Indiana vs Texas Taxes: A 2026 State Tax Comparison Guide

When it comes to Indiana vs Texas taxes for the 2026 tax year, the differences are stark and strategically important. Indiana currently imposes a 3.23% state income tax on residents, while Texas maintains zero state income tax—a fundamental distinction that affects thousands of business owners, contractors, and high-income professionals. Understanding how Indiana and Texas approach taxation is essential for anyone considering relocation, business structure optimization, or comprehensive tax planning in 2026.

Table of Contents

- Key Takeaways

- How Do Indiana and Texas Handle State Income Tax?

- What Are the Property Tax Differences Between Indiana and Texas?

- How Do Sales Tax Rates Compare in Indiana vs Texas?

- What New Tax Legislation Affects Indiana in 2026?

- Which State Is Better for Business Owners and Contractors?

- Uncle Kam in Action: Strategic Tax Planning Across State Lines

- Next Steps

- Frequently Asked Questions

Key Takeaways

- Texas has zero state income tax while Indiana charges 3.23%, making Texas significantly advantageous for high-income earners in 2026.

- Indiana SB 243 (effective for 2026 income) provides temporary relief on overtime and tips income, reducing state revenue by $250 million.

- Property taxes vary significantly: Texas relies heavily on property taxes to replace lost income tax revenue, while Indiana has moderate rates.

- Sales taxes in Indiana (7% base) exceed Texas rates in most areas, though Texas uses sales tax strategically to compensate for no income tax.

- Relocation strategy should consider total tax burden, including federal standard deductions of $31,500 (MFJ) for 2026.

How Do Indiana and Texas Handle State Income Tax?

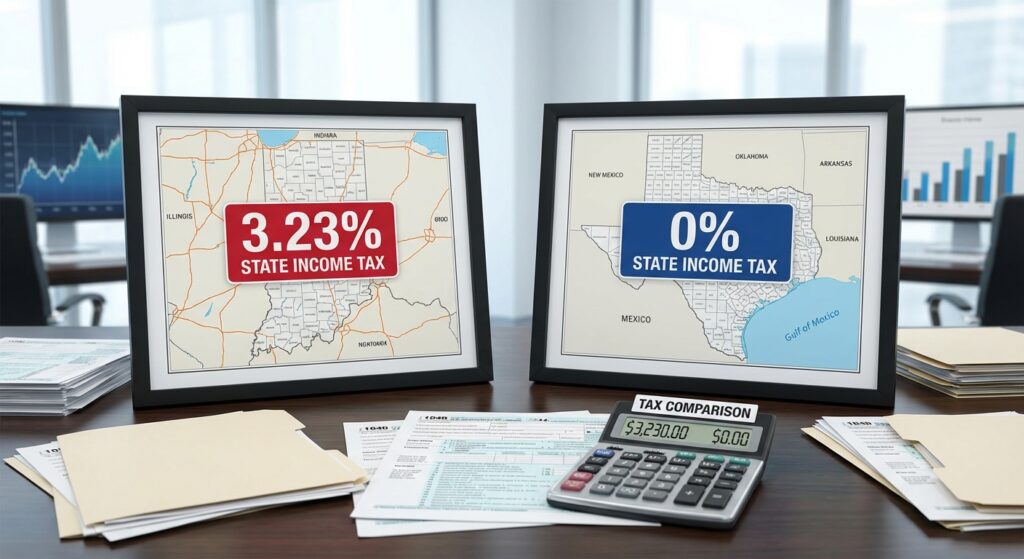

Quick Answer: Texas has zero state income tax, while Indiana imposes a flat 3.23% state income tax on all residents. This difference creates millions in tax savings for high-income professionals relocating to Texas.

The most significant distinction between Indiana vs Texas taxes is the state income tax structure. For the 2026 tax year, Indiana residents pay a flat 3.23% state income tax on wages, business income, and investment income. In contrast, Texas imposes no state income tax whatsoever. This fundamental difference means that a self-employed contractor earning $150,000 annually would owe approximately $4,845 in Indiana state income tax but zero state income tax in Texas.

Indiana’s Flat Income Tax Structure

Indiana applies a uniform 3.23% tax rate to all income types, making it predictable but relatively expensive compared to no-income-tax states. This means wage earners, business owners, and retirees all pay the same rate. The Indiana Department of Revenue requires state income tax returns for residents with income above certain thresholds, and estimated quarterly tax payments are necessary for self-employed individuals and business owners. For federal purposes, Indiana residents can benefit from federal deductions—such as the 2026 standard deduction of $31,500 for married couples filing jointly—but Indiana provides no state-level equivalent deduction, making the state income tax apply to nearly all household income.

Texas’s Zero Income Tax Advantage

Texas has maintained a zero state income tax policy for decades, a strategic choice that has attracted high-income professionals and entrepreneurs nationwide. According to White House economic analysis, states without income taxes like Texas rank among the top 10 in GDP growth and net migration rates. For 2026, a Texas resident earning $200,000 saves approximately $6,460 in state income tax compared to an Indiana resident with identical income. This creates powerful incentives for business relocation and individual tax planning.

Pro Tip: The absence of state income tax in Texas applies equally to W-2 wages, self-employment income, and passive investment income. This makes Texas particularly attractive for contractors, real estate investors, and business owners earning significant income in 2026.

What Are the Property Tax Differences Between Indiana and Texas?

Quick Answer: Texas property taxes are significantly higher than Indiana’s because Texas must generate state revenue without income tax. Indiana homeowners enjoy moderate property tax rates, while Texas property taxes range from 0.8% to 2% of home value.

While Indiana maintains an income tax, Texas compensates by relying heavily on property taxes. This creates a trade-off that business owners and homebuyers must evaluate carefully. For the 2026 tax year, Texas is actively debating property tax reform, with proposals targeting targeted relief for first-time homebuyers and property tax reduction strategies. The property tax comparison reveals that Indiana offers a more balanced approach across multiple tax types, while Texas concentrates revenue collection through property and sales taxes.

Indiana’s Property Tax Rates

Indiana property tax rates are generally moderate, averaging between 0.65% and 0.85% of home value depending on county and local levies. This makes Indiana competitive nationally. Property owners also benefit from homestead property tax deductions, which provide relief for primary residences. For someone with a $350,000 home in Indiana, annual property taxes might range from $2,275 to $2,975, depending on local school district and county assessments.

Texas Property Tax Burden

Texas property tax rates are among the highest in the nation, ranging from 0.8% to 2.0% of home value, with most areas clustering around 1.2% to 1.8%. This compensates for the zero state income tax. For the same $350,000 home in Texas, annual property taxes could range from $2,800 to $7,000. While this seems expensive compared to Indiana, Texas residents save thousands annually on state income tax, creating a mixed financial picture that depends on individual income levels and property values.

| Tax Category | Indiana (2026) | Texas (2026) |

|---|---|---|

| State Income Tax | 3.23% flat | 0% (no tax) |

| Property Tax Rate | 0.65% – 0.85% | 0.8% – 2.0% |

| Sales Tax (Base) | 7% + local (up to 9.65%) | 6.25% + local (up to 8.25%) |

| Tax on Tips & OT Income | 3.23% (temporary 2026 relief pending) | 0% (federal deduction applies) |

How Do Sales Tax Rates Compare in Indiana vs Texas?

Quick Answer: Indiana’s base sales tax is 7% (plus local additions reaching up to 9.65%), while Texas’s base is 6.25% (up to 8.25% with local taxes). Indiana has higher sales taxes, offsetting some income tax advantages.

Sales tax rates represent another significant distinction in Indiana vs Texas taxes for 2026. Indiana imposes a 7% state sales tax plus local option taxes that can add up to 2.65% additional, totaling as high as 9.65% in some jurisdictions. Texas charges 6.25% state sales tax plus local options that can reach 2%, for a combined maximum of 8.25%. This difference becomes material when making large purchases like vehicles or real estate furnishings. For a $40,000 vehicle purchase, Indiana sales tax could reach $3,860, while Texas would charge approximately $3,300—a $560 difference favoring Texas.

