2026 Ohio Opportunity Zone Tax Deferral: Strategy Guide for Business Owners & Real Estate Investors

2026 Ohio Opportunity Zone Tax Deferral: Strategy Guide for Business Owners & Real Estate Investors

For the 2026 tax year, opportunity zone tax deferral strategies in Ohio present one of the most overlooked wealth-building tools available to business owners, real estate investors, and high-net-worth individuals. Under federal Section 1400Z regulations, investors can defer capital gains taxes indefinitely by reinvesting profits into designated economic zones—including dozens of communities across Ohio. This comprehensive guide reveals how to structure opportunity zone investments, maximize tax benefits, and avoid costly mistakes in 2026.

Table of Contents

- Key Takeaways

- What Are Opportunity Zones and How Do They Work?

- Which Ohio Communities Qualify as Opportunity Zones in 2026?

- How Does Capital Gains Tax Deferral Work Under Section 1400Z?

- What Investments Qualify for Opportunity Zone Benefits?

- Step-by-Step: Making the Opportunity Zone Election for 2026

- Real-World Tax Savings Scenarios for Ohio Investors

- Uncle Kam in Action

- Next Steps

- Frequently Asked Questions

Key Takeaways

- Opportunity zones allow you to defer capital gains taxes indefinitely by reinvesting profits into designated Ohio communities before December 31, 2026.

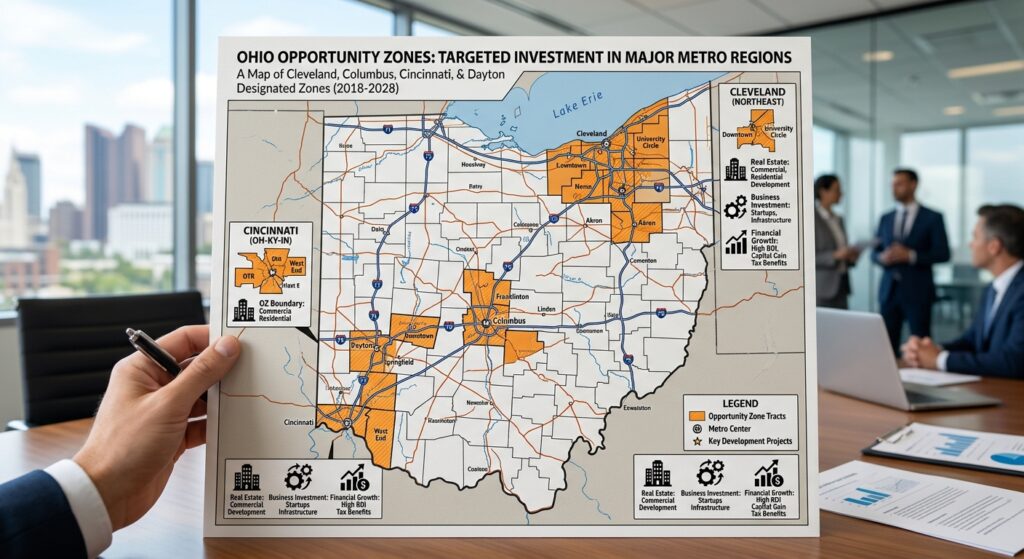

- Ohio has 158 designated opportunity zones, with significant concentrations in Cleveland, Columbus, Cincinnati, and Dayton metro areas.

- A 10-year holding period can potentially eliminate capital gains taxes entirely on profits earned within the opportunity zone.

- You must make the election within 180 days of receiving capital gains to qualify for the deferral benefit.

- Both business owners and real estate investors can deploy opportunity zone strategies for maximum 2026 tax efficiency.

What Are Opportunity Zones and How Do They Work?

Quick Answer: Opportunity zones are economically disadvantaged areas designated by the IRS where investors can defer, reduce, or eliminate capital gains taxes by reinvesting profits into qualifying businesses and real estate. Created under Section 1400Z in 2017, the program continues to offer substantial tax incentives in 2026.

Opportunity zones represent a federal tax incentive designed to stimulate economic development in lower-income communities. The program, codified under IRS Section 1400Z, allows investors to reinvest capital gains into these designated areas and receive significant tax benefits in return.

