New Hampshire 2026 Tax Changes — How OBBBA and State Tax Repeals Create a Double Win

On January 1, 2026, the tax landscape for New Hampshire residents will undergo a historic and positive transformation. At the federal level, the One Big Beautiful Bill Act (OBBBA ) has made the popular 2017 TCJA tax cuts permanent and introduced new benefits, avoiding the feared “tax cliff.”

This federal relief is amplified by New Hampshire’s own major tax reform: the complete repeal of the Interest & Dividends (I&D) Tax, which is being phased out and will be fully eliminated by 2027. This makes New Hampshire one of the few truly tax-free states for individual income, creating a powerful “double win” for residents, investors, and business owners.

This guide provides a clear, localized breakdown of how these permanent federal and state tax laws will impact your income, business, and financial strategy in 2026 and beyond.

The Double Win: Federal Relief and State Tax Elimination

Part 1: Permanent Federal Relief from OBBBA

OBBBA has made the federal tax picture much brighter for all Americans, including New Hampshire residents.

- LowerFederal Tax Brackets are PERMANENT: The lower individual income tax rates from the TCJA are here to This is a crucial win for New Hampshire’s working families, skilled trades, and professionals.

- The Federal Standard Deduction is PERMANENT: The higher federal standard deduction is also permanent, simplifying filing and lowering federal taxable income for the majority of households.

- The QBI Deduction is PERMANENT and ENHANCED: The 20% Qualified Business Income (QBI) Deduction is a permanent part of the federal tax code, a massive benefit for the state’s many small businesses, contractors, and tourism operators.

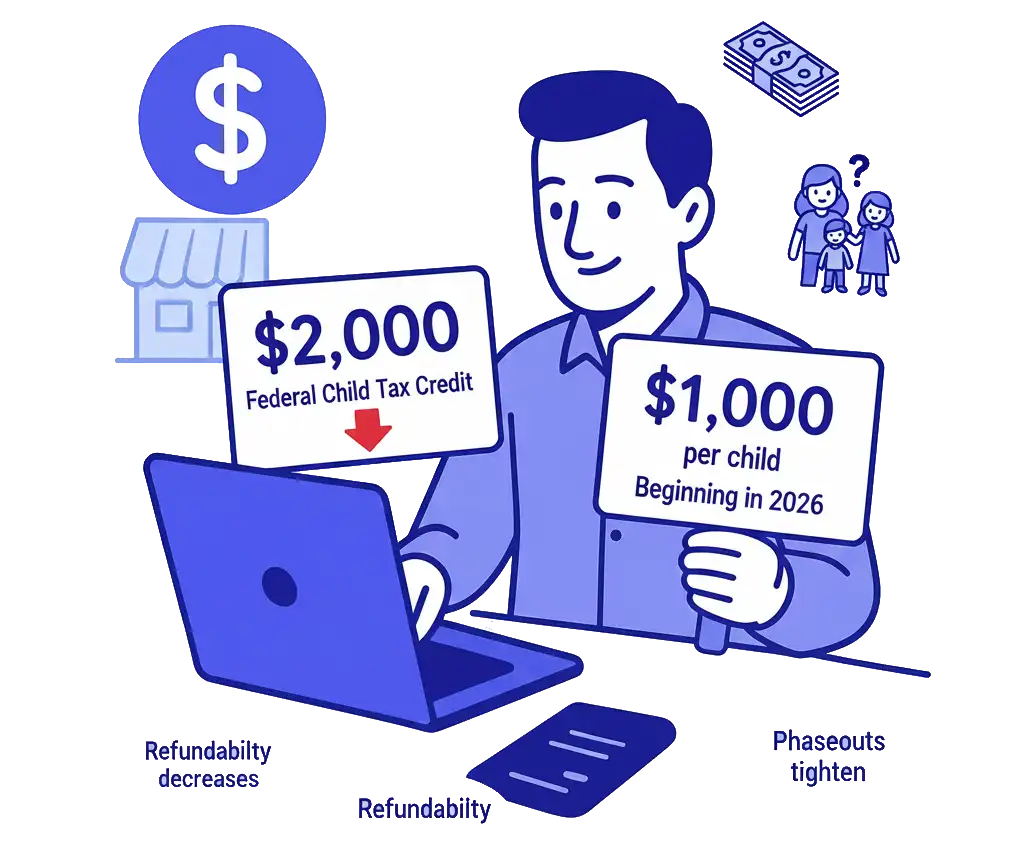

Child Tax Credit Shrinks

- The Child Tax Credit decreases from about $2,000

- To roughly $1,000 per child

- Refundability decreases

Families throughout southern New Hampshire and growing suburban regions will see reduced federal refunds.