Food, Clothing, and Exempt Items

Both states exempt groceries and unprepared food from sales tax, making daily living somewhat comparable. However, Indiana taxes clothing, while Texas provides a clothing exemption during certain periods. Prescription medications are tax-exempt in both states, benefiting seniors and those with chronic conditions who claim deductions under the IRS Publication 502 for medical expenses. Understanding these exemptions is important for business owners evaluating cost-of-living comparisons between the two states.

Did You Know? Texas voters passed Proposition 3 allowing temporary sales tax holidays on school supplies, clothing, and sports equipment. Indiana has no similar statewide exemption, making back-to-school shopping significantly cheaper in Texas.

What New Tax Legislation Affects Indiana in 2026?

Quick Answer: Indiana SB 243, passed by the state Senate 47-1, provides a one-year tax break on tips and overtime income for 2026, reducing state revenue by approximately $250 million and applying to income filed in 2027 returns.

Indiana legislative action in 2026 directly impacts state tax planning. Senate Bill 243 represents a major development for workers earning overtime and tips income. Passed with near-unanimous bipartisan support on January 29, 2026, SB 243 conforms Indiana’s tax treatment of federal deductions created under the One Big Beautiful Bill Act. This legislation benefits service industry workers, overtime employees, and anyone earning supplemental income through tips. The temporary nature of this relief—lasting only one year—creates urgency for eligible workers to document and claim qualifying income.

Understanding SB 243: Tips and Overtime Relief

SB 243 implements federal provisions allowing overtime deductions of up to $12,500 per individual return ($25,000 for joint filers) and tips deductions of up to $25,000 annually. On the 2026 Indiana tax return (filed in April 2027), qualifying workers reduce their taxable income through these deductions, saving approximately 3.23% on the deducted amounts. For someone with $25,000 in overtime income, the tax savings equals approximately $808 at Indiana’s 3.23% rate. However, unlike federal treatment where these deductions phase out, Indiana’s implementation remains generous for 2026 only.

Temporary Nature and Planning Implications

The temporary one-year nature of SB 243 is critical. Senate Finance Chair Travis Holdman indicated the state will reassess in 2027 whether to extend this relief beyond 2026. This creates important planning considerations: individuals should maximize overtime and tips income recognition during 2026 while this tax break is available. Additionally, the $250 million revenue reduction highlighted by state legislators shows this is a significant tax expenditure. Business owners and contractors should consult professional tax advisors to ensure they’re properly categorizing and claiming eligible income to maximize 2026 benefits.

Which State Is Better for Business Owners and Contractors?

Quick Answer: Texas is generally superior for high-income business owners due to zero state income tax, though Indiana’s moderate property taxes and corporate tax advantages may appeal to specific business structures.

For small business owners, consultants, and 1099 contractors, Indiana vs Texas taxes creates substantially different financial outcomes. A self-employed business owner earning $250,000 annually pays approximately $8,075 in Indiana state income tax but zero in Texas. When multiplied by business lifespan, this difference funds expansion, hiring, or retirement savings. The White House Council of Economic Advisers documented that no-income-tax states experience 16% to 19% higher new startup formation rates, suggesting Texas’s tax structure actively encourages entrepreneurship.

Contractor and 1099 Income Advantages in Texas

Independent contractors filing Schedule C should carefully evaluate relocation to Texas. In 2026, contractors can claim the federal standard deduction of $15,750 (single) or $31,500 (married filing jointly), reducing federal taxable income. However, self-employment tax of 15.3% applies to approximately 92.35% of net self-employment income regardless of state. Indiana’s 3.23% state tax compounds this burden, while Texas’s zero state tax preserves more business income for reinvestment. Over a 20-year career, this difference accumulates to hundreds of thousands of dollars for six-figure contractors.

Real Estate Investors and Property Considerations

Real estate investors face complex trade-offs in Indiana vs Texas taxes. Texas’s higher property tax rates (1.2%-1.8%) eat into rental income, but investors can deduct these property taxes as business expenses under IRS Publication 946 for depreciation and cost recovery. Additionally, real estate investors in both states benefit from depreciation deductions—a non-cash deduction that reduces taxable income without affecting cash flow. For long-term investors holding property multiple decades, Texas’s zero state income tax advantage often outweighs higher property taxes, especially when depreciation is optimized.

| Income Level | Indiana State Tax (2026) | Texas State Tax (2026) | Annual Savings (TX) |

|---|---|---|---|

| $100,000 | $3,230 | $0 | $3,230 |

| $200,000 | $6,460 | $0 | $6,460 |

| $500,000 | $16,150 | $0 | $16,150 |

Uncle Kam in Action: Strategic Tax Planning Across State Lines

Client Snapshot: Jennifer, a 42-year-old management consultant, earned $280,000 through her Indiana-based consulting practice in 2025. She was considering relocation to Texas to expand her client base and reduce tax burden.

Financial Profile: $280,000 annual business income, $450,000 home value in Indianapolis, married filing jointly, two children ages 8 and 12, significant charitable contributions averaging $15,000 annually.

The Challenge: Jennifer was paying approximately $9,044 in Indiana state income tax annually on her business income, plus high property taxes on her home. Her Texas clients were suggesting she relocate her home office to Austin for better business growth and tax efficiency. However, she was uncertain about Texas’s higher property taxes and how the move would affect her family’s overall financial picture, including potential impacts on her children’s college savings and charitable giving incentives.

The Uncle Kam Solution: Uncle Kam’s analysis revealed multiple opportunities. First, we modeled a Texas relocation scenario examining total tax burden: eliminating $9,044 in Indiana state income tax, but replacing it with estimated Texas property taxes of $7,650 annually (on a similar $450,000 home). The net savings: approximately $1,394 per year in state/local taxes. However, we discovered additional advantages: qualifying for the 2026 federal deduction of $31,500 for married couples filing jointly and maximizing business deductions through proper entity structuring. We recommended converting to an S-Corp structure effective January 1, 2026, which would provide self-employment tax savings of approximately $8,400 annually on her business income—far exceeding state tax savings.

The Results:

- State Tax Savings: $1,394 annually through Texas relocation (Indiana income tax elimination partially offset by higher property taxes)

- Federal Self-Employment Tax Savings: $8,400 annually through S-Corp election

- Total First-Year Savings: $9,794 (representing a 3.5% reduction in her overall tax burden)

- Investment Strategy: The firm helped establish a Trump Account for her youngest child, capturing the $1,000 federal contribution and structuring annual family contributions of $5,000 to maximize tax-advantaged wealth building

- Charitable Giving Optimization: Established a Donor-Advised Fund to strategically bunch charitable contributions in high-income years while maintaining tax deductions

This is just one example of how our comprehensive tax strategy services have helped entrepreneurs achieve significant savings through state-level tax planning combined with federal optimization. Jennifer’s decision to relocate was supported by concrete numbers showing a $9,794 first-year return on strategic planning.

Next Steps

Take these actionable steps to optimize your Indiana vs Texas tax situation for 2026:

- Calculate Your State Tax Burden: Use your 2025 tax return to estimate Indiana or Texas taxes on your 2026 projected income. Factor in SB 243 relief if you earn tips or overtime.

- Evaluate Total Tax Burden: Don’t compare income tax in isolation. Model state income tax, property tax, and sales tax impacts on your household. Professional tax preparation services in Indiana can provide detailed analysis for your specific situation.

- Review Business Structure: If you’re self-employed, analyze whether S-Corp election or LLC treatment could reduce self-employment tax—often providing greater savings than state tax differences.

- Document Qualifying Income: If earning tips or overtime in Indiana, maintain careful records to maximize SB 243 deduction claims on your 2026 return filed in 2027.

- Consult a Tax Professional: State relocation decisions involve complex implications for federal taxation, business structure, and estate planning. Schedule a consultation to develop a personalized strategy aligned with your 2026 and 10-year financial goals.