The core mechanism is straightforward: when you sell an asset and realize a capital gain, you have 180 days to reinvest that gain into a qualified opportunity zone investment. Once invested, the clock starts on a preferential tax timeline. Unlike traditional investments where you owe capital gains taxes immediately, opportunity zone investments allow you to defer these taxes for up to 15 years—or potentially eliminate them entirely under current law.

The Three-Phase Tax Benefit Structure

Opportunity zones operate through a tiered tax benefit system. In Phase 1, lasting five years, you defer taxes on your original capital gains. In Phase 2, from year five through year seven, you gain a temporary 15% exclusion on the original gain amount. In Phase 3, after holding your investment for 10 years, any gains earned within the opportunity zone itself become permanently tax-free. For 2026 investors, understanding these phases is critical for planning your exit strategy.

Why Ohio Opportunity Zones Matter for Your Portfolio

Ohio’s opportunity zones span economically diverse regions—from manufacturing hubs like Cleveland to emerging tech corridors in Columbus and Cincinnati. With 158 designated tracts across the state, Ohio offers investors unprecedented flexibility in choosing investment locations aligned with their portfolio strategy. Many of these zones are already experiencing revitalization, making them attractive for both tax benefits and genuine economic upside.

Which Ohio Communities Qualify as Opportunity Zones in 2026?

Quick Answer: Ohio has 158 designated opportunity zone tracts across 57 counties, including major urban areas (Cleveland, Columbus, Cincinnati, Dayton) and rural communities. The complete list is available on the IRS website and through state development agencies.

Ohio’s opportunity zones are strategically distributed across the state. The Cleveland metro area has approximately 40 designated tracts, capturing neighborhoods undergoing significant redevelopment. Columbus—the state’s capital and fastest-growing major city—contains around 25 opportunity zone tracts, many in the Arena District and nearby emerging neighborhoods. Cincinnati and Dayton each have substantial designations, as do smaller cities like Akron, Toledo, and Youngstown.

Rural and small-town Ohio also benefits from the program. Many agricultural counties have designated opportunity zones, making the strategy available to investors with diverse portfolio goals. Before committing capital in 2026, verify your target investment location using the IRS’s opportunity zone census tract list, which identifies all qualifying areas nationwide.

| Major Ohio Metro Area | Approximate Opportunity Zone Tracts | Key Investment Sectors |

|---|---|---|

| Cleveland | 40+ | Real estate redevelopment, tech startups, healthcare |

| Columbus | 25+ | Commercial real estate, fintech, entertainment |

| Cincinnati | 18+ | Riverfront development, biotechnology, food/beverage |

| Dayton | 12+ | Manufacturing, advanced materials, aerospace |

How Does Capital Gains Tax Deferral Work Under Section 1400Z?

Quick Answer: When you reinvest capital gains into an opportunity zone within 180 days, you defer the tax on that gain until the earlier of December 31, 2026, or when you sell your opportunity zone investment. This creates powerful cashflow and compounding advantages for savvy investors.

The mechanics of opportunity zone tax deferral differ fundamentally from standard capital gains treatment. Normally, when you sell an asset and realize a gain, you owe federal income tax that same year. The IRS taxes long-term capital gains at preferential rates (15% or 20% for high-income earners), but the tax is still due.

With opportunity zones, the deferral period begins the moment you make the reinvestment election. For 2026 investors, this deferral extends until December 31, 2026—creating a critical planning deadline. After that date, your deferred gains face taxation at ordinary income rates, unless you’ve held the opportunity zone investment for the full holding period.

The 180-Day Election Window

The most critical deadline in opportunity zone planning is the 180-day election window. Beginning from the date you recognize the capital gain (sale close date), you have exactly 180 calendar days to reinvest that gain into a qualified opportunity zone fund or investment. Miss this deadline by even one day, and the deferral benefit is lost. For 2026 transactions, calculating this date precisely is essential.

Example: You sell a commercial property on June 1, 2026, recognizing a $500,000 capital gain. Your 180-day window closes on November 29, 2026. You must have reinvested that $500,000 into a qualified opportunity zone investment by November 29 to qualify for deferral. Even investing on November 30 would disqualify the strategy.

