Minnesota 2026 Tax Changes — What the One Big Beautiful Bill Act (OBBBA ) Means for Residents

On January 1, 2026, the federal tax landscape underwent a historic and positive transformation. The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, made permanent many of the major tax cuts from the 2017 Tax Cuts and Jobs Act (TCJA) and introduced new, powerful benefits for taxpayers. The long-feared 2026 “tax cliff” has been avoided.

For residents of Minnesota, this is exceptionally good news. In a state with a progressive, high-tax environment, these permanent federal tax cuts provide crucial relief. This guide provides a clear, localized breakdown of how the permanent tax laws under OBBBA will impact your income, business, and financial strategy in 2026 and beyond.

Federal Changes Bring Relief to Minnesota Taxpayers

While Minnesota has its own progressive tax system, your federal tax bill is a major part of your overall financial picture. OBBBA has made that picture much brighter.

Lower Federal Tax Brackets are PERMANENT

- The biggest news is that the lower individual income tax rates from the TCJA are now permanent. The anticipated jump in federal tax rates has been avoided.

Minnesota Impact:

This is a crucial win for Minnesota’s high-earning professional households. For the many healthcare professionals in the Mayo Clinic ecosystem, corporate employees in the Twin Cities, and tech workers, having lower, predictable federal tax rates provides significant and welcome financial breathing room in a high-tax state.

The Federal Standard Deduction is PERMANENT

The higher federal standard deduction, which simplifies tax filing for millions, is also here to stay.

Minnesota Impact:

A permanent, higher federal standard deduction is a direct benefit for the majority of Minnesotans, especially in a state with high housing costs and property taxes. It provides a substantial, straightforward deduction on your federal return, lowering your taxable income without the need for complex itemization.

The QBI Deduction is PERMANENT and ENHANCED (Federal Level)

This is a critical update for Minnesota’s many small businesses, consultants, and independent contractors. The 20% Qualified Business Income (QBI) Deduction is not expiring. OBBBA has made it a permanent part of the federal tax code and even improved it.

Important Note for Minnesota:

- Minnesota is a non-conforming state, meaning it does not offer a state-level QBI deduction. However, this powerful 20% deduction remains fully available on your federal tax return.

This is a major federal benefit for Minnesota’s:

- Skilled trades and construction contractors

- Healthcare consultants and medical professionals with private practices

- LLCs, S-Corps, and Sole Proprietors

- Real estate investors and landlords

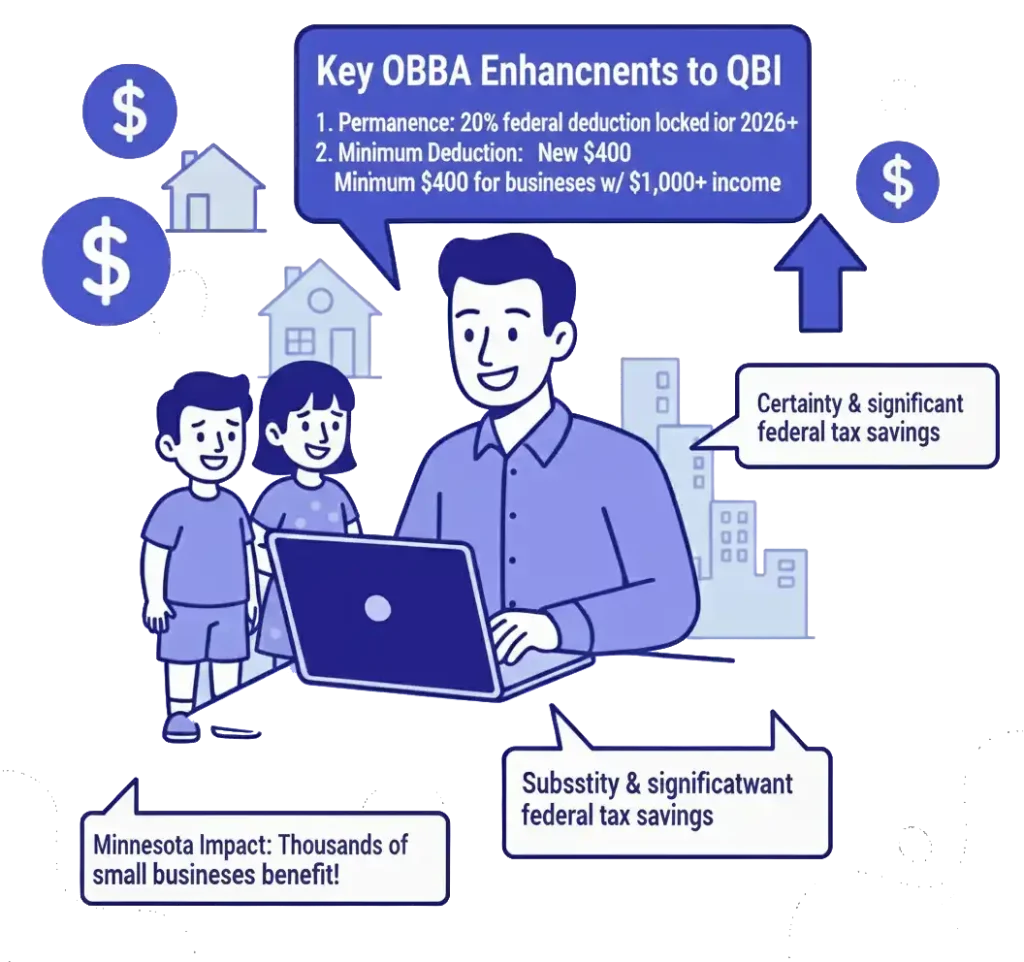

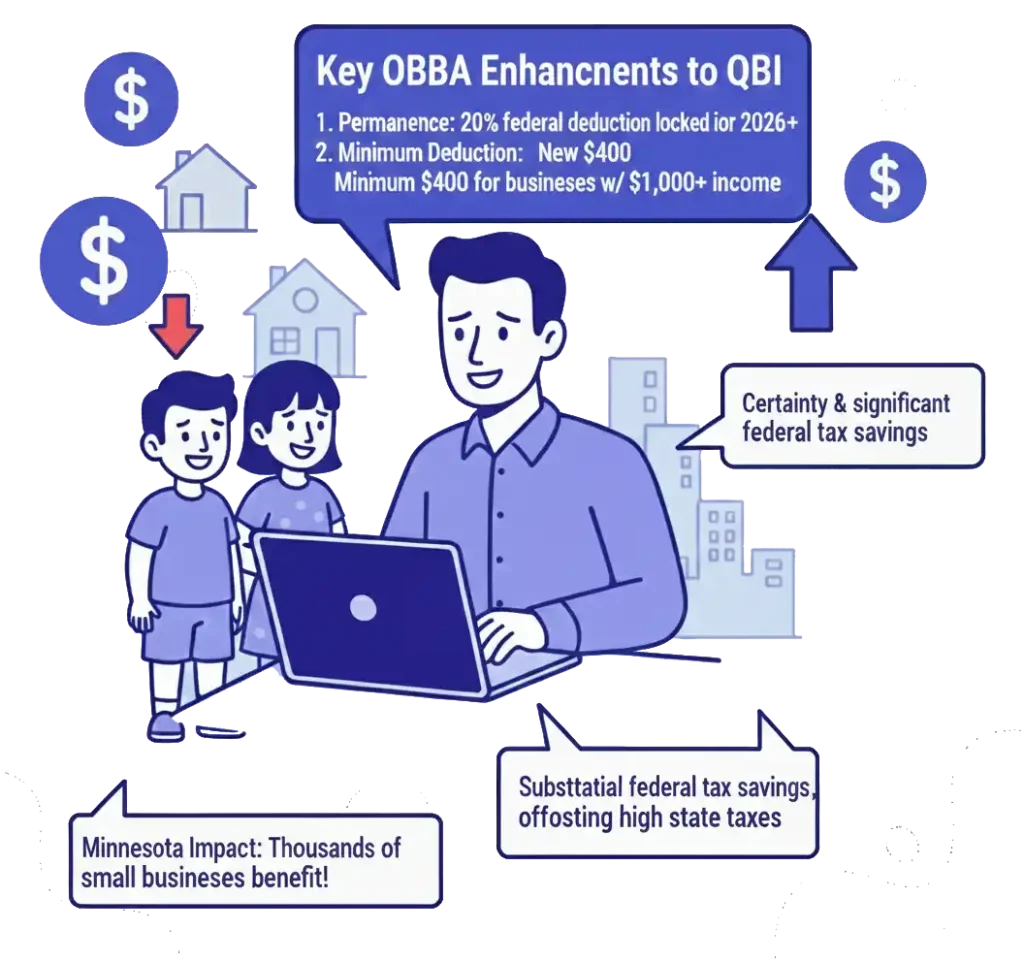

Key OBBBA Enhancements to QBI:

- Permanence: The 20% federal deduction is locked in for 2026 and

- Minimum Deduction: A new $400 minimum federal deduction is available for any business with at least $1,000 of qualified

Minnesota Impact:

For the thousands of small businesses that drive Minnesota’s economy, the permanent federal QBI deduction provides certainty and significant federal tax savings, helping to offset the high state tax burden.

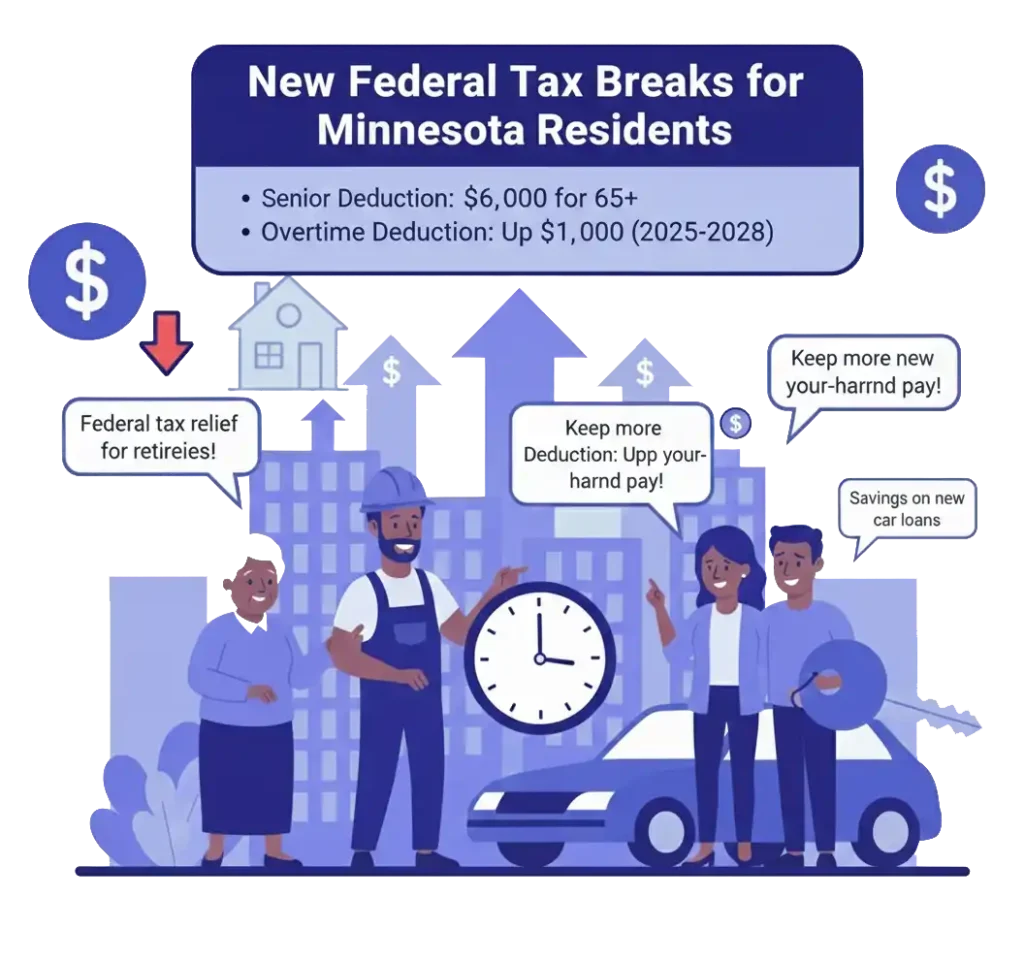

New Federal Tax Breaks for Minnesota Residents

OBBBA also introduced several new federal deductions that will directly benefit many in Minnesota:

- Senior Deduction: An additional $6,000 deduction for individuals 65 and older, providing federal tax relief for Minnesota’s retirees (subject to phase-out).

- Overtime Deduction: Deduct up to $12,500 ($25,000 for joint filers) of qualified overtime

- Auto Loan Interest Deduction: Deduct up to $10,000 in interest on new personal vehicle loans from 2025-2028.

Minnesota-Specific Tax Considerations for 2026

Minnesota’s State Tax and Federal AGI

Minnesota has one of the most progressive state income tax systems in the nation, with rates climbing to 9.85%. Because the state uses federal Adjusted Gross Income (AGI) as the starting point for its calculations, the permanent federal deductions under OBBBA help keep your AGI lower. This provides a positive starting point for calculating your Minnesota state tax, offering some relief from the state’s high rates.

Real Estate in a High-Value Market

For property owners in competitive markets like the Twin Cities metro, Rochester, and the Lake Minnetonka area, OBBBA brings welcome news. The 100% bonus depreciation for

qualified property is now permanent. This allows real estate investors to immediately

write off the cost of certain assets on their federal return, making strategies like cost segregation incredibly powerful.

Retirement Income in Minnesota

Minnesota taxes most forms of retirement income, including 401(k) and IRA distributions,

and even some Social Security benefits for higher earners. The good news is that the

permanent lower federal tax rates under OBBBA reduce the overall tax burden on these withdrawals, leaving more money in your pocket during your retirement years, even if state taxes still apply.

What Minnesota Taxpayers Should Do Now

- UpdateYour Tax Plan: Your old strategy, based on the fear of expiring tax cuts, is It’s time to build a new plan based on permanence and new federal opportunities.

- Integrate Federal and State Planning: Work with a professional who understands how to maximize permanent federal benefits while navigating Minnesota’s complex, high- tax

- Maximize the Federal QBI Deduction: If you own a business or are a contractor, ensure your structure and bookkeeping are optimized to claim the full 20% federal QBI

- LeverageReal Estate Benefits: Plan your real estate investments to take full advantage of permanent 100% bonus depreciation on your federal return.

Minnesota 2026 Tax FAQ

Does Minnesota conform to QBI?

No — QBI is federal-only.

Will Minnesota taxes rise?

Rates stay the same, but taxable income increases due to federal changes.

Are families affected?

Yes — reduced credits and higher taxable income impact refunds.

Are STR owners affected?

Yes — depreciation and participation rules tighten.

Are retirees affected?

Yes — federal bracket increases raise tax on withdrawals and investment income.

Get Your Personalized 2026 Minnesota Tax Plan

The tax landscape has permanently shifted in your favor. Don’t operate on outdated assumptions. A personalized strategy session will ensure you are structured to maximize every new and permanent benefit under OBBBA, fully integrated with Minnesota’s unique economic and tax environment.

Because tax situations vary by individual and business, many Minnesota residents choose to work with a qualified tax professional. You can explore available Minnesota tax services here: