his area is $50,000.

- 1. Payroll Tax (FICA): This is the 15.3% tax, but only on the salary.

- FICA Tax on $50,000 Salary: $7,650

- 2. Federal Income Tax:

- AGI: $50,000 (Salary) + $30,000 (Distribution) = $80,000

- QBI Deduction: 20% of the $30,000 in pass-through profit = $6,000

- Taxable Income: $80,000 - $6,000 (QBI) - $14,600 (Standard Deduction) = $59,400

- Federal Income Tax Owed: ~$8,052

- 3. State Income Tax:

- State Taxable Income: ~$74,000

- State Income Tax Owed: ~$3,700

👉Total Tax Bill: ~$19,402

👉Effective Tax Rate: 24.2%

👉Take-Home Pay: $60,598

The Analysis:

Even at this level, the S-Corp election provides a net savings of $863, even after accounting for an estimated $2,000 in payroll and accounting fees. More importantly, it establishes a scalable system. As Alex’s income grows, the savings will explode.

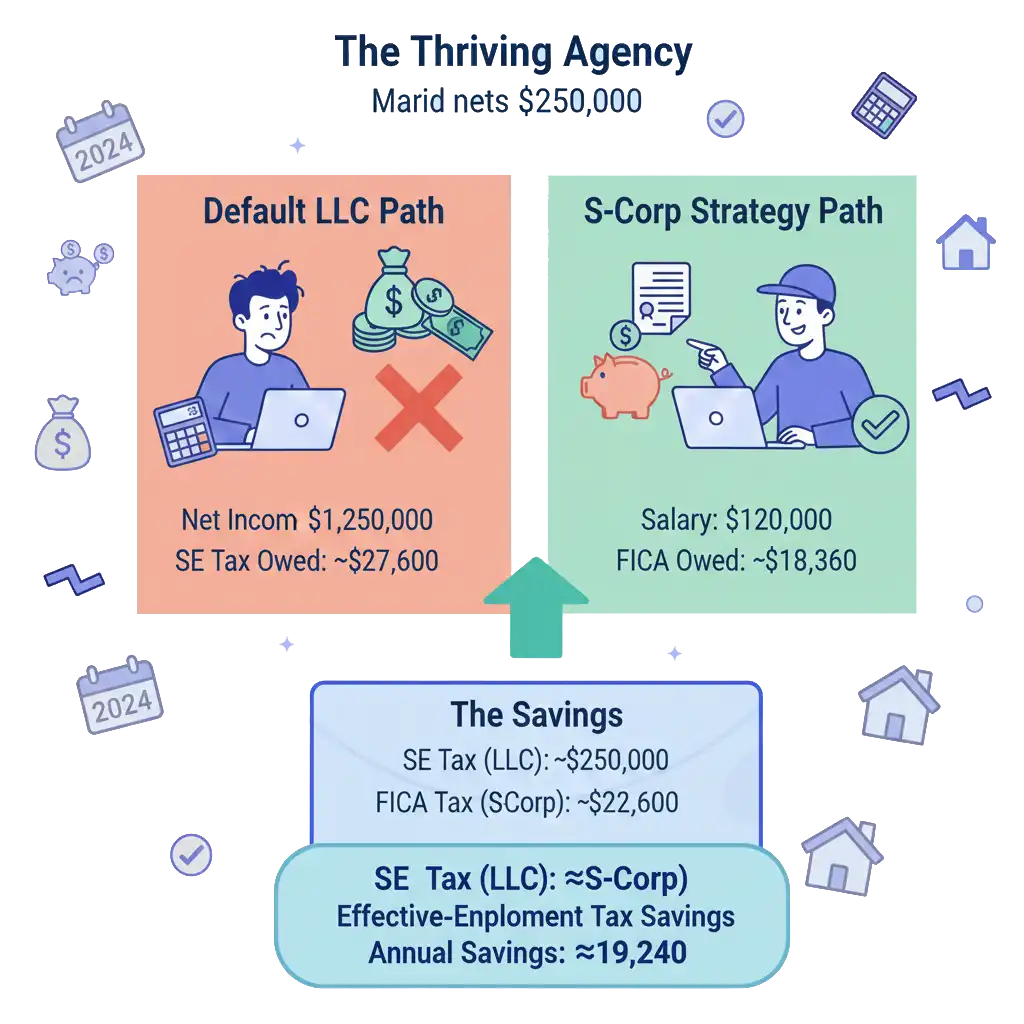

Case Study 2: The Thriving Agency - $250,000 in Net Profit

The Owner: Meet Maria, the founder of a successful digital marketing agency. Her LLC, taxed as an SCorp, nets $250,000.

The Default LLC Path (Hypothetical):

If Maria had remained a default LLC, her tax situation would be painful.

- 1. Self-Employment Tax:

- The 12.4% Social Security tax applies up to the $168,600 wage base for 2024. The 2.9% Medicare tax applies to all of it.

- SE Tax Calculation: ($168,600 * 15.3%) + (($250,000 * 92.35%) - $168,600) * 2.9% = $25,796 + $1,804 = $27,600 (approx.)

- The S-Corp Strategy Path:

Maria pays herself a reasonable salary of $120,000 for her role as CEO and lead strategist.

- 1. Payroll Tax (FICA):

- FICA on $120,000 Salary: $18,360

- 2. The Savings:

- SE Tax as Default LLC: $27,600

- FICA Tax as S-Corp: $18,360

- Annual Self-Employment Tax Savings: $9,240

- The Lifestyle Impact:

What does an extra $9,240 a year mean for Maria? It’s not just a number on a spreadsheet. It’s:

- A fully funded family vacation to Europe, every single year.

- The ability to max out a Roth IRA for both herself and her spouse.

- The down payment on a rental property every two to three years, accelerating her path to financial freedom.

This is the tangible result of a single strategic decision.