The December 31, 2026 Tax Recognition Date

An additional complexity affects 2026 planners. Current law specifies that if you don’t hold your opportunity zone investment until its required holding period conclusion, your deferred gains become taxable on December 31, 2026. This means any 2026 investor who needs liquidity before that date faces immediate tax recognition on deferred gains—a situation that requires careful planning with experienced tax advisors.

What Investments Qualify for Opportunity Zone Benefits?

Free Tax Write-Off Finder

Free Tax Write-Off FinderQuick Answer: Qualified investments include ownership stakes in Opportunity Zone Funds (OZFs), direct real estate purchases in opportunity zone areas, and interests in qualified businesses operating within designated zones. Both active and passive strategies qualify for 2026.

Not all investments in opportunity zone areas receive the same tax treatment. The IRS restricts the definition of “qualified opportunity zone property” to ensure capital actually drives economic development. Understanding what qualifies is essential to avoid accidentally forfeiting tax benefits.

Qualified Opportunity Zone Funds (OZFs)

The most common vehicle for opportunity zone investing is a Qualified Opportunity Zone Fund (OZF). These are investment partnerships or corporations that hold property and businesses exclusively within designated opportunity zones. By investing through an OZF, you gain the deferral benefit while pooling capital with other investors to access larger deals.

OZFs must have at least 90% of their assets invested in qualified opportunity zone property. This requirement ensures that when you invest in an OZF, your capital is truly deployed in the designated areas. As of 2026, hundreds of registered OZFs operate across Ohio, ranging from commercial real estate funds to operating business vehicles.

Direct Real Estate Investments

Many investors prefer direct real estate ownership within opportunity zones. For example, you might purchase an apartment complex in Cleveland’s opportunity zone, or acquire commercial office space in Columbus. Direct ownership qualifies for the deferral benefit provided the property is located within a designated zone and meets “use” requirements—meaning it’s actively developed or improved as real estate rather than held vacant.

Direct investments offer greater control but require capital and expertise. Many investors combine direct ownership with OZF investments to diversify across property types and geographies within Ohio’s opportunity zone network.

Qualified Operating Businesses

Opportunity zone investing extends beyond real estate to operating businesses. If you purchase an equity stake in a business that operates within an opportunity zone and meets size requirements, your investment qualifies for deferral benefits. This includes technology startups, manufacturing operations, retail businesses, and service providers.

Owning a piece of a high-growth Ohio startup or regional business can deliver both tax deferral and genuine economic upside, making business ownership an attractive opportunity zone strategy for growth-oriented investors.

Step-by-Step: Making the Opportunity Zone Election for 2026

Quick Answer: Making an opportunity zone election requires identifying a qualified investment, reinvesting capital within 180 days of your original gain, and properly documenting the election on your 2026 tax return (Form 8949 or Schedule D).

The process of electing opportunity zone deferral involves several sequential steps. Each step has legal and tax compliance requirements that must be followed precisely to preserve benefits.

Step 1: Identify and Realize Your Capital Gain

The process begins when you recognize a capital gain. This happens on the sale closing date of any asset—real estate, stock, business interest, or appreciated personal property. Document the gain amount carefully, as it determines the maximum deferral amount. For 2026 investors, realize that gains are taxable in the year of sale regardless of opportunity zone elections.

Step 2: Locate a Qualified Investment Vehicle

Next, identify your investment target—an OZF, direct property, or business. Research available options across Ohio’s designated opportunity zones. This might involve reviewing IRS resources, consulting state development agencies, or working with specialized investment advisors. Your choice determines not just tax treatment but also your investment returns.

Step 3: Execute the Investment Within 180 Days

You have exactly 180 days from your gain recognition date to reinvest the capital. This isn’t a filing deadline—it’s a transaction deadline. The money must actually be invested and funds transferred. Failing to invest by day 180 disqualifies the deferral, making this deadline non-negotiable.

Step 4: File the Election on Your Tax Return

When filing your 2026 tax return, you must document the opportunity zone election. This is typically done on Form 8949 or Schedule D, identifying the original gain and the election to defer. Proper documentation is critical—the IRS has issued detailed guidance on required disclosures.

Real-World Tax Savings Scenarios for Ohio Investors

Quick Answer: A business owner who sells appreciated stock for $1,000,000 and reinvests into an Ohio opportunity zone can defer $200,000+ in federal taxes while potentially building wealth in emerging communities.

Scenario 1: Real Estate Investor in Cleveland Metro Opportunity Zones

Sarah, a seasoned real estate investor, sells a rental property in Columbus for $800,000, realizing a $300,000 capital gain. At the 20% federal long-term capital gains rate, she faces approximately $60,000 in immediate federal tax liability. Instead, Sarah reinvests the full $300,000 gain into a Cleveland opportunity zone apartment complex within 150 days. By making the election on her 2026 tax return, Sarah defers the $60,000 federal tax bill. If she holds the investment for 10 years, the gains earned within the opportunity zone are permanently tax-free—potentially worth an additional $100,000+ in tax savings if the property appreciates.

Scenario 2: Business Owner Deploying Stock Sale Proceeds

Marcus, a successful entrepreneur, sells his stake in a business for $2,500,000, generating a $1,200,000 capital gain. Federal taxes alone would total $240,000 (at the 20% rate), plus state taxes, totaling $300,000+ in annual tax liability. Instead, Marcus works with an investment advisor to identify a Columbus-based tech fund investing in opportunity zone startups. He reinvests $1,200,000 within 180 days, deferring the $300,000 tax bill. His investment vehicle operates multiple startups within opportunity zones, providing diversification while building future wealth in high-growth companies.

Scenario 3: Multi-Asset Liquidation Strategy

A family office liquidates $5,000,000 in appreciated securities, recognizing $1,800,000 in gains. Rather than paying $360,000+ in immediate federal taxes, the office coordinates reinvestments across multiple Ohio opportunity zones: $750,000 into Cincinnati commercial real estate, $600,000 into a Dayton-based manufacturing business, and $450,000 into a Columbus opportunity zone fund. By structuring multiple 180-day elections, the family defers $360,000 in taxes while deploying capital across Ohio’s economic development zones.

Pro Tip: Combine opportunity zone deferral with other business tax strategies. If you own an S Corp or LLC, consider how opportunity zone investments interact with your entity structure. Some investors find that maximizing 2026 opportunity zone deployments alongside generous Section 179 expensing (up to $2.5 million for 2026 under the One Big Beautiful Bill Act) creates compound tax savings.

Uncle Kam in Action: Real Estate Investor Defers $85,000 in Annual Taxes

Client Profile: David, a Columbus-based real estate developer, had accumulated five commercial properties over 15 years. In early 2026, he sold two properties for a combined $2,100,000, realizing net capital gains of $425,000. His federal tax liability approached $85,000 (at combined rates including state taxes).

The Challenge: David wanted to redeploy capital into new real estate investments but faced an immediate $85,000 tax hit that would reduce his available deployment capital. Additionally, his concentrated real estate portfolio exposed him to market risk—he needed diversification while still maintaining control over his investments.

The Solution: Uncle Kam recommended an opportunity zone strategy. Rather than reinvesting all capital into a single property, David structured a two-part plan: (1) $250,000 reinvested into a Cincinnati opportunity zone fund managing mixed-use development; (2) $175,000 deployed into a Columbus opportunity zone commercial property he would actively manage. This approach deferred the $85,000 in taxes while providing portfolio diversification.

The Results: By executing this strategy within the 180-day window, David deferred $85,000 in annual taxes, preserving that capital for additional opportunities. After five years, he reevaluates his holdings—the opportunity zone fund appreciated 22%, while his direct Columbus property appreciated 18%. When David eventually exits the opportunity zone investments after their required holding periods, he’s positioned to claim permanent tax elimination on the gains earned within the zones themselves. Total first-year impact: $85,000 deferred in taxes, plus diversified portfolio growth exceeding 20%.

Fee Invested: $2,500 in tax planning and structuring. Return on Investment: $85,000 deferred ÷ $2,500 invested = 3,400% first-year ROI.

Next Steps

- Audit Your 2026 Gains: Document any capital gains you’ve realized or will realize in 2026. Calculate your tax liability at both federal and state levels to understand the deferral potential.

- Identify Ohio Opportunity Zones: Review the IRS’s opportunity zone census list and determine if your target investments align with your capital deployment timeline and risk tolerance.

- Map Your 180-Day Timeline: Create a calendar showing your gain recognition dates and corresponding 180-day reinvestment deadlines. Missing even one deadline disqualifies the entire strategy.

- Consult a Tax Professional: Before executing opportunity zone investments, work with a tax advisor experienced in Section 1400Z strategy to ensure proper structuring and compliance. Uncle Kam’s tax preparation services in Ohio specialize in opportunity zone tax deferral strategies for business owners and real estate investors.

- Execute Within 180 Days: Once you’ve identified your investment opportunity, ensure funds transfer and investment documentation is complete before your 180-day deadline expires.

Frequently Asked Questions

Can I Use Opportunity Zone Deferrals if I Don’t Sell a Business or Asset in 2026?

The opportunity zone deferral requires an actual capital gain recognized within the prior year. If you haven’t sold an appreciated asset, you don’t have a “gain” to reinvest. However, you can still invest in opportunity zones directly—you just won’t receive the deferral benefit. For example, if you have $500,000 in cash savings and invest it in an opportunity zone, you benefit from the 10-year gain exclusion, but you don’t get a deferral of previously taxed gains.

What Happens if My Opportunity Zone Investment Declines in Value?

Like any investment, opportunity zone assets can depreciate. If your $500,000 reinvestment declines to $400,000, you still owe tax on the original $500,000 gain when the deferral period ends (December 31, 2026, for 2026 investments, or upon sale). However, you can claim a capital loss on the $100,000 decline. The deferral benefit doesn’t protect you from market risk.

Are Ohio State Taxes Deferred Along with Federal Taxes?

The opportunity zone deferral is a federal tax strategy under Section 1400Z. Ohio, however, does not automatically conform to this deferral. You may still owe Ohio state income tax on your original gain in the year of sale. Ohio’s income tax rate averages 2.58% (per 2026 data), meaning additional state taxes of $12,900 on a $500,000 gain. Consult with a state tax specialist to determine your Ohio tax position.

What if I Need to Access My Opportunity Zone Investment Before 10 Years?

If you sell your opportunity zone investment before reaching the required holding period, your deferred gains become immediately taxable. For 2026 investments, this means taxes would be due by December 31, 2026. You lose the benefit of deferral and any future gain exclusions. This is why opportunity zone strategy works best for patient capital with a 5-10 year investment horizon.

Can I Use Opportunity Zones if I Have Losses From Other Investments?

Capital losses offset capital gains dollar-for-dollar. If you have $500,000 in gains and $200,000 in losses, your net capital gain is $300,000. You can reinvest the $300,000 net gain into an opportunity zone and benefit from deferral on that amount. Losses don’t disqualify the strategy—they reduce the gain subject to deferral.

Are There Income Limits or Restrictions on Who Can Use Opportunity Zones?

Unlike many tax benefits, opportunity zones have no income limits. High-net-worth individuals, corporations, partnerships, and trusts can all use the strategy. The only restriction is on investments—your money must be deployed into qualified opportunity zone property. Individual investor wealth and income don’t limit eligibility.

Can I Invest in Multiple Opportunity Zones in 2026?

Yes. If you recognize gains from multiple asset sales in 2026, each gain can be independently reinvested into different opportunity zones. You might reinvest real estate gains into a Cleveland opportunity zone fund and business sale proceeds into a Cincinnati opportunity zone operating business. Each investment has its own 180-day deadline, but they can be coordinated for tax efficiency.

How Do I Know if an Investment is Truly a Qualified Opportunity Zone Vehicle?

Verify directly with the fund manager or investment sponsor. Ask for their Form 8949 or an opinion letter from their tax counsel confirming qualified status. The IRS website maintains lists of registered opportunity zone funds, though the list isn’t exhaustive. Never rely solely on marketing materials—demand tax documentation verifying the fund’s qualified status.

Related Resources

- Tax Strategy Planning Services for business owners deploying capital in 2026

- Real Estate Investor Tax Planning guides for opportunity zone and cost segregation strategies

- IRS Opportunity Zones FAQ – Official federal resource

- Ongoing Tax Advisory Services to monitor opportunity zone compliance through 2026 and beyond

- High-Net-Worth Tax Planning for sophisticated investors managing multiple opportunity zone positions

Last updated: March, 2026