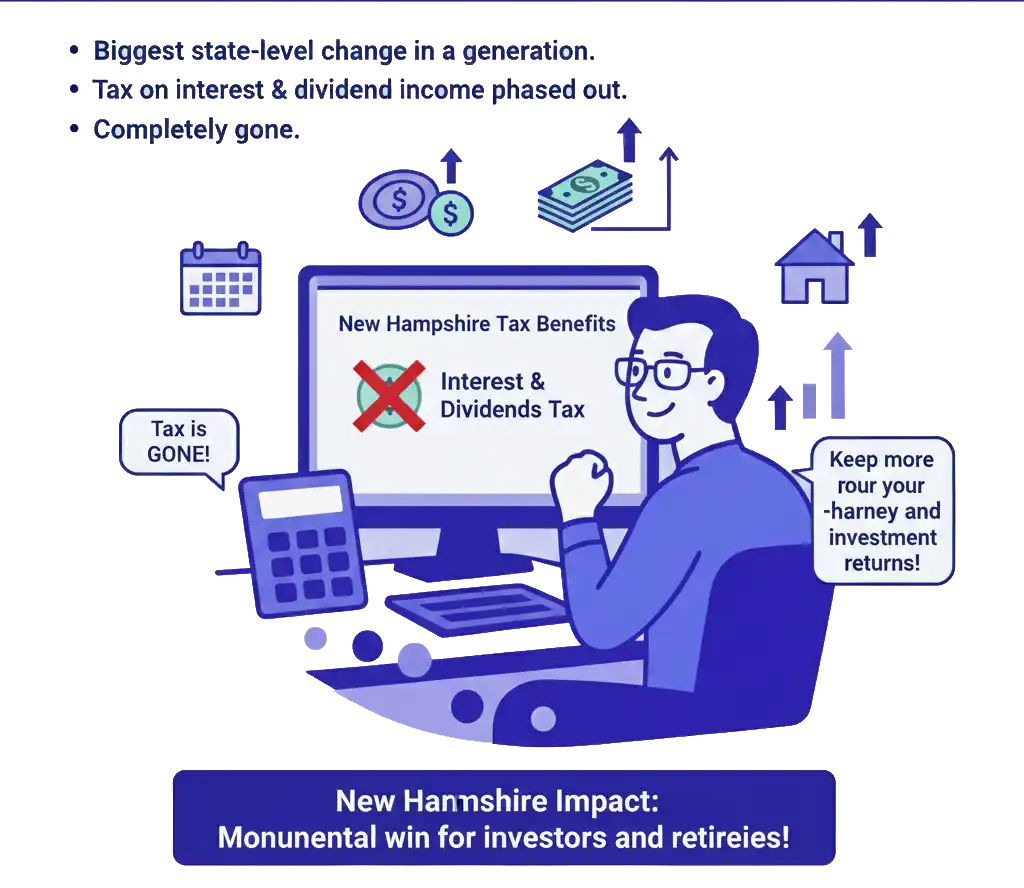

Part 2: New Hampshire Becomes Truly Income-Tax-Free

This is the biggest state-level tax change in a generation. While New Hampshire has never taxed wages, it did tax interest and dividend income. That tax is being phased out and will be gone completely.

New Hampshire Impact:

- This is a monumental win for investors, retirees, and anyone with a brokerage account. When combined with the permanent federal cuts, it means New Hampshire residents will keep more of their hard-earned money and investment returns.