Frequently Asked Questions

Does Texas Really Have No State Income Tax in 2026?

Yes, Texas maintains zero state income tax for 2026 and has no plans to implement one. This has been consistent policy for decades. However, Texas compensates through higher property taxes and sales taxes. The economic impact is significant: research shows no-income-tax states like Texas experience stronger GDP growth and higher business formation rates. For high-income professionals, this advantage is substantial and typically justifies relocation costs.

How Much Will Indiana SB 243 Save Me on My 2026 Taxes?

Savings depend on your qualifying income. Under SB 243, you can deduct up to $12,500 in overtime income (or $25,000 for joint filers) and up to $25,000 in tips annually. These deductions reduce Indiana taxable income by 3.23% of the deducted amount. For someone with $20,000 in qualifying tips, the Indiana tax savings equals $646 ($20,000 × 3.23%). However, this relief is temporary—effective only for 2026 income—making it prudent to maximize documentation and recognition in 2026.

If I Relocate from Indiana to Texas, When Does Texas Claim Me as a Resident for Tax Purposes?

Generally, you become a Texas tax resident when you establish a domicile by moving your primary residence and establishing proof of intent to remain (voting registration, driver’s license, property ownership). If you relocate mid-year, you may owe partial-year Indiana and Texas taxes. Filing position becomes important: allocate income between states based on days worked in each. For complex mid-year relocations, consult a CPA specializing in multi-state taxation to avoid audit risk and ensure proper filing.

Are Texas Property Taxes Really That Much Higher Than Indiana’s?

Yes. Texas property tax rates average 1.2% to 1.8% of home value, while Indiana averages 0.65% to 0.85%. On a $400,000 home, Texas property taxes might run $4,800 to $7,200 annually versus Indiana’s $2,600 to $3,400. However, Texas is implementing property tax relief for certain demographics in 2026, and the state legislature is actively debating homestead exemption expansions. Additionally, the zero state income tax often more than compensates the property tax difference for higher-income households.

Can I Claim Both Indiana and Texas Tax Deductions if I Work in Both States?

No, you can’t claim deductions for both states. However, you may pay tax to both states if you work in both. Most states offer “tax credits for taxes paid to other states” to prevent double taxation. If you earn $100,000 in Indiana and $100,000 in Texas, you’d allocate the 2026 federal standard deduction ($31,500 for MFJ) between both states based on income allocation. Indiana would tax its portion, and Texas would tax its portion (but at 0%). You’d claim an Indiana tax credit on your federal return for any double taxation. Proper allocation requires professional guidance.

Which State Is Better for Retirees: Indiana or Texas?

For retirees, Texas’s zero state income tax is advantageous because Social Security, retirement account withdrawals, and investment income are not subject to state tax. However, retirees should evaluate property taxes, which can be substantial on fixed incomes. Indiana offers tax breaks for retirees over 65, including a potential $6,000 senior deduction for Social Security (federal). Overall, Texas generally saves more money for higher-income retirees, while Indiana may benefit lower-income retirees with fixed pensions. The 2026 federal child tax credit of $2,200 per dependent may also influence decisions for multigenerational households.

How Do Federal Tax Changes in 2026 Impact Indiana vs Texas Comparisons?

Federal changes significantly impact state comparisons. The 2026 federal standard deduction ($31,500 for MFJ) benefits residents of both states equally at the federal level. However, Indiana doesn’t provide an equivalent state deduction—all Indiana income is subject to the 3.23% state tax. New federal deductions for tips ($25,000) and overtime pay ($12,500/$25,000 joint) reduce federal taxable income in both states, but Indiana residents still owe state tax on these amounts unless SB 243 applies. The One Big Beautiful Bill Act of 2025 raised the SALT deduction cap to $40,000 temporarily, benefiting high-income residents in both states with significant property taxes or state income taxes.

This information is current as of 02/03/2026. Tax laws change frequently. Verify updates with the IRS (IRS.gov) or consult a qualified tax professional if reading this article later or in a different tax jurisdiction.

Last updated: February, 2026