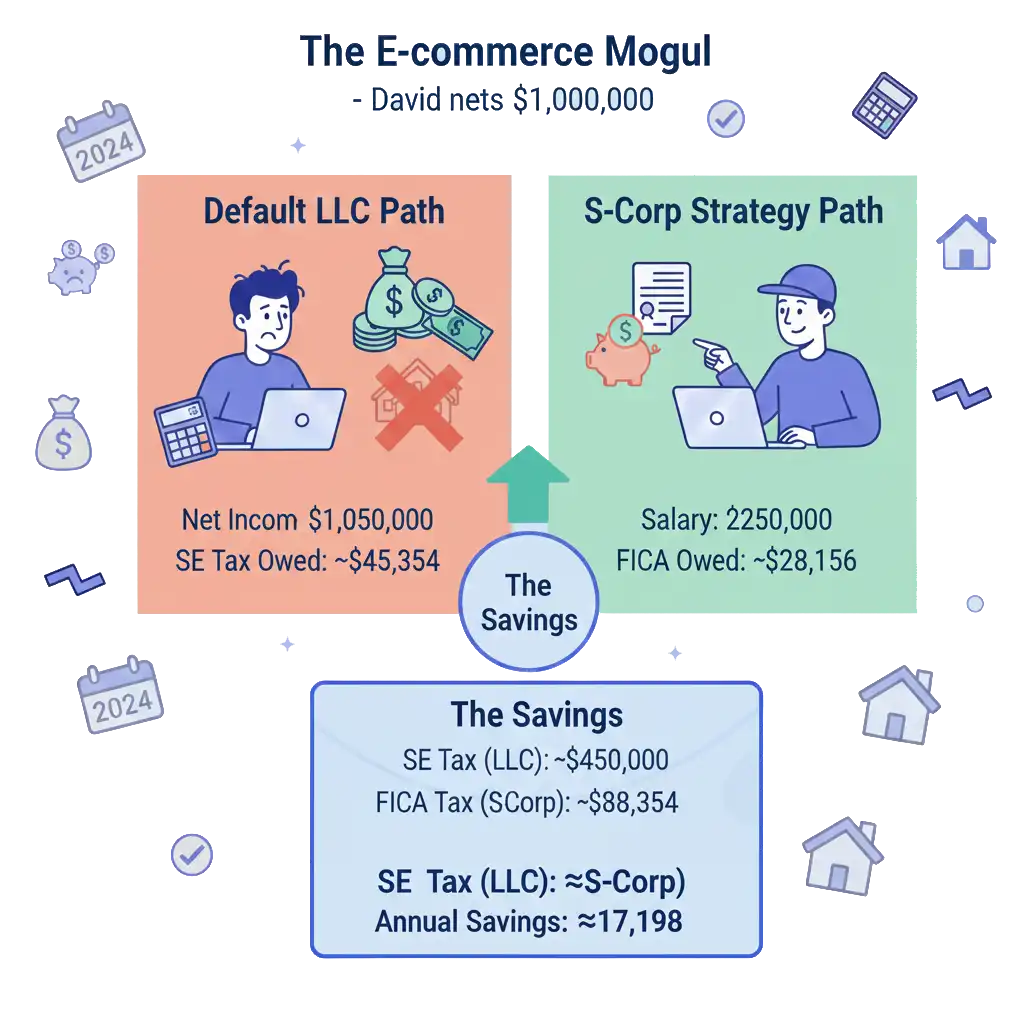

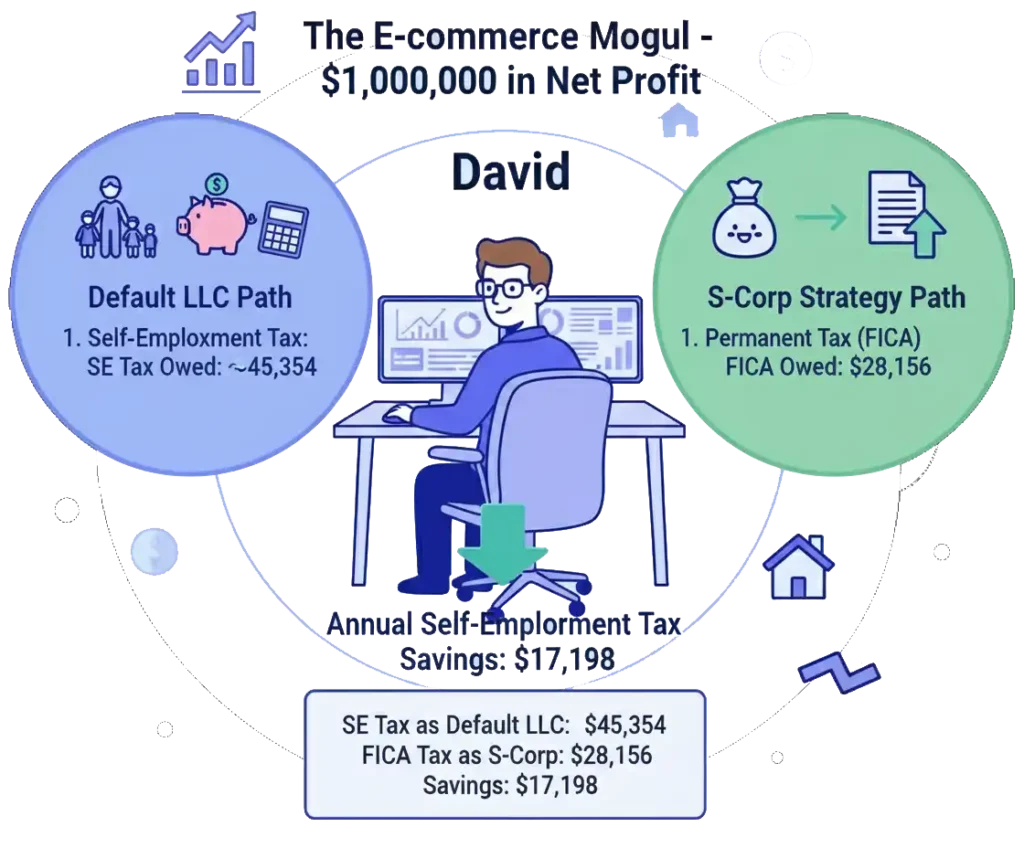

Case Study 3: The E-commerce Mogul - $1,000,000 in Net Profit

The Owner: Meet David, whose e-commerce brand has exploded, netting $1,000,000 this year.

The Default LLC Path (Hypothetical):

- 1. Self-Employment Tax:

- The calculation is complex, but the result is a massive tax bill.

- SE Tax Owed: ~$45,354

- The S-Corp Strategy Path:

David’s role is primarily strategic CEO. He sets a reasonable salary of $250,000.

- 1. Payroll Tax (FICA):

- The Social Security portion is capped at the $168,600 wage base.

- FICA Owed: ($168,600 * 15.3%) + (($250,000 - $168,600) * 2.9%) = $25,796 + $2,360 = $28,156

- 2. The Savings:

- SE Tax as Default LLC: $45,354

- FICA Tax as S-Corp: $28,156

- Annual Self-Employment Tax Savings: $17,198

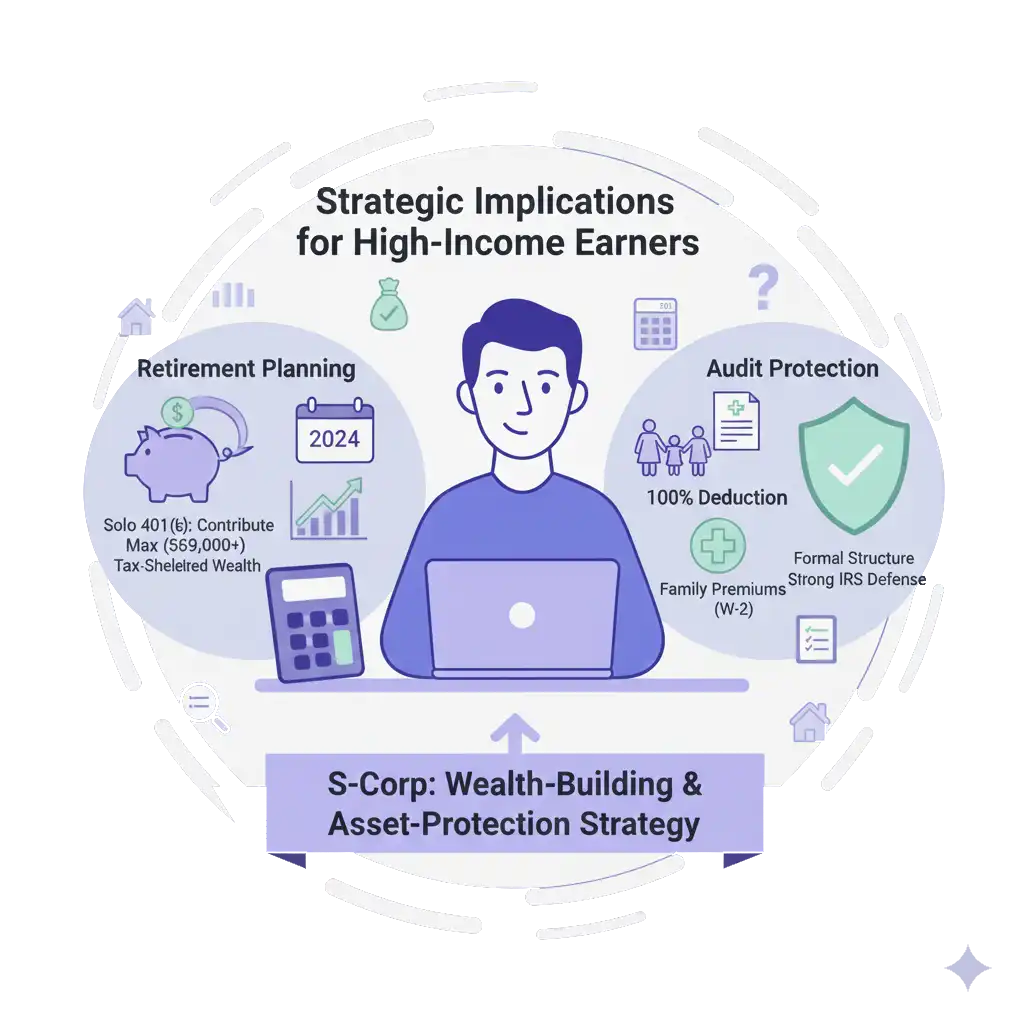

The Strategic Implications:

For David, the $17,198 in annual savings is significant, but the S-Corp structure provides even greater strategic advantages at this level:

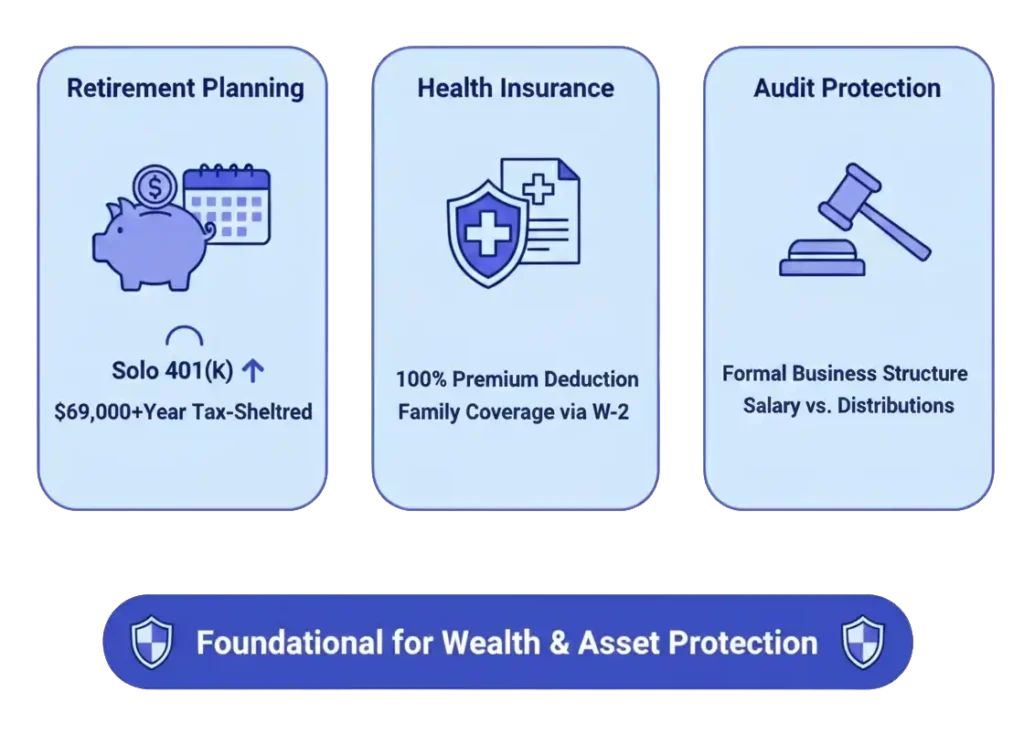

- Retirement Planning: The S-Corp salary allows David to implement a Solo 401(k) and contribute the maximum as both "employee" and "employer," potentially sheltering over $69,000 per year from tax.

- Health Insurance: He can use the S-Corp to deduct 100% of his family's health insurance premiums through the W-2 process.

- Audit Protection: The formal structure of the S-Corp, with its clear distinction between salary and distributions, provides a much stronger defense in the event of an IRS audit compared to a highincome sole proprietorship.

For high-income earners, the S-Corp is not just a tax-saving tool; it is a foundational element of a comprehensive wealth-building and asset-protection strategy.

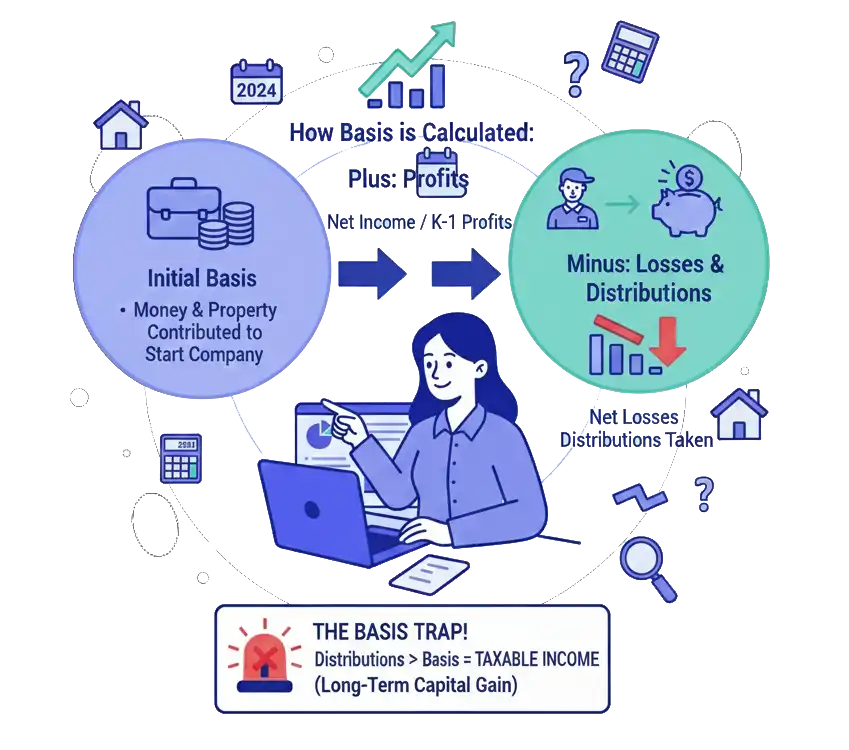

The S-Corp Basis Deep Dive: A Trap for the Unwary

“Basis” is one of the most critical and misunderstood concepts for S-Corp owners. In simple terms, your basis is your financial stake in the company. It is the well from which you can draw tax-free distributions. If you take distributions when the well is dry (i.e., you have no basis), those distributions become taxable income. This is a tripwire that can turn your tax-saving strategy into a tax nightmare.

How Basis is Calculated:

Your initial basis is the amount of money and property you contributed to start the company. From there, it is a running, year-by-year calculation:

Basis Increases With:

- Additional capital contributions you make.

- Your pro-rata share of the company's profits (the net income on your Schedule K-1).

- Loans you personally make to the corporation.

Basis Decreases With:

- Distributions you take (but not below zero).

- Your pro-rata share of the company's losses.

- Repayment of loans you made to the corporation.

A Multi-Year Basis Tracking Example:

Let’s follow a business owner, Jane, over three years to see how basis works in practice.

- Year 1: Formation and Profit

- Jane starts her S-Corp with a $10,000 personal investment. Her initial basis is $10,000.

- The business has a successful first year, with a net profit of $80,000. This is reported on her K-1.

- Her basis increases by the profit: $10,000 + $80,000 = $90,000.

- Jane takes a distribution of $40,000.

- Her year-end basis is: $90,000 - $40,000 = $50,000. The distribution is completely tax-free.

- Year 2: A Business Loss

- The market takes a downturn, and the business has a net loss of $20,000.

- Her basis decreases by the loss: $50,000 - $20,000 = $30,000

- Jane needs money to live, so she takes a distribution of $35,000.

- The Basis Trap is Sprung!

- The first $30,000 of the distribution is a tax-free return of her basis. Her basis is now $0.

- The remaining $5,000 is a distribution in excess of basis. This amount is not taxfree. It will be reported on her personal tax return as a long-term capital gain.

- Year 3: Recovery and a Loan

- Jane's basis starts at $0.

- To get through a slow period, Jane personally loans the company $15,000. This is a formal loan with a promissory note. This loan increases her basis to $15,000.

- The business recovers and has a net profit of $100,000.

- Her basis increases: $15,000 + $100,000 = $115,000.

- She takes a distribution of $60,000.

- Her year-end basis is: $115,000 - $60,000 = $55,000. The distribution is tax-free.

Why This Matters:

Accurate basis tracking is not optional. It is a legal requirement for every S-Corp shareholder. Your tax preparer should be updating your basis schedule every single year. If they are not, it is a major red flag. Without this calculation, you are flying blind and risk turning tax-free distributions into a surprise tax bill.

S-Corp Formalities: Respecting the Corporate Veil

When you elect to have your LLC taxed as an S-Corporation, you are asking the IRS to treat your business as a corporation for tax purposes. This is a privilege, and it comes with the expectation that you will respect the corporate form. This means running your business with a certain level of formality that is not required of a default LLC. Failure to do so can give the IRS a powerful argument to “pierce the corporate veil.” This is a legal concept that essentially says you have not been acting like a real business, and therefore, you do not deserve the tax benefits or liability protection of one.

Here is a guide to the essential corporate formalities you must follow.

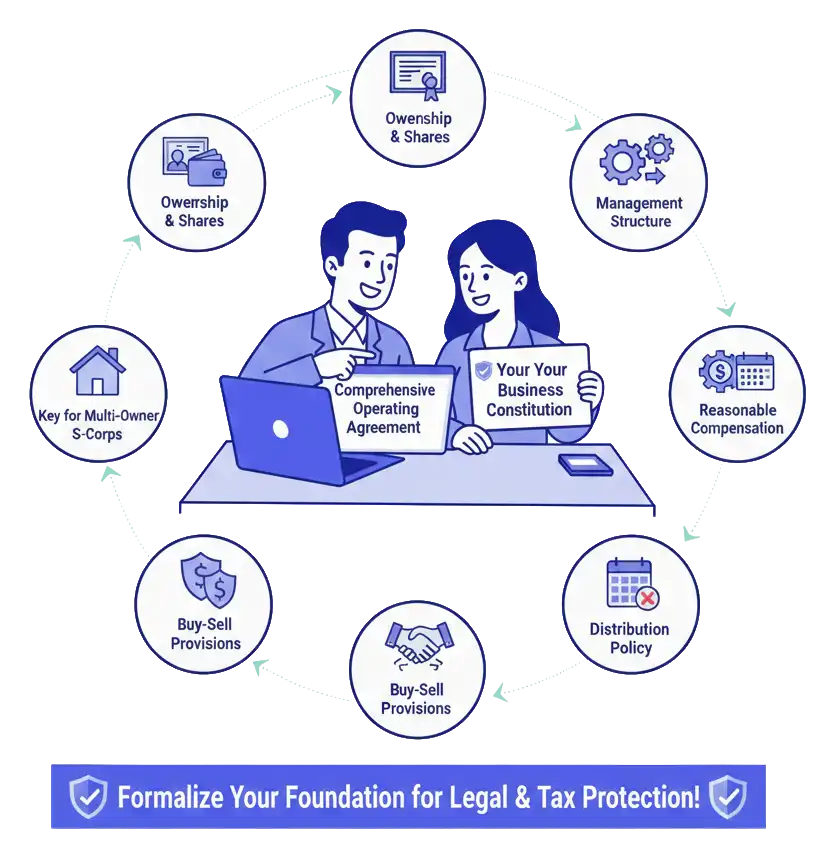

1. A Comprehensive Operating Agreement

While all LLCs should have an operating agreement, it is absolutely critical for an LLC taxed as an SCorp. This internal document is the constitution of your business. It should be far more detailed than a simple template.

- What to Include:

- Ownership and Share Structure: Clearly define who the owners (shareholders) are and the number of shares each owns. Even if you are the sole owner, you should formally issue 100% of the shares to yourself.

- Management Structure: Detail who is responsible for managing the business. Will it be managed by the members (owners) or by appointed managers?

- Reasonable Compensation Clause: Include a clause stating that all owner-employees will be paid a reasonable salary for their services, to be determined annually.

- Distribution Policy: Outline how and when distributions of profit will be made to the shareholders.

- Buy-Sell Provisions: This is critical for multi-owner S-Corps. What happens if a partner wants to leave, dies, or gets divorced? A buy-sell agreement funded by life insurance is a non-negotiable part of a mature business structure.

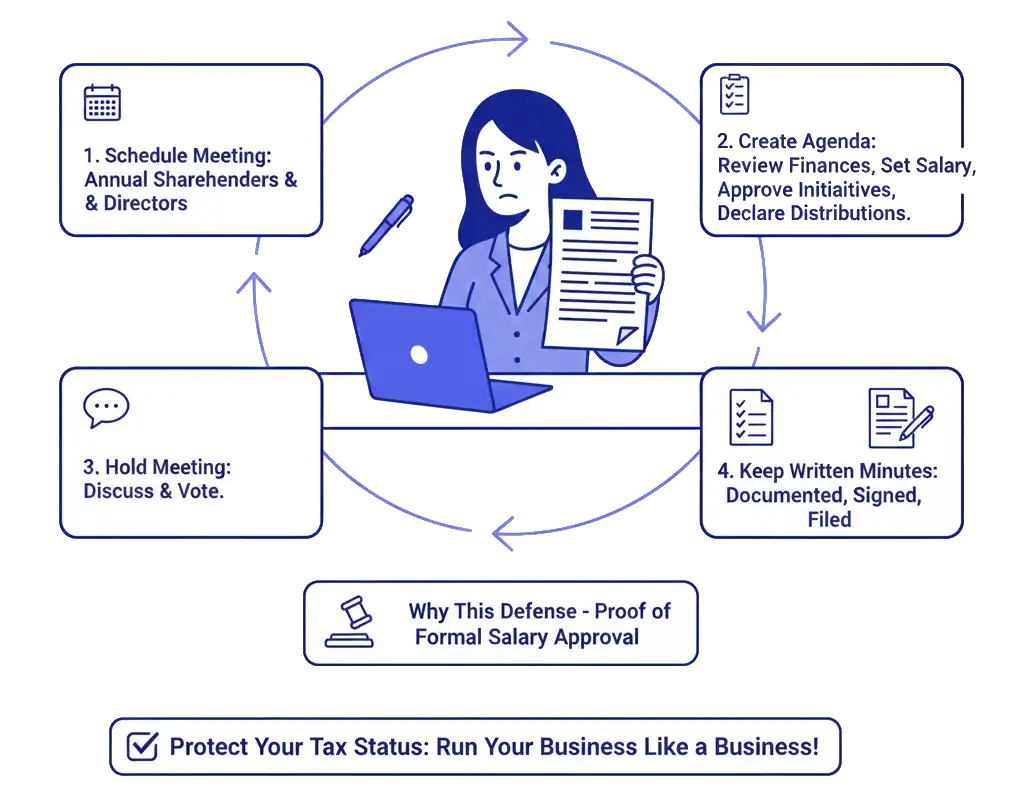

2. Holding Annual Meetings and Keeping Minutes

This is the formality that most small business owners skip, and it is a major mistake. You must hold at least one formal meeting of the shareholders and board of directors each year. Yes, even if you are the only person in the room.

- The Process:

- 1. Schedule the Meeting: Formally schedule an "Annual Meeting of the Board of Directors & Shareholders."

- 2. Create an Agenda: The agenda should include key items like:

- Review of the previous year’s financial performance.

- Setting or confirming the reasonable salary for the owner-employee(s) for the upcoming year.

- Approving any major business initiatives or purchases.

- Declaring any planned distributions.

- 3. Hold the Meeting: Discuss the agenda items.

- 4. Keep Written Minutes: This is the most important part. You must create a formal document called “Minutes of the Annual Meeting.” The minutes should document the date of the meeting, who was present, what was discussed, and what was voted on and approved. These minutes are then signed and placed in your corporate records.

Why This Matters: In an audit, the first thing an agent may ask for is your corporate minutes. Producing a professional set of minutes showing that you formally approved your salary is a powerful piece of evidence that you are respecting the corporate form.

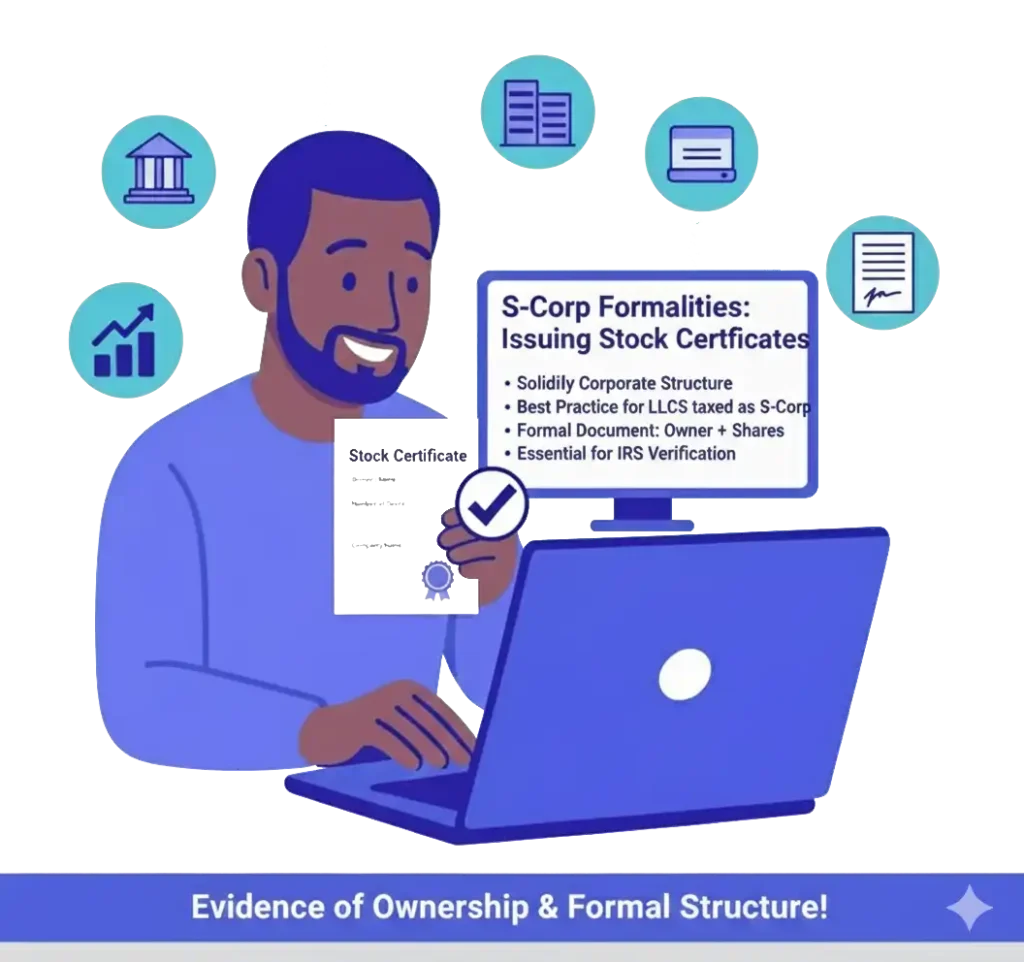

3. Issuing Stock Certificates

While an LLC has “membership units,” an S-Corp has stock. It is a best practice for an LLC taxed as an S-Corp to formally issue stock certificates to its owners. This further solidifies the corporate structure in the eyes of the IRS. A stock certificate is a simple document that states the name of the owner and the number of shares they own.

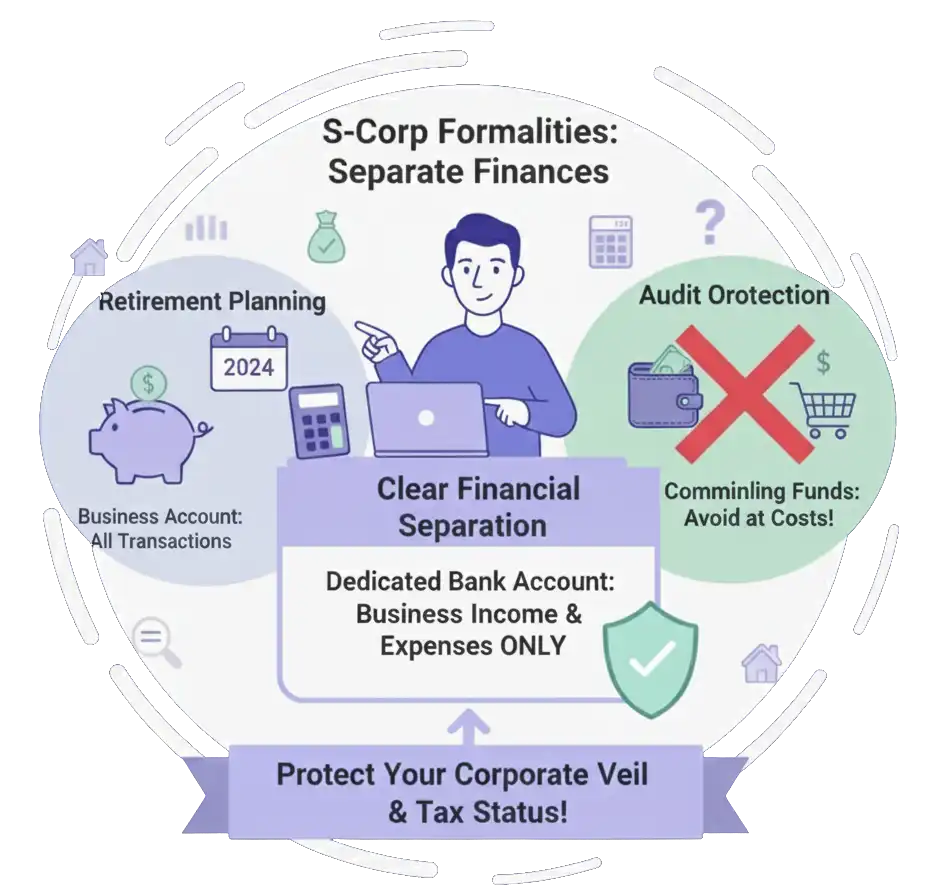

4. Maintaining Separate Finances

This is the most fundamental and non-negotiable of all corporate formalities. You must have a dedicated bank account for your S-Corp. All business income must be deposited into this account, and all business expenses must be paid from it.

Commingling funds is the cardinal sin of corporate formalities. Paying for your personal groceries with your business debit card or paying a business expense from your personal account may seem harmless, but it creates a crack in your corporate veil. It tells the IRS that you do not see a real distinction between yourself and the business, so why should they? In an audit, a pattern of commingling funds can be used to disallow your S-Corp status entirely

By diligently following these formalities, you are building a fortress around your business. You are creating a clear, documented record that proves you are a serious business owner who respects the rules. This not only provides you with near-impenetrable audit protection but also instills a level of financial discipline that is essential for long-term growth andterm growth and success.

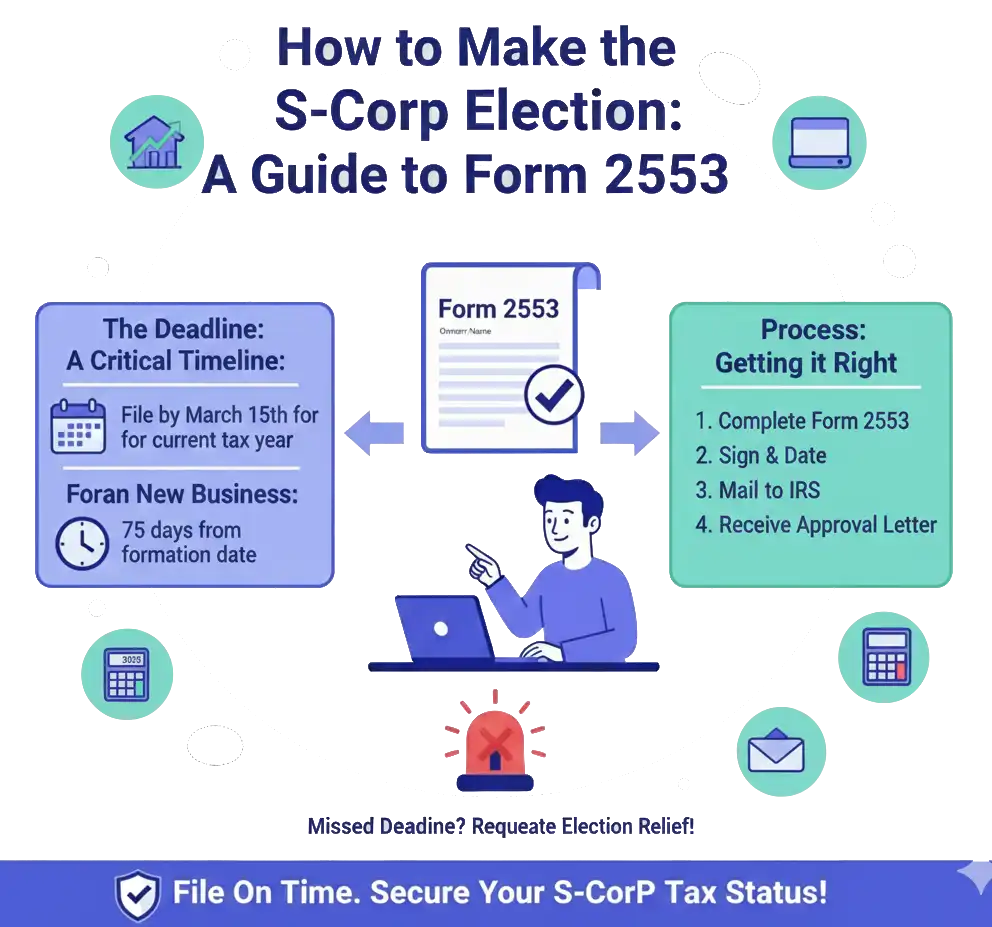

How to Make the S-Corp Election: A Guide to Form 2553

Making the S-Corp election is done by filing Form 2553, “Election by a Small Business Corporation,” with the IRS. This form is your formal request to have your LLC treated as an S Corporation for tax purposes. While the form itself is only a few pages long, getting it right is critical.

The Deadline: A Critical Timeline

- Timing is everything with the S-Corp election. The IRS has strict deadlines:

- For an Existing Business: If you have an existing LLC or C-Corporation that you want to convert to an S-Corp for the current tax year, you must file Form 2553 by March 15th of that year. For the election to be effective for all of 2024, you must have filed by March 15, 2024.

- For a New Business: If you are just starting your LLC, you have a window of two months and 15 days (75 days) from your official date of formation to file Form 2553 and have it be effective from day one.

- Late Election Relief: A Powerful Safety Net

What happens if you miss the deadline? For many years, this was a significant and often irreversible problem. However, the IRS has provided a generous and powerful safety net: Revenue Procedure 2013-30. This procedure allows for late S-Corp election relief if you can show that you had “reasonable cause” for failing to file on time.

- What constitutes reasonable cause?

- You were unaware of the need to file the election.

- You received incorrect advice from a tax professional

- You were simply not aware of the significant tax savings and would have filed had you known.

How to Request Late Relief:

If you are filing late, you do not need to file a separate request for relief. You simply file the completedForm 2553 and write at the top of the form: “FILED PURSUANT TO REV. PROC. 2013-30.”

You must also attach a statement to the form explaining why you had reasonable cause for filing late. This statement should be sincere and to the point. For example: “I was not aware of the S-Corporation election and its potential tax savings until I consulted with a new tax advisor on [Date]. Had I been aware, I would have timely filed the election.”

This late election relief is a game-changer. It means that even if you are reading this in November, you can still potentially make the S-Corp election for the entire current year and unlock thousands of dollars in tax savings you thought were lost.

Where to File:

Form 2553 must be filed with a specific IRS service center depending on where your business is located. You can find the correct address on the IRS website or in the instructions for Form 2553. It is highly recommended that you file by certified mail with a return receipt to have a legal record that the IRS received your election.

While you can technically fill out and file Form 2553 yourself, it is highly recommended that you do so with the guidance of a qualified tax professional. They can ensure the form is filled out correctly, that you meet all the eligibility requirements, and that you properly file for late election relief if necessary. This is a step that is too important to get wrong.

The Final Verdict: A Decision-Making Framework

The choice between a default LLC and an S-Corp is one of the most consequential financial decisions a business owner will make. But it doesn’t have to be complicated.

The Core Logic: If your business consistently generates over $60,000 in net profit per year, the S-Corp election is almost certainly the correct financial move. The tax savings will far outweigh the administrative costs.

Address the Fear: The primary reason business owners hesitate is fear of complexity. They worry about payroll, the separate tax return, and doing something wrong. But you must reframe this. The administrative tasks are a system, and systems can be learned and managed. The cost of a good CPA and a payroll service is not an expense; it is an investment with a 200%, 500%, or even 1,000% annual return in the form of tax savings.

The Next Step: This decision should not be made in a vacuum based on a single article. The logical next step is to get a professional analysis of your specific situation. A qualified tax strategist can project your exact tax savings, help you determine a defensible reasonable salary, and map out the entire implementation plan.

Stop leaving a tip for the IRS. The tax code is written to provide strategic advantages to business owners who are proactive and informed. The S-Corp election is the single most powerful advantage available to a profitable LLC owner.

Let’s find out exactly how much you could be saving.

A Tale of Three Tax Bills: Case Studies at Every Level

To truly understand the power of the S-Corp election, we need to move beyond simple examples and look at detailed, real-world scenarios. We will follow three different business owners at three distinct profit levels to see how this single decision impacts their take-home pay, their financial strategy, and their ability to build wealth.

Case Study 1: The Rising Freelancer – $80,000 in Net Profit

The Owner: Meet Alex, a talented freelance web developer. After years of building a client base, Alex’s single-member LLC had a breakout year, netting $80,000 after all business expenses. Alex lives in a state with a 5% income tax and is single.

- The Default LLC Path:

Alex sticks with the default sole proprietorship taxation. The math is straightforward and brutal.

- 1. Self-Employment Tax: The IRS demands its 15.3% cut for Social Security and Medicare on nearly all of the profit.

- Profit Subject to SE Tax: $80,000 * 92.35% = $73,880

- SE Tax Owed: $73,880 * 15.3% = $11,304

- 2. Federal Income Tax: Alex gets the standard deduction and the QBI deduction

- Adjusted Gross Income (AGI): $80,000 - (1/2 of SE Tax of $5,652) = $74,348

- QBI Deduction: 20% of $73,880 = $14,776

- Taxable Income: $74,348 - $14,776 (QBI) - $14,600 (Standard Deduction) = $44,972

- Federal Income Tax Owed: ~$5,561

- 3. State Income Tax:

- State Taxable Income: ~$68,000 (varies by state rules)

- State Income Tax Owed: ~$3,400

👉Total Tax Bill: ~$20,265

👉Effective Tax Rate: 25.3%

👉Take-Home Pay: $59,735

- The S-Corp Strategy Path:

Alex consults a tax strategist and elects to be taxed as an S-Corp. They determine a reasonable salary for a web developer in his area is $50,000.

- 1. Payroll Tax (FICA): This is the 15.3% tax, but only on the salary.

- FICA Tax on $50,000 Salary: $7,650

- 2. Federal Income Tax:

- AGI: $50,000 (Salary) + $30,000 (Distribution) = $80,000

- QBI Deduction: 20% of the $30,000 in pass-through profit = $6,000

- Taxable Income: $80,000 - $6,000 (QBI) - $14,600 (Standard Deduction) = $59,400

- Federal Income Tax Owed: ~$8,052

- 3. State Income Tax:

- State Taxable Income: ~$74,000

- State Income Tax Owed: ~$3,700

👉Total Tax Bill: ~$19,402

👉Effective Tax Rate: 24.2%

👉Take-Home Pay: $60,598

The Analysis:

Even at this level, the S-Corp election provides a net savings of $863, even after accounting for an estimated $2,000 in payroll and accounting fees. More importantly, it establishes a scalable system. As income grows, the savings will explode.

Case Study 2: The Thriving Agency - $250,000 in Net Profit

The Owner: Meet Maria, the founder of a successful digital marketing agency. Her LLC, taxed as an SCorp, nets $250,000.

- The Default LLC Path (Hypothetical):

- If Maria had remained a default LLC, her tax situation would be painful.

- 1. Self-Employment Tax:

- The 12.4% Social Security tax applies up to the $168,600 wage base for 2024. The 2.9% Medicare tax applies to all of it.

- SE Tax Calculation: ($168,600 * 15.3%) + (($250,000 * 92.35%) - $168,600) * 2.9% = $25,796 + $1,804 = $27,600 (approx.)

- The S-Corp Strategy Path

Maria pays herself a reasonable salary of $120,000 for her role as CEO and lead strategist.

- 1. Payroll Tax (FICA):

- FICA on $120,000 Salary: $18,360

- 2. The Savings:

- SE Tax as Default LLC: $27,600

- FICA Tax as S-Corp: $18,360

- Annual Self-Employment Tax Savings: $9,240

- The Lifestyle Impact:

- What does an extra $9,240 a year mean for Maria? It’s not just a number on a spreadsheet. It’s:

- A fully funded family vacation to Europe, every single year.

- The ability to max out a Roth IRA for both herself and her spouse.

- The down payment on a rental property every two to three years, accelerating her path to financial freedom.

- This is the tangible result of a single strategic decision.

Case Study 3: The E-commerce Mogul - $1,000,000 in Net Profit

The Owner: Meet David, whose e-commerce brand has exploded, netting $1,000,000 this year.

The Default LLC Path (Hypothetical):

- 1. Self-Employment Tax:

- The calculation is complex, but the result is a massive tax bill.

- SE Tax Owed: ~$45,354

- The S-Corp Strategy Path:

David’s role is primarily strategic CEO. He sets a reasonable salary of $250,000.

- 1. Payroll Tax (FICA):

- The Social Security portion is capped at the $168,600 wage base

- FICA Owed: ($168,600 * 15.3%) + (($250,000 - $168,600) * 2.9%) = $25,796 + $2,360 = $28,156

- The Savings:

- SE Tax as Default LLC: $45,354

- FICA Tax as S-Corp: $28,156

- Annual Self-Employment Tax Savings: $17,198

- The Strategic Implications:

- For David, the $17,198 in annual savings is significant, but the S-Corp structure provides even greater strategic advantages at this level:

- Retirement Planning: The S-Corp salary allows David to implement a Solo 401(k) and contribute the maximum as both "employee" and "employer," potentially sheltering over $69,000 per year from tax

- Health Insurance: He can use the S-Corp to deduct 100% of his family's health insurance premiums through the W-2 process

- Audit Protection: The formal structure of the S-Corp, with its clear distinction between salary and distributions, provides a much stronger defense in the event of an IRS audit compared to a highincome sole proprietorship.

For high-income earners, the S-Corp is not just a tax-saving tool; it is a foundational element of a

comprehensive wealth-building and asset-protection strategy.

The S-Corp Basis Deep Dive: A Trap for the Unwary

“Basis” is one of the most critical and misunderstood concepts for S-Corp owners. In simple terms, your basis is your financial stake in the company. It is the well from which you can draw tax-free distributions. If you take distributions when the well is dry (i.e., you have no basis), those distributions become taxable income. This is a tripwire that can turn your tax-saving strategy into a tax nightmare.

- How Basis is Calculated:

Your initial basis is the amount of money and property you contributed to start the company. From there, it is a running, year-by-year calculation:

Basis Increases With:

- Additional capital contributions you make.

- Your pro-rata share of the company's profits (the net income on your Schedule K-1).

- Loans you personally make to the corporation.

Basis Decreases With:

- Distributions you take (but not below zero).

- Your pro-rata share of the company's losses.

- Repayment of loans you made to the corporation.

A Multi-Year Basis Tracking Example:

Let’s follow a business owner, Jane, over three years to see how basis works in practice.

- Year 1: Formation and Profit

- Jane starts her S-Corp with a $10,000 personal investment. Her initial basis is $10,000.

- The business has a successful first year, with a net profit of $80,000. This is reported on her K-1.

- Her basis increases by the profit: $10,000 + $80,000 = $90,000.

- Jane takes a distribution of $40,000.

- Her year-end basis is: $90,000 - $40,000 = $50,000. The distribution is completely tax-free.

- Year 2: A Business Loss

- The market takes a downturn, and the business has a net loss of $20,000.

- Her basis decreases by the loss: $50,000 - $20,000 = $30,000.

- Jane needs money to live, so she takes a distribution of $35,000.

- The Basis Trap is Sprung!

- The first $30,000 of the distribution is a tax-free return of her basis. Her basis is now $0.

- The remaining $5,000 is a distribution in excess of basis. This amount is not tax-free. It will be reported on her personal tax return as a long-term capital gain.

- Year 3: Recovery and a Loan

- Jane's basis starts at $0.

- To get through a slow period, Jane personally loans the company $15,000. This is a formal loan with a promissory note. This loan increases her basis to $15,000.

- The business recovers and has a net profit of $100,000.

- Her basis increases: $15,000 + $100,000 = $115,000.

- She takes a distribution of $60,000.

- Her year-end basis is: $115,000 - $60,000 = $55,000. The distribution is tax-free.

- Why This Matters:

Accurate basis tracking is not optional. It is a legal requirement for every S-Corp shareholder. Your tax preparer should be updating your basis schedule every single year. If they are not, it is a major red flag. Without this calculation, you are flying blind and risk turning tax-free distributions into a surprise tax bill.

S-Corp Formalities: Respecting the Corporate Veil

When you elect to have your LLC taxed as an S-Corporation, you are asking the IRS to treat your business as a corporation for tax purposes. This is a privilege, and it comes with the expectation that you will respect the corporate form. This means running your business with a certain level of formality that is not required of a default LLC. Failure to do so can give the IRS a powerful argument to “pierce the corporate veil.” This is a legal concept that essentially says you have not been acting like a real business, and therefore, you do not deserve the tax benefits or liability protection of one.

Here is a guide to the essential corporate formalities you must follow.

1. A Comprehensive Operating Agreement

While all LLCs should have an operating agreement, it is absolutely critical for an LLC taxed as an S-Corp. This internal document is the constitution of your business. It should be far more detailed than a simple template.

- What to Include:

- Ownership and Share Structure: Clearly define who the owners (shareholders) are and the number of shares each owns. Even if you are the sole owner, you should formally issue 100% of the shares to yourself.

- Management Structure: Detail who is responsible for managing the business. Will it be managed by the members (owners) or by appointed managers?

- Reasonable Compensation Clause: Include a clause stating that all owner-employees will be paid a reasonable salary for their services, to be determined annually.

- Distribution Policy: Outline how and when distributions of profit will be made to the shareholders.

- Buy-Sell Provisions: This is critical for multi-owner S-Corps. What happens if a partner wants to leave, dies, or gets divorced? A buy-sell agreement funded by life insurance is a non-negotiable part of a mature business structure.

2. Holding Annual Meetings and Keeping Minutes

This is the formality that most small business owners skip, and it is a major mistake. You must hold at least one formal meeting of the shareholders and board of directors each year. Yes, even if you are the only person in the room.

- The Process:

- Schedule the Meeting: Formally schedule an "Annual Meeting of the Board of Directors & Shareholders."

- Create an Agenda: The agenda should include key items like:

- Review of the previous year’s financial performance.

- Setting or confirming the reasonable salary for the owner-employee(s) for the upcoming year.

- Approving any major business initiatives or purchases.

- Declaring any planned distributions.

- Hold the Meeting: Discuss the agenda items.

- Keep Written Minutes:This is the most important part. You must create a formal document called “Minutes of the Annual Meeting.” The minutes should document the date of the meeting, who was present, what was discussed, and what was voted on and approved. These minutes are then signed and placed in your corporate records.

- Why This Matters:

In an audit, the first thing an agent may ask for is your corporate minutes. Producing a professional set of minutes showing that you formally approved your salary is a powerful piece of evidence that you are respecting the corporate form.

[DOWNLOAD: Sample Annual Meeting Minutes Template]

3. Issuing Stock Certificates

While an LLC has “membership units,” an S-Corp has stock. It is a best practice for an LLC taxed as an S-Corp to formally issue stock certificates to its owners. This further solidifies the corporate structure in the eyes of the IRS. A stock certificate is a simple document that states the name of the owner and the number of shares they own.

4. Maintaining Separate Finances

This is the most fundamental and non-negotiable of all corporate formalities. You must have a dedicated business bank account for your S-Corp. All business income must be deposited into this account, and all business expenses must be paid from it.

Commingling funds is the cardinal sin of corporate formalities. Paying for your personal groceries with your business debit card or paying a business expense from your personal account may seem harmless, but it creates a crack in your corporate veil. It tells the IRS that you do not see a real distinction between yourself and the business, so why should they? In an audit, a pattern of commingling funds can be used to disallow your S-Corp status entirely.

By diligently following these formalities, you are building a fortress around your business. You are creating a clear, documented record that proves you are a serious business owner who respects the rules. This not only provides you with near-impenetrable audit protection but also instills a level of financial discipline that is essential for long-term growth andterm growth and success.

The Final Verdict: A Decision-Making Framework

The choice between a default LLC and an S-Corp is one of the most consequential financial decisions a business owner will make. But it doesn’t have to be complicated.

The Core Logic: If your business consistently generates over $60,000 in net profit per year, the S-Corp election is almost certainly the correct financial move. The tax savings will far outweigh the administrative costs.

Address the Fear: The primary reason business owners hesitate is fear of complexity. They worry about payroll, the separate tax return, and doing something wrong. But you must reframe this. The administrative tasks are a system, and systems can be learned and managed. The cost of a good CPA and a payroll service is not an expense; it is an investment with a 200%, 500%, or even 1,000% annual return in the form of tax savings.

The Next Step: This decision should not be made in a vacuum based on a single article. The logical next step is to get a professional analysis of your specific situation. A qualified tax strategist can project your exact tax savings, help you determine a defensible reasonable salary, and map out the entire implementation plan. Stop leaving a tip for the IRS. The tax code is written to provide strategic advantages to business owners who are proactive and informed. The S-Corp election is the single most powerful advantage available to a profitable LLC owner.

Let’s find out exactly how much you could be saving