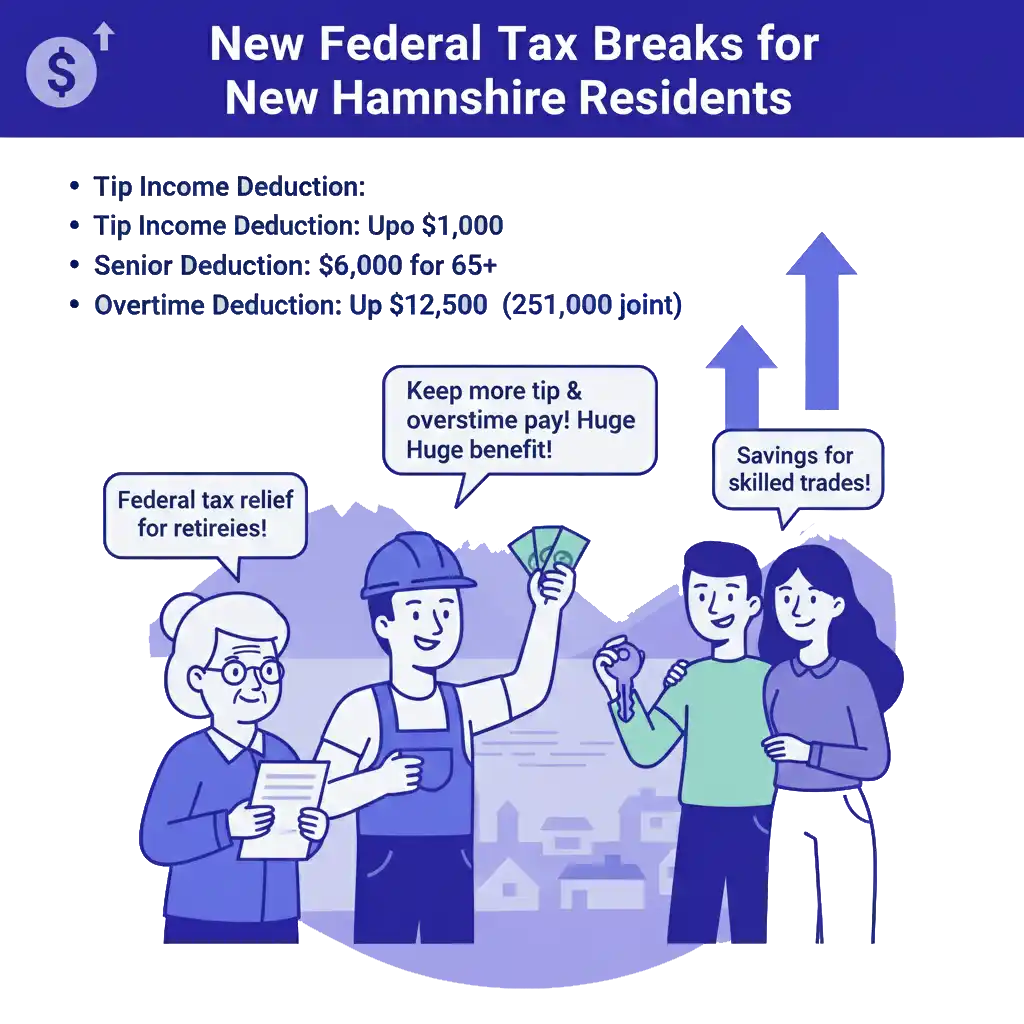

New Federal Tax Breaks for New Hampshire Residents

OBBBA also introduced several new federal deductions that will directly benefit many in New Hampshire:

- Tip Income Deduction: Deduct up to $25,000 of reported tip income. This is a huge benefit for workers in New Hampshire’s thriving tourism and hospitality sectors in the Lakes Region, White Mountains, and

- Senior Deduction: An additional $6,000 deduction for individuals 65 and older (subject to phase-out).

- Overtime Deduction: Deduct up to $12,500 ($25,000 for joint filers) of qualified overtime pay, a great benefit for skilled trades and healthcare workers.

New Hampshire-Specific Tax Considerations for 2026

A Major Win for Tourism and Small Business

The new federal Tip Income Deduction is a game-changer for New Hampshire’s tourism economy. From restaurant servers in Portsmouth to hotel staff in the White Mountains, this provides direct, substantial federal tax relief.

Furthermore, the permanent 20% federal QBI Deduction provides certainty and significant tax savings for the thousands of entrepreneurs, contractors, and small business owners who are the backbone of the state’s economy.

The Ultimate Retirement and Investment Haven

New Hampshire already attracts retirees because it does not tax Social Security or other retirement income. The repeal of the I&D tax, combined with permanent lower federal tax rates under OBBBA, makes it one of the most attractive states in the nation for retirees and investors.

Real Estate and STRs

For property owners in the Lakes Region, White Mountains, and Seacoast, OBBBA brings welcome news. The 100% bonus depreciation for qualified property is now permanent. This allows real estate investors and STR hosts to immediately write off the cost of certain assets on their federal return, making strategies like cost segregation incredibly powerful.

What New Hampshire Taxpayers Should Do Now

- Update Your Tax Plan: Your old strategy is It’stime to build a new plan based on the dual benefits of permanent federal cuts and New Hampshire’s elimination of the I&D tax.

- Maximize New Federal Deductions: If you earn tips or overtime, ensure you are accurately tracking your income to take full advantage of these powerful new federal

- Leverage Your Business Structure: Work with a professional to ensure your LLC or S-Corp is structured to maximize the permanent 20% federal QBI deduction.

- Review Your Investment Strategy: With the I&D tax gone, review your portfolio for opportunities to generate tax-free income at the state level.

New Hampshire 2026 Tax FAQ

Does New Hampshire tax wages?

No. New Hampshire does not tax earned income.

Did OBBBA prevent federal tax increases?

OBBBA preserved QBI but allowed many TCJA provisions — such as brackets and the standard deduction — to expire.

Are families affected?

Yes — reduced child credits and higher taxable income impact refunds.

Are STR owners impacted?

Yes — participation and depreciation rules tighten significantly.

Are retirees affected?

Yes — higher federal brackets increase taxation of retirement withdrawals.

Get Your Personalized 2026 New Hampshire Tax Plan

The tax landscape has permanently shifted in your favor. Don’t operate on outdated assumptions. A personalized strategy session will ensure you are structured to maximize every new and permanent benefit under OBBBA and New Hampshire’s new tax-free status.

Because tax situations vary by individual and business, many New Hampshire residents choose to work with a qualified tax professional. You can explore available New Hampshire tax services here: